![]()

Every Indian middle-class family eventually faces one big financial question: Should I invest my savings in gold or the stock market? For decades, this has been a subject of debate at dining tables, on WhatsApp family groups, and in investment meet-ups. Parents often favor gold for its security, while younger professionals boast about their stock market returns. But when you look at real numbers, the choice isn’t so simple. Let’s break it down with facts, examples, and practical insights to help you decide wisely.

Two Opposing Investment Beliefs

Gold: The Age-Old Safe Asset

Gold has been India’s preferred investment for generations. It carries cultural weight, is tangible, and provides a sense of financial security. Take this for perspective: gold priced at just ₹200 per 10 grams in the 1970s has climbed to nearly ₹1,07,740 by September 2025.

Stocks: The Modern Engine of Growth

In contrast, equities—represented by benchmarks like the Nifty 50—mirror India’s economic progress. These stocks include leading companies such as Reliance, Infosys, and HDFC Bank. Investing here means owning a share of India’s corporate growth story.

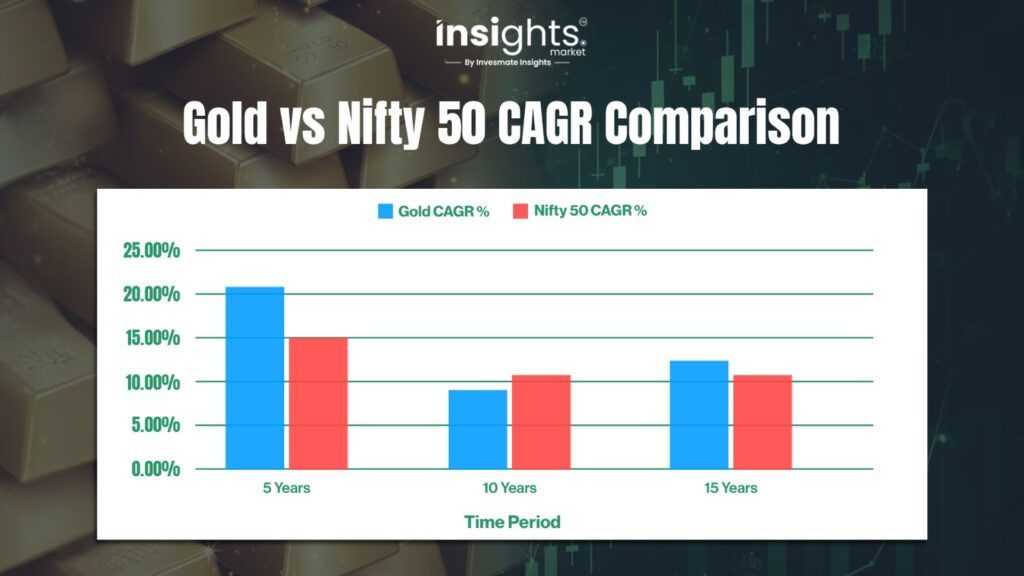

Gold vs. Nifty 50 CAGR Comparisons: What the Numbers Really Tell Us

10-Year Snapshot

Gold: 9.47% CAGR

Nifty 50: 11.2% CAGR

Over the past decade, the Nifty has outperformed! But when we see the time around the pandemic…

5-Year Performance

Over the past five years, gold investors had the upper hand:

Gold: 22.13% CAGR

Nifty 50: 15.22% CAGR

Gold beat equities by a wide margin of nearly 7 percentage points annually.

15-Year Horizon

Stretching further back:

Gold: 13.11% CAGR

Nifty 50: 11.07% CAGR

But we see ₹1 lakh investment made in August 2015 would today be around :

Gold ETF : ~₹3,53,531 (13.46% CAGR)

Nifty 50 TRI : ~₹3,58,548 (13.62% CAGR)

That’s just a ₹5,017 difference over ten years—surprisingly close.

