![]()

Imagine a world where every sports match, award show, or political debate streams seamlessly across devices. Behind this ecosystem sits Amagi Media Labs, a cloud-based media technology firm that enables broadcasters and content owners to distribute and monetize content globally. The company entered the public markets today on January 13, 2026.

IPO Details (Structured Overview)

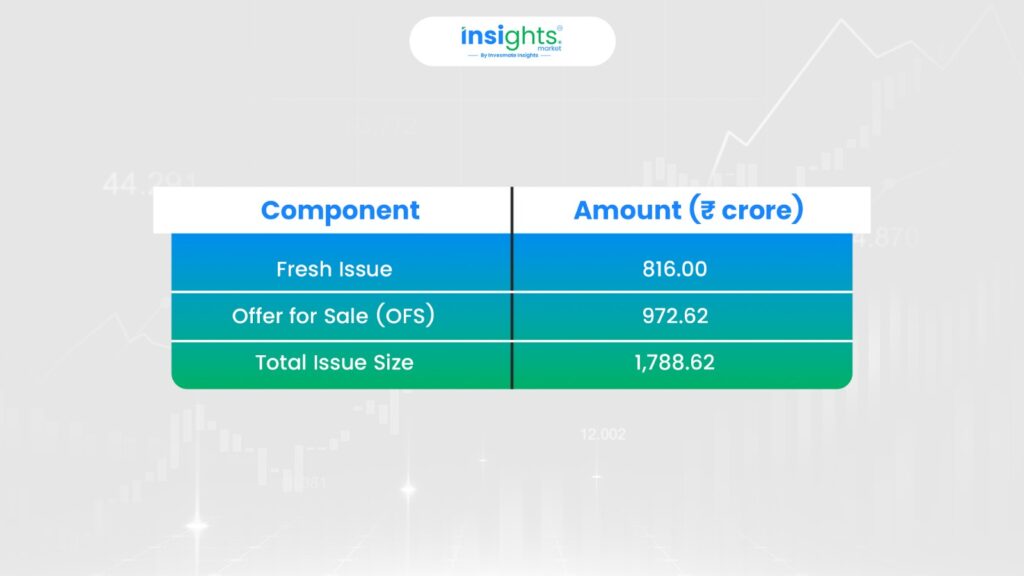

Issue Size & Structure

OFS exceeding the fresh issue indicates partial exits by existing shareholders.

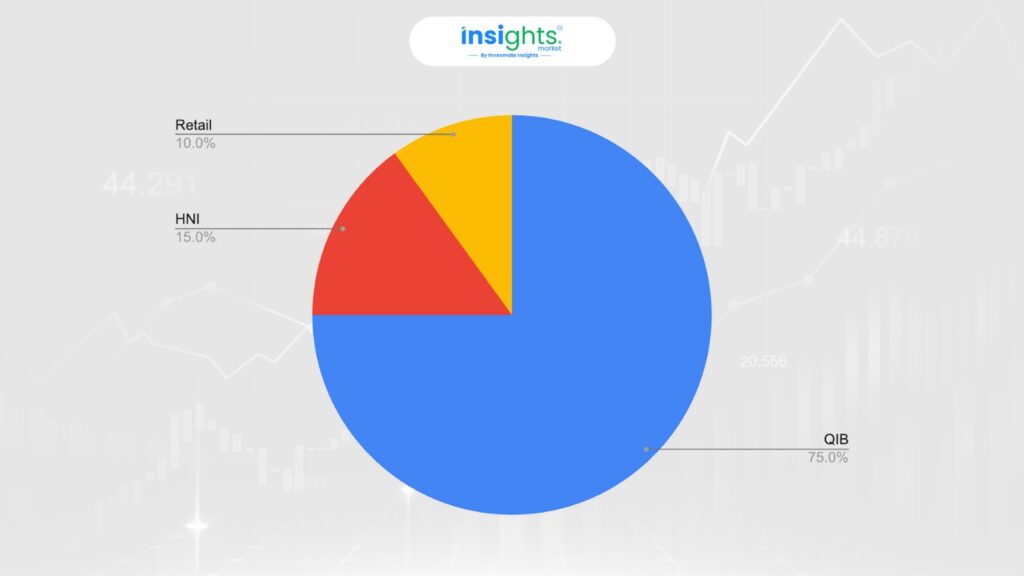

Investor Quota

The heavy allocation to QIBs (75%) means institutional investors will have priority. For retail investors, the only 10% quota means the chances of getting full allotment are relatively lower, especially if the IPO is oversubscribed.

