![]()

India’s stock market is full of fast-growing companies. Every day, we hear about startups or well-known brands doing something new. But sometimes, a company quietly grows in the background—steadily building value without making headlines. These are the companies that focus on strong leadership, solid business models, and long-term goals. And when they succeed, the results can be extraordinary.

In this blog, we’ll talk about one such company. We’ll take a close look at how it started, how it entered the defense sector, how it expanded into global markets, and how it stayed strong financially. Most importantly, we’ll explore what led to its incredible stock price growth of nearly 1,400% over the last five years—and whether that momentum can continue.

The Massive Growth of the Defense Stock Over 5 years:

The company at the center of this story is Solar Industries India Ltd. Based in Nagpur, Solar began as a mining explosives supplier. Today, it’s a major player in industrial and defence explosives and a key part of India’s journey toward self-reliance in defence manufacturing. Let’s explore how Solar Industries became one of the country’s top-performing stocks.

From Humble Beginnings to Global Success

Solar Industries began in 1995 under the name Solar Explosives Limited, founded by Mr. Satyanarayan Nuwal, who had been in the explosives business since 1984. Initially, the company distributed explosives, and over time, it moved into manufacturing bulk explosives, packaged explosives, and detonators.

As Solar Industries grew, it built a reputation for safety, quality, and reliability. The company started by supplying to mining and infrastructure industries but later expanded into defense and aerospace—a sector where it now plays a key role.

Also Read: Undervalued Or Underperforming? A Deep Dive Into Two Falling P/E Stocks

The Essential Growth Drivers

1. Defense Segment Expansion

Solar Industries has significantly diversified into high-end defense products:

- Producing advanced explosives like RDX and HMX.

- Manufacturing hand grenades for the Indian Army.

- Supplying Pinaka rocket boosters, a key indigenous artillery system.

- Partnering in BrahMos missile systems production—marking entry into strategic deterrence capabilities.

2. Make in India Push

- Entered defense manufacturing in 2010, aligning early with the government’s ‘Atmanirbhar Bharat’ initiative.

- Reinforced commitment at Davos 2024, with the CMD highlighting expansion in defense R&D and manufacturing under the Make in India drive.

3. Exports

- Export presence in over 65 countries (includes Zambia, Nigeria, Turkey, Ghana, South Africa, and more).

- In 2024, secured a ₹2,150 crore defense export order—its largest ever, enhancing global credibility.

4. Capacity Expansion

- Developing a central defense manufacturing hub in Nagpur.

- Announced ₹12,700 crore capex plan over the next few years.

- Investing in drone systems and loitering munitions to meet evolving warfare needs.

Key Milestones:

1996: Began Manufacturing Operations

Transitioned from trading to manufacturing with a licensed capacity of 6,000 MT, laying the foundation for vertical integration and long-term scalability.

2005: Full Subsidiary Consolidation

Acquired all key group entities (Economic Explosives, Solar Capitals, Solar Components), enabling unified operations under one corporate umbrella and stronger financial control.

2010: Entry into Defense Manufacturing

Marked a strategic pivot from industrial explosives to high-value defense segment—years ahead of the private sector defense boom under ‘Make in India’.

2018: Strategic Partnership with EURENCO (France)

Partnered with a global leader in propellants and ammunition to access advanced technologies, fast-tracking Solar’s credibility in artillery and bomb manufacturing.

2023: Delivered 100% Indigenous Ammunition to Indian Navy

Became the first private Indian company to fully indigenize 30mm ammunition, positioning itself as a vital partner in India’s defense self-reliance mission.

Recent milestones include:

- Supplying BrahMos missile boosters

- Delivering 100% Indigenous 30mm ammunition to the Indian Navy

- Testing NAGASTRA-1 loitering munition

- Securing a ₹239 crore order for hand grenades from the Ministry of Defence in March 2025

- Solar’s subsidiary Economic Explosives Limited (EEL) has partnered with the Maharashtra government to invest ₹12,700 crore in building a Defence and Aerospace Hub in Nagpur in January 2025.

- Q3 FY25 Result: Solar Industries India Ltd reported a 55% YoY surge in net profit to ₹7,315 Cr and a 38% rise in revenue to ₹71,973 Cr, with EPS at ₹734.80, reflecting robust growth and strong quarterly performance.