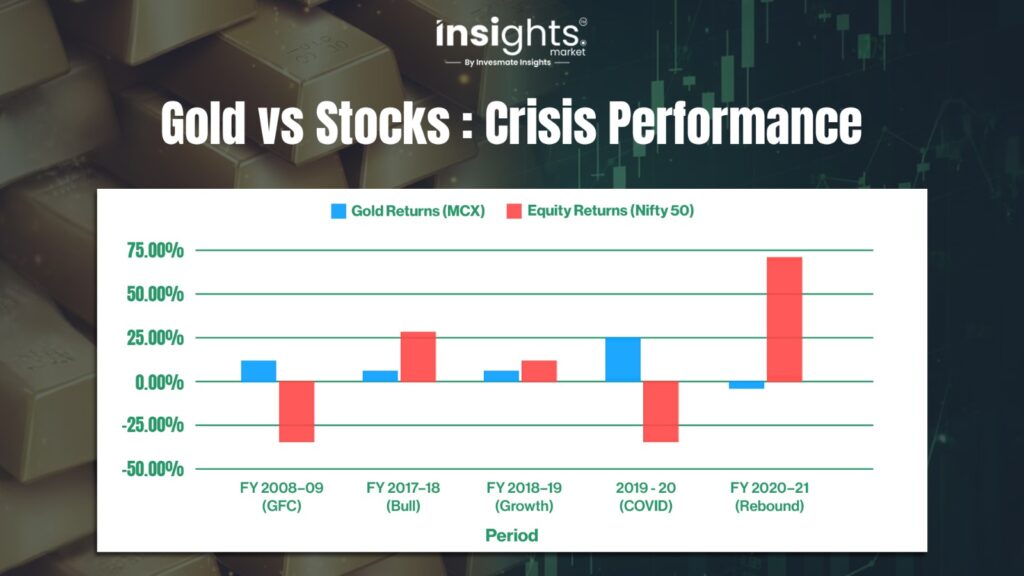

When Each Investment Outperforms

Gold’s Strong Phases

Gold tends to shine during:

- Economic turmoil (2008 crisis: Gold +16% vs. Nifty -36 %)

- Health scares (COVID-2020: Gold +27% vs. Nifty -38% at first)

- Inflationary times

- Currency weakness

Stocks’ Winning Periods

Equities lead during:

- Economic expansion (2017: Nifty +28.65% vs. Gold -1.6%)

- Strong corporate earnings cycles

- Low-interest-rate environments

- Technology booms

The Global Gold Fever: Why 2025 Feels Like Déjà Vu, But Bigger

Something unusual is happening in the age-old “gold vs. stocks” tug-of-war: we’re in the middle of a worldwide gold obsession. And this isn’t just about aunties at jewelry stores. Think bigger. Russia and China aren’t merely buying gold—they’re stacking it like there’s no tomorrow. Even our own RBI is flexing, having bought in the last few months what it usually scoops up in an entire year.

So why is everyone suddenly romancing gold? Enter the “dollar-plus-one” strategy. Big economies don’t want to keep all their eggs in the US dollar basket anymore. Gold is their shiny backup plan. When global powers hoard it, ordinary investors take notice—and FOMO kicks in.

Why Gold Has Its Spotlight Right Now

- Festival Frenzy: Only in India can weddings, Diwali, and Karwa Chauth double as a demand booster for bullion. History shows that during October–December, gold prices almost always catch a festive high.

- Bye-Bye FD Charm: RBI’s rate cuts have made fixed deposits look as exciting as soggy toast. With returns barely beating inflation, the middle class is naturally drifting toward gold, which has historically averaged 10–12% gains.

- Crisis Magnet: Wars, trade disputes, political drama—you name it. Whenever the world feels shaky, gold steps in as the emotional support asset. Right now, uncertainty is basically its best marketing team.

Still, investors must remember: gold rallies during uncertainty but often underperforms when stability returns. The smart play is balance—not betting everything on one asset.

