![]()

India has signed its first structured LPG import deal with the US. The country will purchase 2.2 million tonnes of cooking gas each year, which is about 10% of all of India’s LPG imports, starting in 2026. This deal represents a significant change after 75 years of almost complete dependence on the Middle East.

Why India Suddenly Needs US LPG?

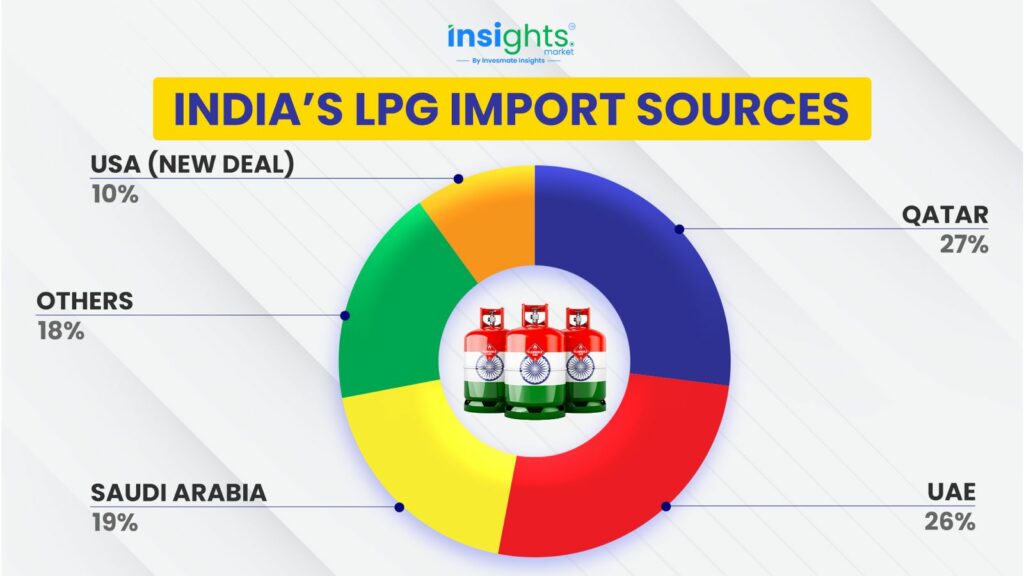

India relies on imports for 60% of its LPG needs. If supplies are disrupted, millions of stoves go cold.

Until now, the situation was straightforward: Qatar, UAE, and Saudi Arabia supplied over 70% of our LPG.

However, the Middle East has become risky. In 2024, there were tanker attacks in the Red Sea and rising tensions between Israel and Iran, along with unpredictable oil markets. These crises increased global LPG prices, and India could only absorb the costs through subsidies.

The government’s solution? is to diversify and find a new, stable supplier located far away.

The USA Enters India's LPG Market

Under the deal signed in November 2025:

- What: 2.2 million tonnes per year (MTPA) of LPG

- When: Starting in 2026 (initial one-year contract)

- Who Buys: Indian Oil (IOC), BPCL, HPCL

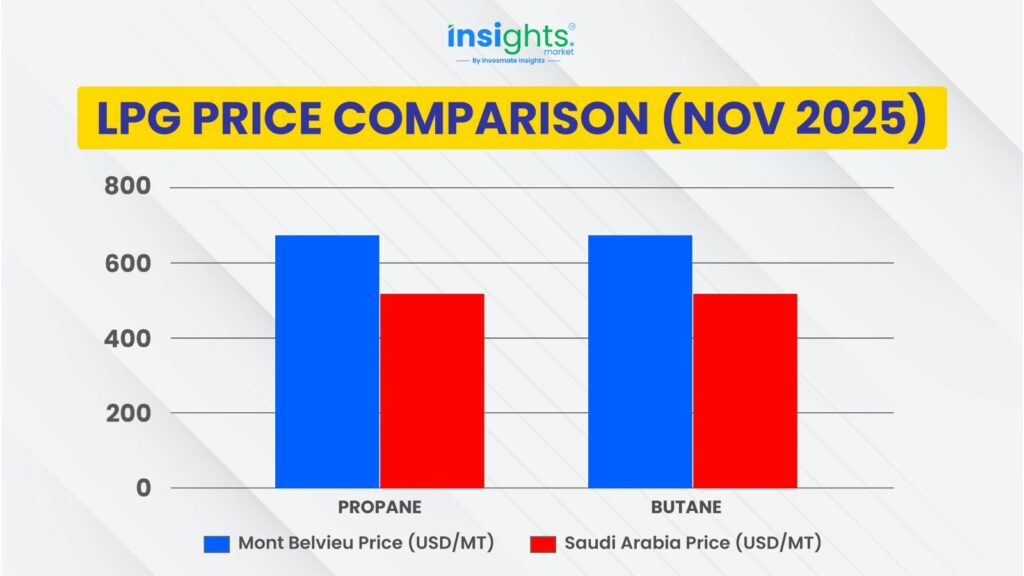

- Price Benchmark: Mont Belvieu (Texas), the largest LPG trading hub in the world