These successes have positioned Solar Industries as a trusted partner for India’s defense forces and have earned the company recognition globally.

Consistent Financial Growth

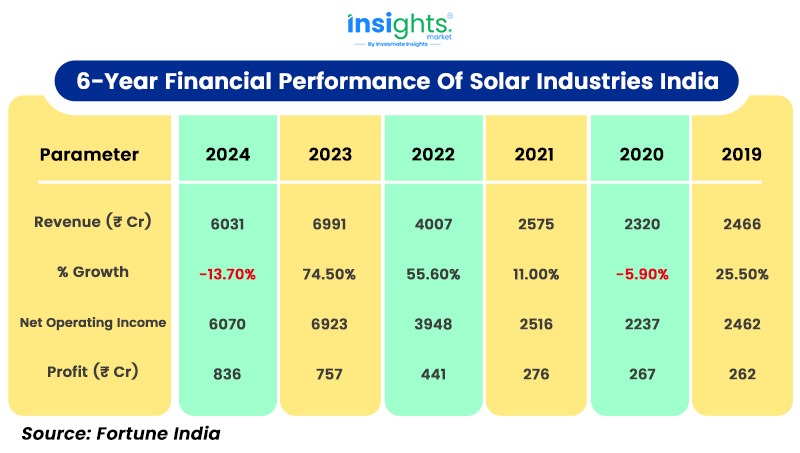

1. Revenue Trends (₹ Cr):

Revenue rose from ₹2,466 Cr in 2019 to a peak of ₹6,991 Cr in 2023, before dropping 13.7% to ₹6,031 Cr in 2024. The highest growth was in 2022 (+55.6%) and 2023 (+74.5%).

2.Net Operating Income:

Followed a similar trend as revenue, peaking at ₹6,923 Cr in 2023 before dipping to ₹6,070 Cr in 2024. Maintained an upward trajectory until FY2024.

3. Profit (₹ Cr):

PAT increased steadily from ₹262 Cr in 2019 to ₹836 Cr in 2024, with sharp growth post-2021 up 71.4% in 2022 and continuing to rise in the following years.

Read Also: The Quiet Rise Of Two Potential Multibaggers: PG Electroplast & Transformers & Rectifiers

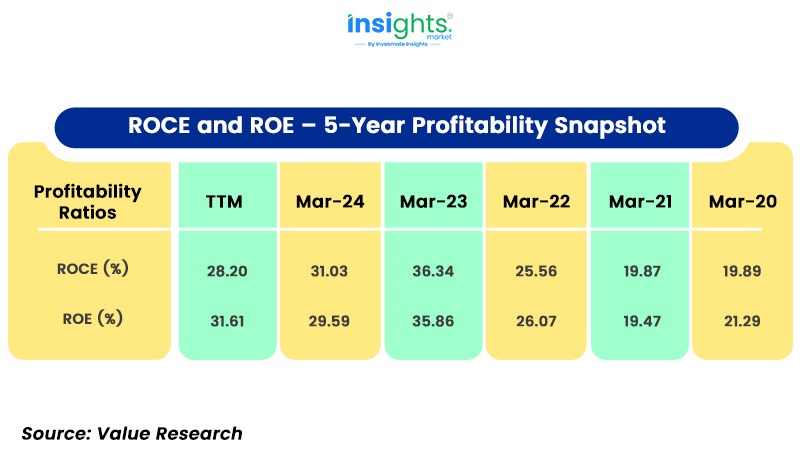

1. Return on Capital Employed (ROCE):

Declined from 36.34% in FY2023 to 28.02% in TTM Mar-24, but remains robust—indicating efficient capital utilization despite the drop.

2. Return on Equity (ROE):

Rose consistently from 19.47% in FY2021 to 31.61% in TTM Mar-24, reflecting strong shareholder value creation and improving financial efficiency.

Despite the slight dip in ROCE, the company maintains strong profitability and capital efficiency. The consistent increase in ROE suggests excellent value creation for shareholders, reflecting a positive long-term trend in the company’s performance.