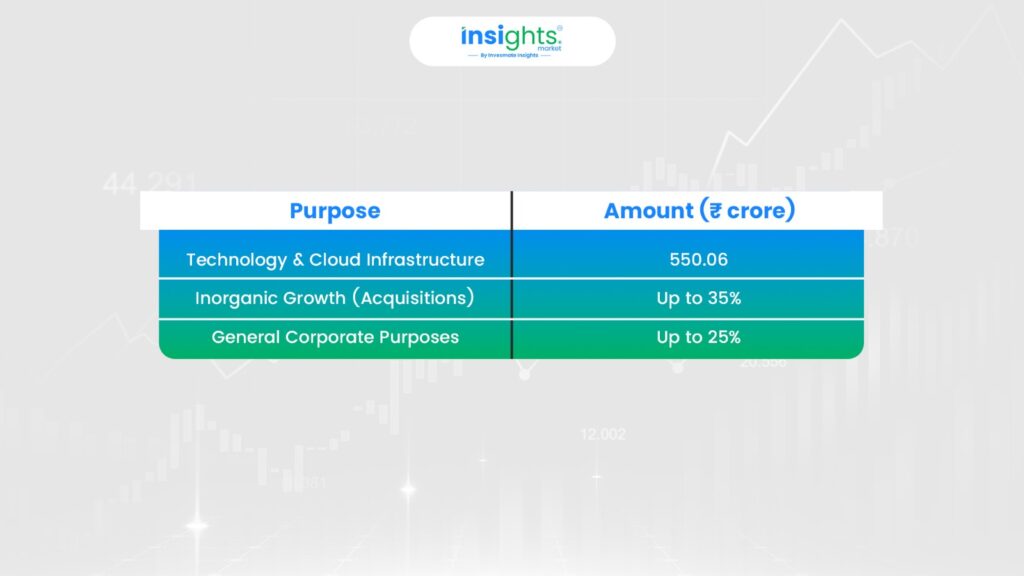

Use of IPO Proceeds

The allocation of ₹550.06 crore (67% of fresh issue) toward technology and cloud infrastructure makes sense for a SaaS company. This capital will be invested in expanding the company’s cloud capacity, improving product capabilities, and building AI-driven features. The remaining amount will be used for acquisitions and general operations.

Business Overview

Founded in 2008 and headquartered in Bengaluru, Amagi operates a SaaS platform across broadcasting, streaming, and digital advertising. The company earns revenue via subscriptions and advertising monetization, creating a recurring, usage-linked revenue model.