- Value: About ₹2,000 crore annually

Why Mont Belvieu? It is the reference price that sets global LPG standards. Unlike the Middle East, which uses the Saudi CP (Contract Price), Mont Belvieu relies on spot-market prices, offering real-time and transparent pricing. Historically, Mont Belvieu propane is cheaper than Saudi alternatives, giving India better rates.

The Good: Why This Deal Works

1. Price Savings (Maybe)

US LPG is usually $0-$30 cheaper per tonne compared to Middle Eastern supplies. If this trend continues and volumes increase, India could save hundreds of crores each year. BPCL’s finance head noted potential net gains of $0-$30 per tonne.

2. Supply Security

India will no longer depend on a single region. If tensions in the Red Sea escalate again, India has a backup plan. The USA is politically stable and has the largest liquefaction capacity in the world at 15.4 Bcf/d.

3. Geopolitical Shield

This deal also suggests a larger trend: stronger India-US energy ties. It’s about more than just LPG; it positions India as a strategic energy buyer, which reduces the power of any single supplier.

4. Better Bargaining Power

Having two competing suppliers allows for better negotiation. Qatar, UAE, and Saudi Arabia will know that India now has options. As a result, expect sharper pricing from them.

The Bad: Why This Deal Isn't Magic

1. The Propane-Butane Mismatch

US LPG consists of 80% propane and 20% butane, while India needs 60% butane and 40% propane. This difference arises from different usage patterns in the US and India.

The solution? India will import extra butane-rich cargoes from the Middle East or blend materials sourced domestically. This blending will incur costs, which may reduce potential savings by 5-10%.

2. Longer Distance, Higher Logistics

The US Gulf Coast is further away, leading to higher shipping costs. Additionally, the rupee is weakening against the dollar, making US imports more expensive in rupee terms. That ₹30-35 per tonne advantage could disappear with increased freight and currency challenges.

3. Infrastructure Isn't Ready

US cargoes arrive in Very Large Gas Carriers (VLGCs), but India’s LPG terminals are equipped for Medium Gas Carriers (MGCs). We will need to upgrade our terminals to handle VLGC turnarounds.

How long will this take? Expect 2-3 years for major infrastructure projects. Until these upgrades are complete, unloading delays will lead to higher costs.

4. Subsidy Crisis Doesn't Disappear

The government approved ₹30,000 crore to reimburse IOC, BPCL, and HPCL. However, they still lack ₹23,700 crore. Each winter month, losses grow. While US LPG helps marginally, it does not address the fundamental issue: the government maintains low cylinder prices to protect low-income households.

Who Actually Wins? (Stock Market Angle)

Oil Marketing Companies (IOC, BPCL, HPCL): Mixed Outcome

In the short term, the ₹30,000 crore subsidy inflow (12 payments starting in November 2025) will improve cash flow and working capital, likely enhancing dividends.

In the medium term, if US LPG stabilizes prices, their margin losses could diminish. However, as long as the government keeps prices regulated, the subsidy issue will persist.

Risk: Winter spikes might still require new government bailouts. This is a political problem, not an economic one.

Pure Refiners (MRPL, CPCL): Real Winners

Companies focused only on refining, not LPG sales, will benefit most. In a low crude price environment ($62-64 per barrel versus $85 last year), their refining margins improve significantly. Without subsidy issues, these stocks may have better upward potential.

Geopolitical Play

The larger picture? The India-US energy partnership is growing. If successful, it could lead to LNG deals, coal sourcing, and even cooperation in renewable energy. This is a major growth theme for energy stocks.

The Critical Questions Nobody's Asking

Will This Become a Multi-Year Deal?

Commerce Minister Piyush Goyal hinted at Phase 2 discussions after November 2025. Long-term US LPG deals with fixed prices could be on the horizon. If volumes rise to 15-20% of imports by 2028, the savings narrative could change significantly.