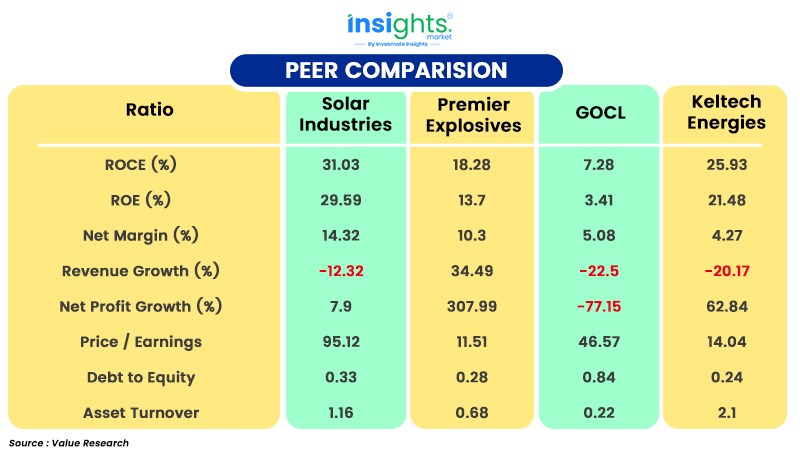

ROCE and ROE: Solar Industries leads with the highest ROCE (31.03%) and ROE (29.59%), indicating superior capital efficiency and returns for shareholders compared to its peers.

Net Margin: Solar Ind. also performs strongly with a net margin of 14.32%, significantly higher than Premier Explosives (10.3%) and the others.

Revenue and Profit Growth: Solar saw a decline in revenue (-12.32%), but Premier Explosives experienced strong growth (+34.49%). However, Solar’s profit growth (+7.9%) outperformed GOCL’s (-77.15%) and Keltech’s (+62.84%).

Valuation: Solar’s high P/E ratio (95.12) suggests a premium valuation compared to peers, indicating that investors may expect continued strong growth.

Debt to Equity: Solar has a moderate debt-to-equity ratio (0.33), lower than GOCL (0.84), indicating better financial stability.

Asset Turnover: Solar’s asset turnover (1.16) is lower than Keltech’s (2.1), which indicates that Keltech is more efficient in utilizing its assets.

Solar Industries stands out for its superior profitability and returns, though its premium valuation suggests high market expectations. Despite a decline in revenue, its strong margins and low debt position it well compared to its peers.

Financial Strength

Despite making large investments, Solar has managed to keep its finances strong:

- Debt-to-OPBDIT ratio remains under 1x, showing good debt control

- Interest coverage was 13.6x in FY24 and 15.6x in H1FY25

- PAT to Operating Income reached 17.6% in H1FY25

- Leads with the highest ROCE (31.03%) and ROE (29.59%)

- The company holds an ICRA A1+ credit rating for three years in a row.

Risks and Challenges

While Solar Industries has delivered impressive growth, a few key risks remain that investors should monitor closely:

- The company fell short of its 30% revenue growth guidance for FY25, largely due to sluggish domestic demand. In a recent management update, Solar acknowledged this shortfall and noted that growth may vary by 5–10%, especially in the near term.

- Long-cycle defense contracts, such as the Pinaka rocket systems, often span 8–12 years, which can delay revenue realization and impact short- to medium-term financial visibility.

- The company’s growing export footprint, while promising, introduces currency fluctuations, geopolitical exposure, and varying international defense budgets, all of which can affect order flow and margins.

Despite these headwinds, Solar Industries maintains a strong balance sheet, robust interest coverage, and a well-diversified order book. Its forward-looking investments, such as the ₹12,700 crore Nagpur defense hub, reinforce the company’s ability to manage risks while staying aligned with long-term growth opportunities.

Read Also: Indian Stock Market Reaction To Wars, Conflicts, And Terror Attacks: A Look Since 1990

Final Thoughts: A Key Player in India’s Defence Future

From humble beginnings as a supplier of mining explosives, Solar Industries has evolved into a leader in India’s defense manufacturing sector. With its broad product range and strong financials, the company is playing a central role in India’s push for defense self-reliance.

For long-term investors looking for growth in India’s strategic sectors, Solar Industries is a shining example of success.