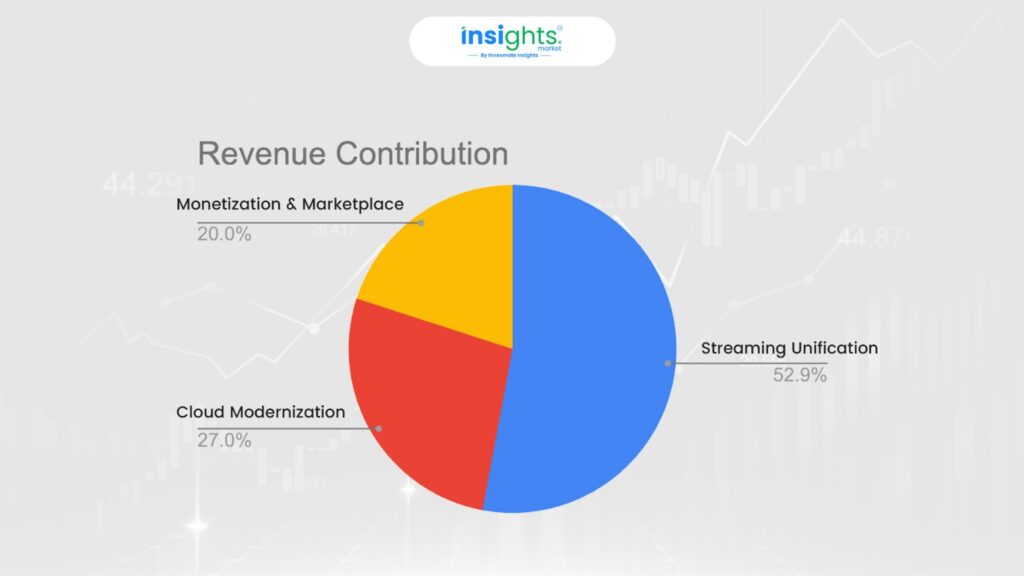

Core Business Segments (Revenue Mix)

(Streaming Unification is the primary growth driver, especially for FAST channels.)

Key Products

- Cloudport – Channel playout & distribution

- Thunderstorm – Server-side ad insertion

- Amagi Planner – AI-driven scheduling & analytics

These platforms have supported global events including the 2024 Paris Olympics, UEFA tournaments, and US Presidential Debates.