What If Red Sea Disruptions End?

If tensions in the Middle East ease, the urgency for US LPG may diminish. Prices could drop, making the US deal less important.

Will Consumers See Lower Cylinder Prices?

This is what every household wants to know. Unfortunately, the answer is likely no. Thanks to PMUY, over 10 crore families already receive subsidized cylinders at ₹300-550 each. Others pay ₹850 or more. The savings from US LPG will help lower the government’s subsidy burden, not benefit consumers directly.

What's Next? (The 2026 Game Plan)

- Q4 2025–Q1 2026: Initial cargoes arrive, and infrastructure testing begins.

- Mid-2026: Analysts will evaluate whether blending costs, logistics, and currency challenges have delivered the promised savings.

- H2 2026: Formal Phase 2 trade talks will begin. Multi-year LPG deals may be announced.

- 2027–2028: Upgrades to terminals will be complete, allowing for standard handling of VLGCs.

The Real Takeaway

This deal is strategically important but only modestly impactful in economic terms for the moment. It won’t immediately change LPG prices. It reduces geopolitical risk, increases negotiating power, and shows that the India-US energy partnership is deepening.

For investors: OMC stocks will see short-term upside from subsidies and medium-term stabilization in margins. Pure refiners offer cleaner growth opportunities. The real chance lies in supporting India’s energy security from a broader perspective.

For consumers: Don’t expect significant drops in cylinder prices. Any savings will support the government’s decreasing subsidy load.

One-line summary: India has reduced its risk from the Middle East. It’s not revolutionary, but it’s necessary.

What Should Be Your Next Move?

If you're a retail investor in the energy sector:

- Watch IOC/BPCL/HPCL for subsidy announcements—each quarter is important.

- Monitor MRPL and CPCL for improvements in refining margins.

- Keep an eye on announcements about Phase 2 trade deals—they will be key for stock movements.

If you're a trader:

- Expect volatility in OMC stocks around subsidy news.

- Pure refiners might outperform in a low-crude-price environment.

If you're just worried about household gas prices:

- Your cylinder costs probably won’t drop significantly in 2026.

- However, the risk of supply disruptions is now lower—that’s the real advantage.

So, what is your view on this? Drop them in the comments. This is just the first part of India’s energy diversification story.

FAQs

Probably not immediately. While US LPG could save ₹0-30 per tonne, that savings won’t reach your cylinder bill. Why? Because the government keeps PMUY cylinder prices fixed at ₹500-550 through subsidies. Any price benefit will reduce the government’s subsidy burden, not lower what you pay. Non-PMUY users might see a slight dip if competition pushes domestic rates down, but don’t expect dramatic changes in 2026.

It’s not always more expensive. Right now, US LPG is competitive because China (the world’s largest importer) has temporarily reduced buying. This flooded US markets with surplus supply, dropping prices. India grabbed the opportunity. If China resumes normal imports, US prices could spike again. So this deal works only because of a temporary market glitch—not because the US is structurally cheaper.

US LPG is 80% propane (used in cars and heating). India needs 60% butane (for cooking stoves). So Indian refiners will need to blend US propane with Middle Eastern butane or buy extra butane elsewhere. This blending costs money and eats into savings—potentially offsetting 5-10% of any price advantage. Infrastructure changes at terminals will take 2-3 years.

No. This is just 10% diversification. Qatar, UAE, and Saudi Arabia will still supply 70%+ of India’s LPG. The Middle East isn’t going anywhere. This deal is a hedge—a backup plan if Red Sea tensions, tanker attacks, or geopolitical shocks happen again. It’s not a replacement; it’s an insurance policy.

Marginally. The government is currently ₹23,700 crore short of covering OMC losses even after allocating ₹30,000 crore. US LPG could theoretically save 5-8% through better pricing, but that’s only ₹2,000-3,000 crore annually. The subsidy crisis won’t disappear—it’s a political problem (keeping poor households warm), not just an economic one. Winter demand will still force fresh government bailouts.

Modest gains, not dramatic. OMC stocks got an immediate boost from the ₹30,000 crore subsidy announcement, not this US deal. Medium-term, if diversification stabilizes margins and reduces under-recoveries, stock upside exists. But the real winners are pure refiners like MRPL and CPCL—they don’t have subsidy losses, just refining margins. Watch for subsidy announcements every quarter; those move OMC stocks more than this US deal.