![]()

The Nifty is down 8%. Your WhatsApp is buzzing. Finfluencers are quoting Buffett. But before you act, there’s one number you need to check first — and it has nothing to do with the Nifty itself.

−8%

NIFTY FALL

SINCE FEB 27

~103

BRENT CRUDE

MAR 2026

₹25L Cr

WEALTH WIPED

IN DAYS

5,000%

“BUY THE DIP”

SEARCH SURGE

A War. An Oil Shock. And Everyone Became an Expert Overnight.

On February 28th, the US and Israel launched joint airstrikes on Iran. Within hours, Iran halted traffic through the Strait of Hormuz — the narrow waterway through which 20% of the world’s oil flows every single day.

Brent crude briefly touched $120. ₹25 lakh crore vanished from Indian markets in a matter of days. And Google searches for “buy the dip” surged nearly 5,000% across India.

Here’s the uncomfortable truth: most people who say it don’t actually understand what they’re saying.

Because in India — a country that imports 89% of its crude oil — a market dip doesn’t exist in isolation. It lives inside a macro environment almost entirely controlled by one variable. And right now, at ~$103 a barrel, that variable is flashing warning signs most retail investors are choosing to ignore.

Every $10 Rise in Crude Triggers the Same Chain Reaction — Every Time

India nets roughly 4.5–5 million barrels of oil imports per day. At that scale, a $10 per barrel rise isn’t a line item — it’s a macro event. Research from SBI, ICRA, and Axis Securities has mapped the transmission precisely. The cascade runs automatically, without exception, every single time crude rises:

At ~$103 today — briefly $120 at peak Hormuz panic — India sits firmly in what analysts call the macro stress zone: inflation rising, current account deficit widening, the rupee under pressure, the RBI holding rates or hiking. This is the fundamental backdrop against which you’re deciding whether to “buy the dip.”

What History Actually Says About Buying When Wars Begin

A 2015 University of Zurich study examined stock markets across every major conflict since World War II. The finding cuts against popular instinct: markets fall hardest when war seems likely — once it actually starts, uncertainty begins to clear, and markets often stabilize. The real enemy is not the war itself. It is the uncertainty leading up to it.

But there’s a critical caveat. When wars erupt without warning — as this one did on February 28th — markets often find their actual floor later, not in the opening week of headlines. March 9th’s brief Nifty recovery, followed immediately by another leg down, was a textbook example. Historical data shows the Sensex has delivered average 6-month forward returns of ~38% from genuine crisis lows — but measured from real panic bottoms, not from overvalued markets that simply corrected 8%.

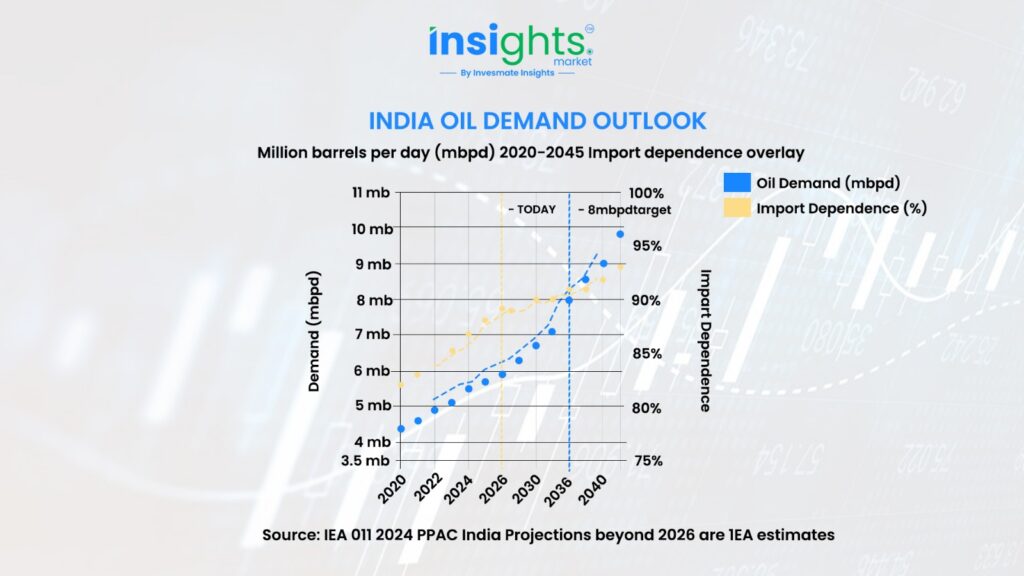

The long game matters here. India’s oil demand is projected to jump from 5.5 to 8 million barrels per day by 2035 — making India the world’s fastest-growing oil market. Import dependence will likely hit 90–92% by 2035.

EVs, ethanol blending, and strategic reserves soften the blows.None of them remove crude from the equation. This dynamic is why getting your oil-price-zone playbook right is a multi-decade skill, not just a war-week tactic.

Your Actual Playbook — Tied Directly to Where Crude Is Trading

“Buy the dip” is not one strategy. It is four completely different strategies depending on a single number: where Brent crude is sitting right now.

$50 – $65 / bbl

ZONE 01 · LOW OIL · BUY BROADLY

Go broad. Almost every dip is a genuine gift.

Inflation tamed, rupee stable, RBI cutting. Load up on aviation, autos, paints, financials, logistics. Avoid ONGC / Oil India — upstream earnings weaken directly.

$65 – $90 / bbl

ZONE 02 · GOLDILOCKS · BALANCED

India’s ideal macro backdrop. Broad dip-buying works.

Reliance earns optimal margins, OMCs are stable, and inflation is manageable. Any Nifty or diversified MF dip here is a genuine entry across the board.