Financial Performance: The Story of Turnaround

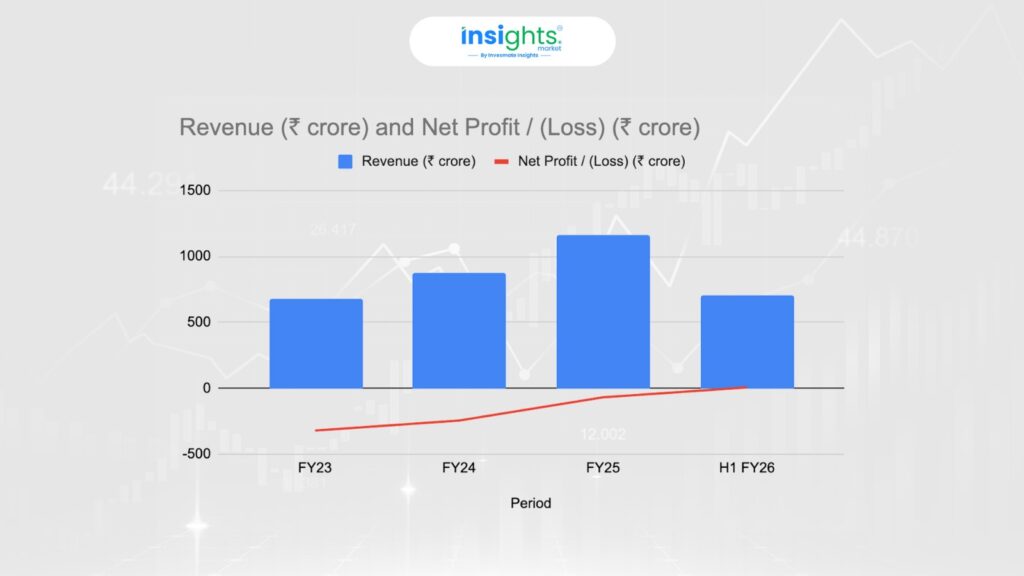

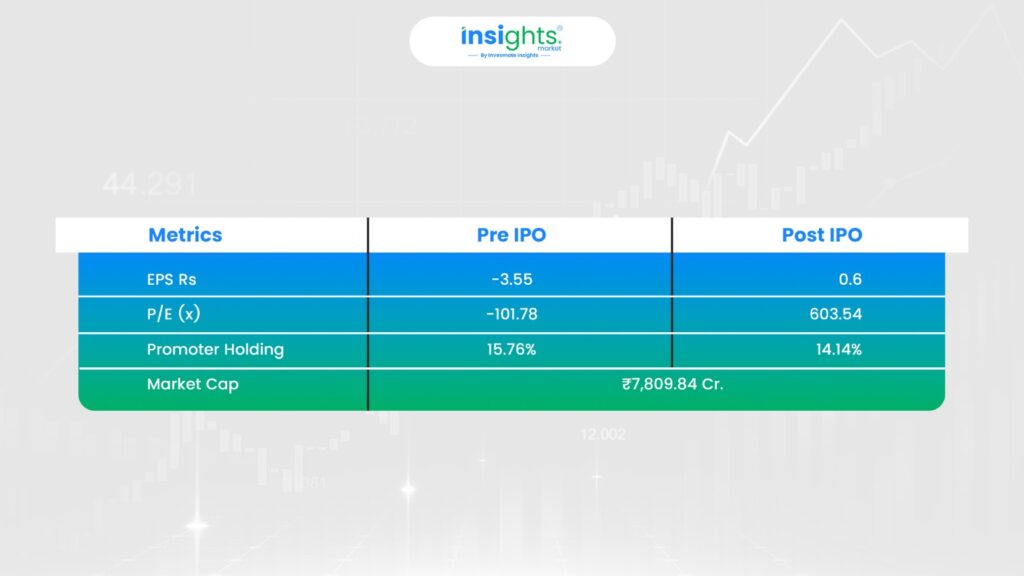

Amagi has delivered a strong revenue growth trajectory, recording ~30% CAGR from FY23 to FY25. Revenue increased from ₹680.56 crore in FY23, when the company reported a net loss of ₹321 crore. In FY24, revenue rose to ₹879.15 crore, while losses narrowed to ₹245 crore, reflecting a ~24% year-on-year reduction. FY25 saw further scale-up, with revenue reaching ₹1,162.64 crore and net losses compressing sharply to ₹68.7 crore. The turnaround became visible in H1FY26, with ₹704.82 crore revenue generated in six months and a net profit of ₹6 crore.

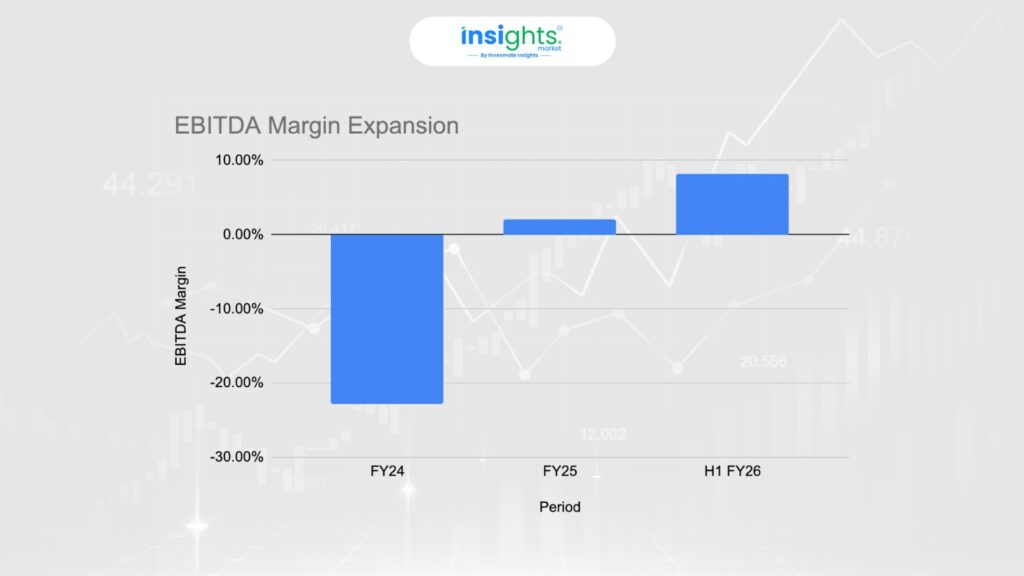

What makes the recent profitability noteworthy is the improvement in EBITDA margins. The company moved from a negative EBITDA margin of -22.86% in FY24 to a positive 2.02% in FY25, and impressively jumped to 8.26% in H1FY26. This indicates that as the company scales, its operational efficiency is improving dramatically.