Middle-Class Realities

SIP Illustration

A ₹5,000 monthly SIP for 10 years would result in:

- Gold fund (12% returns): ~₹11.6 lakh

- Nifty index fund (13% returns): ~₹12.3 lakh

Starting Small

The good news? You don’t need huge amounts to begin:

Gold ETFs: Buy from just 1 gram (~₹10,774 today)

Gold mutual funds: SIPs from ₹500

- Nifty index funds: Start with ₹500–1,000

Now the next part is Taxation! This is where things get technical, but it’s crucial for your returns:

Taxation: What You Keep

Advantage: Equities, especially long-term.

So, who is the winner on taxes?

Stocks have a slight edge, especially for long-term investors.

Example of a Smart Portfolio Mix

Financial planners suggest gold should only be part of a broader strategy:

- Conservative: 5–7% in gold

- Moderate: 7–10% in gold

- Cautious/risk-aware: Up to 15% in gold

Adjusting to Market Cycles

- During Uncertainty: Raise gold share around 10–15%, prefer ETFs or Sovereign Gold Bonds(Inactive presently). Keep equity SIPs running.

- During Growth Phases: Cut gold around 5–7%, tilt more towards equities and sectors driving expansion.

Mistakes to Avoid (Stay Cautious!)

With Gold

- Paying high making charges for jewelry

- Trying to time the market

- Over-allocating (>20% of portfolio)

With Equities

- Panic selling in downturns

- Chasing past performance

- Skipping SIPs during volatility

Best approach: Don’t pick one side—use both in combination.

P.S.: This blog is purely based on information. Not Investment Advice!

Bottom Line

The real dilemma isn’t about choosing gold or stocks. It’s about how both can complement each other to create a portfolio that weathers volatility while building wealth. Smart investors don’t take sides—they diversify.

What’s your take on this eternal debate? Are you team gold, team stocks, or team “smart diversification”? The numbers suggest that the wisest investors might just be playing for both teams.

FAQs

Ans. Both gold and stocks can be good long-term investments, but they serve different purposes. Gold provides stability during uncertainty, while stocks generate higher wealth during growth cycles. A balanced portfolio with both is usually recommended.

Ans. Yes, over the last 5 years, gold delivered a CAGR of 22.13%, while the Nifty 50 returned 15.22%. However, over 10 years, the difference between gold and stocks was very small.

Ans. Gold has cultural significance, is tangible, and is seen as a safe-haven asset. Many families feel more secure holding physical gold than investing in stock markets, which are considered risky.

Ans. Financial experts recommend 5–15% allocation to gold, depending on your risk profile. Conservative investors may prefer higher gold exposure, while younger investors can keep it lower.

Ans.

- Gold ETFs: From 1 gram (~₹10,774 as of Sept 2025)

- Gold mutual funds: SIPs from ₹500

- Nifty index funds: SIPs from ₹500–1,000

Ans. Yes. Gold is taxed at 12.5% for long-term holdings (more than 3 years), while stocks are taxed at 10% on gains above ₹1 lakh if held for more than a year. Stocks generally enjoy a tax advantage.

Ans. Gold usually outperforms during economic crises, inflationary periods, currency depreciation, and geopolitical uncertainty. Stocks, however, shine during periods of economic growth and strong corporate earnings.

Ans. Gold ETFs and Sovereign Gold Bonds are better options than physical gold for investment. They have no making charges, are easier to sell, and provide tax benefits in some cases.

Ans. Yes, you can start SIPs in gold mutual funds or ETFs as well as in index funds or equity mutual funds. SIPs allow small, consistent investments that reduce risk over time.

Ans. A practical portfolio could be 70–80% in equities, 10–20% in gold, and 10–20% in debt instruments. This balance offers both stability and growth potential.

The information provided in this reference is for educational purposes only and should not be considered investment advice or a recommendation. As an SEBI-registered organization, our objective is to provide general knowledge and understanding of investment concepts.

It is recommended that you conduct your own research and analysis before making any investment decisions. We believe that investment decisions should be based on personal conviction and not borrowed from external sources. Therefore, we do not assume any liability or responsibility for investment decisions made based on the information provided in this reference.