$90 – $120 / bbl

ZONE 03 · HIGH OIL · WE ARE HERE

Selective only. Broad buying is dangerous here.

In Focus: ONGC, Oil India, IT exporters, pharma, renewables.

Avoid: Airlines, OMCs, autos, paints, consumer names.

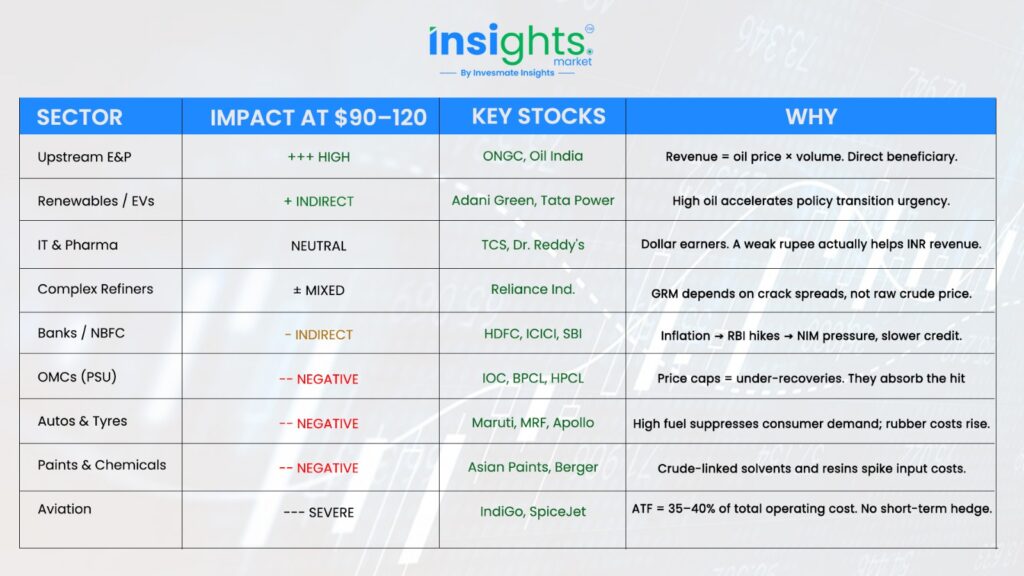

Who Wins, Who Bleeds — The Complete Stock Market Breakdown

The Nifty Oil & Gas index is 60%+ Reliance Industries by weight — watching it gives a completely distorted picture.

Here’s the real sector-by-sector breakdown of who benefits from high crude and who gets crushed. The visual impact bars show the direction and intensity at Zone 03 (~$103/bbl):

The Two Questions That Separate Investors From Gamblers

01

IS THE DAMAGE TO THIS STOCK’S EARNINGS TEMPORARY OR PERMANENT?

IndiGo is down because aviation fuel — 35–40% of its operating cost — just spiked. That’s arithmetic, not panic. TCS is down because broad fear dragged everything lower. Its actual business is barely touched by Gulf oil routes. Same 10% drop on your screen. Completely opposite trades underneath. Know which one you’re holding before you deploy more capital.

02

CAN YOU AFFORD TO WAIT FOR THE RESOLUTION?

The question is never “will the market recover?” It almost always does. The real question: how long will the pain last, and do you have the patience and financial cushion to sit through it without being forced to sell at the worst moment? Analysts estimate resolution within roughly two months — but nobody knows. Stagger purchases. Don’t bet everything on a single entry point.

And one more thing nobody says loudly enough: where the market was before the dip matters as much as the dip’s size.Indian markets were already overvalued before this war. A 10% fall may simply be a correction toward fair value — not the generational opportunity being sold on social media.

India is building resilience that didn’t exist in past crises. Russian discounted crude now covers 35–40% of imports, ethanol blending is live, strategic reserves are expanding.

None of it removes crude from the equation — it only softens each blow. Crude oil will remain India’s economic heartbeat for at least the next two decades.

So the next time “buy the dip” floods your feed, ask the one question that actually changes your outcome: Which dip? In what? At what oil price? And for how long? That question is worth more than every WhatsApp forward you’ll receive today.

THE BOTTOM LINE

The dip is real. The question is which one — and whether you’re walking into a gift or a trap dressed up as an opportunity.

Check crude first. Identify the cause. Apply the zone filter. And if your original investment thesis hasn’t changed because of a war in the Gulf, the clearest move might simply be to do nothing at all.

FAQs

Crude oil prices directly affect India’s inflation, trade deficit, rupee value, and interest rates. Since India imports nearly 90% of its crude oil, a sharp rise in oil prices can increase costs across the economy and negatively impact many sectors in the stock market.

Higher crude oil prices increase India’s import bill, widen the current account deficit, and push inflation higher. This often forces the RBI to keep interest rates high, which can slow economic growth and hurt stock market sentiment.

Not always. During periods of high crude prices, broad dip buying can be risky. Investors should first understand the macro environment and focus only on sectors that benefit or remain stable when oil prices rise.

Upstream oil companies like ONGC and Oil India benefit because their revenue increases with higher oil prices. IT and pharma companies may also benefit indirectly due to a weaker rupee boosting export earnings.

Airlines, paint companies, auto manufacturers, tyre companies, and PSU oil marketing companies often face higher input costs when crude prices rise, which can hurt profitability.

The Strait of Hormuz is one of the world’s most critical oil shipping routes, with around 20% of global oil supply passing through it daily. Any disruption in this region can quickly push oil prices higher and impact global financial markets.

This article is for educational and informational purposes only. It is not investment advice or a stock recommendation. Investors should conduct their own research or consult a qualified financial advisor before making investment decisions.