However, here’s the critical point: profitability is still nascent. The company went from significant losses to just ₹6 crore profit in six months. If we annualize this, it translates to approximately ₹12-13 crore annual profit on ₹1,400+ crore revenue—a mere 1% net margin. This means any adverse conditions, increased customer acquisition costs, or regulatory challenges could push the company back into losses.

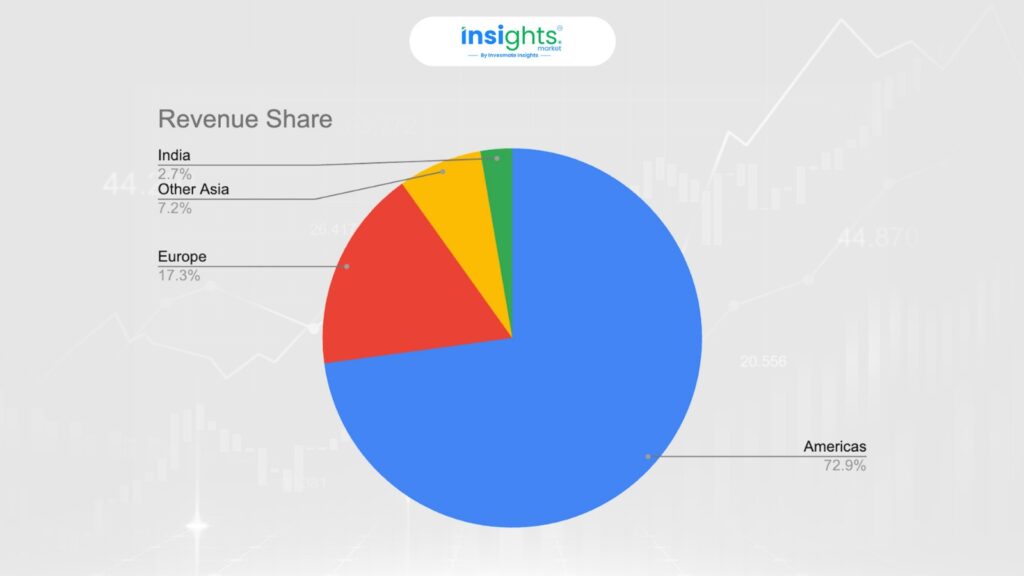

Geographic Revenue Concentration

Heavy dependence on the US market remains a key variable.

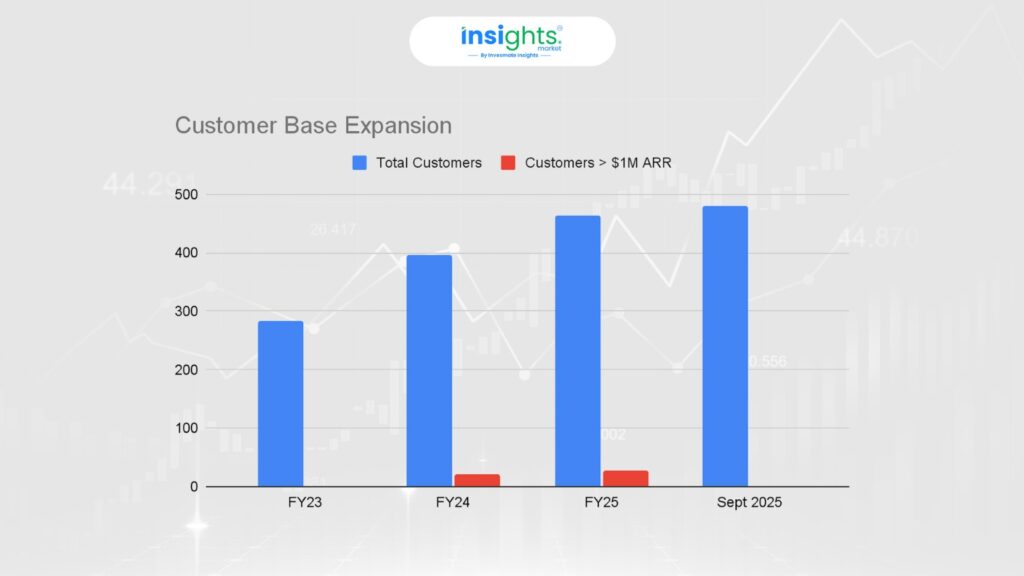

Customer Growth Trend (FY23 to Sept 2025)

As of September 2025, Amagi served 481 customers, up from 283 in FY23, representing an increase of nearly 70% over two years. Alongside overall customer growth, the number of high-value customers generating more than $1 million in annual recurring revenue increased from 22 in FY24 to 28 in FY25, indicating improving customer quality and deeper enterprise adoption.

Opportunities & Risks

Key Opportunities

- Structural shift from cable TV to cloud & FAST channels

- Scalable SaaS economics with improving margins

- Strong expansion-led customer retention

- AI-led monetization and scheduling tools

Key Risks

- High geographic concentration in the Americas

- Customer concentration (Top 10 = 33.74% of revenue)

- Streaming Unification dependency (52.86% of revenue)

- Very recent profitability track record

Valuation Snapshot

Grey Market Premium (GMP)

GMP Date | IPO Price | GMP | Estimated Listing Price |

13-01-2026 | 361 | ₹17 | ₹378 (4.71%) |

12-01-2026 | 361 | ₹20 | ₹381 (5.54%) |

11-01-2026 | 361 | ₹37 | ₹398 (10.25%) |

Bottom Line

Amagi Media Labs sits at the convergence of cloud infrastructure, OTT streaming, and digital advertising. Revenue growth has been strong, margins are improving, and customer expansion metrics are healthy. At the same time, profitability is recent, revenue concentration is high, and valuation leaves limited room for execution errors.

However, the IPO opens at a valuation that leaves little room for disappointment. The company’s profitability is recent and fragile, its exposure to the U.S. market creates geopolitical risk, and its dependence on a few large customers adds uncertainty.

FAQs

The Amagi Media Labs IPO opens for subscription on January 13, 2026, and closes on January 16, 2026. The shares are scheduled to be listed on January 21, 2026, subject to final allotment.

The IPO price band is fixed at ₹343–₹361 per share. Retail investors must apply for a minimum of 1 lot (41 shares), translating to a minimum investment of ₹14,801 at the upper price band.

Amagi Media Labs is raising ₹1,788.62 crore through the IPO, comprising a fresh issue of ₹816 crore and an offer for sale (OFS) of ₹972.62 crore. The fresh issue proceeds will primarily be used for technology and cloud infrastructure expansion, potential acquisitions, and general corporate purposes.

Amagi Media Labs turned profitable in H1 FY26, reporting a net profit of ₹6 crore, after several years of losses. While EBITDA margins have improved significantly, overall profitability is still at an early stage and remains modest at the net level.

In FY25, approximately 72.86% of Amagi’s revenue came from the Americas, primarily driven by higher adoption of FAST channels and digital advertising in the US market. Europe contributed 17.27%, while India and other Asian markets together accounted for less than 10%.

Key risks include high geographic revenue concentration in the Americas, dependence on a few large customers, recent and limited profitability history, and reliance on the Streaming Unification segment, which contributes over 50% of total revenue.

The information provided in this reference is for educational purposes only and should not be considered investment advice or a recommendation. As an SEBI-registered organization, our objective is to provide general knowledge and understanding of investment concepts.

It is recommended that you conduct your own research and analysis before making any investment decisions. We believe that investment decisions should be based on personal conviction and not borrowed from external sources. Therefore, we do not assume any liability or responsibility for investment decisions made based on the information provided in this reference.