![]()

New financial year. New rulebook. Here’s what’s actually changing — and what it means for your money.

April 1 is usually just the start of a new financial year.

This time, it’s different.

From April 1, 2026, the rules that govern how you trade, invest, borrow against your portfolio, and even how your gold fund calculates its NAV — all of it is being rewritten. Not tweaked. Rewritten.

Traders will pay more. Mutual fund investors will likely pay less. Leverage is getting squeezed from both ends. And even if you’ve never bought a single derivative in your life, the new Income Tax Act 2025 and updated SGB rules are going to touch you.

Here’s the complete picture — topic by topic, with what it actually means for your money.

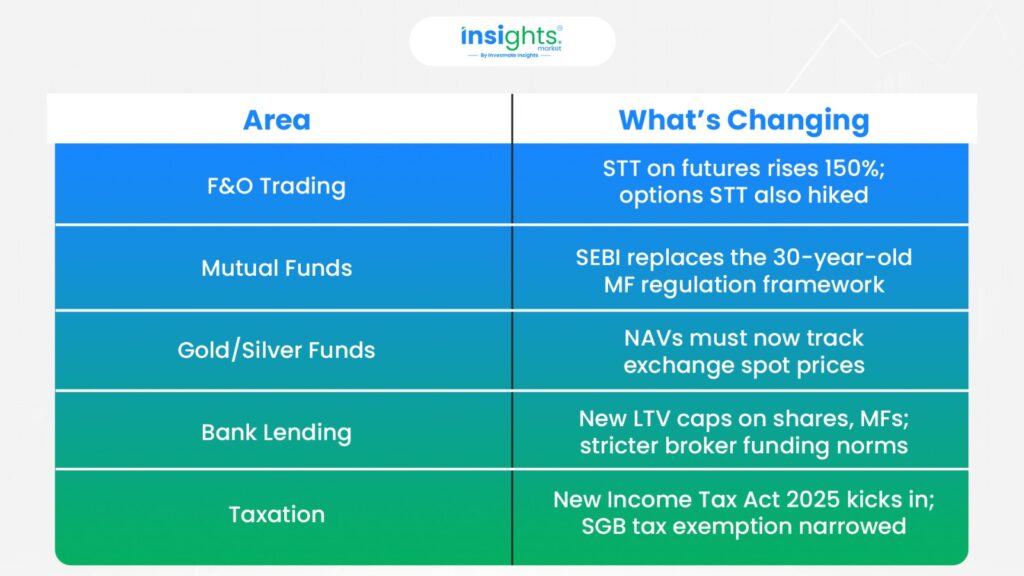

Quick Snapshot: What’s Changing from April 1, 2026

1. F&O Traders: Your Cost Per Trade Just More Than Doubled

If you trade futures, this one stings.

STT (Securities Transaction Tax) on equity futures is jumping from 0.02% to 0.05% of transaction value — a 150% increase, effective for all trades executed on or after April 1, 2026. This comes through Clause 143 of Finance Bill 2026.

Options traders aren’t spared either:

- Options premium STT: 0.10% → 0.15%

- Exercised options STT: 0.125% → 0.15%

To put this in perspective: if you trade 10 lots of Nifty futures daily, your STT outgo on those trades alone rises by 2.5x. For high-frequency traders or those running index arbitrage strategies, these aren’t rounding errors — they’re strategy-breakers.

What this means in practice:

- Many short-duration, low-margin F&O strategies that were marginally profitable after costs will tip into loss territory.

- Expect a reduction in F&O volumes, particularly in near-expiry contracts where traders rely on thin per-lot margins.

- Break-even points on spreads, straddles, and delta-neutral trades shift meaningfully upward.

For equity delivery and equity mutual fund transactions, STT is unchanged. This is explicitly a derivatives-focused cost hike — and the market’s reaction on Budget day suggested real concern about liquidity.

2. Mutual Funds 2.0: Lower Costs, Tougher Governance

But it’s not just traders feeling the pressure.

SEBI has done something remarkable on the mutual fund side: it has replaced the entire 1996 MF Regulation framework with the new SEBI (Mutual Funds) Regulations, 2026, effective April 1. The old rulebook served for 30 years. The new one is a comprehensive rewrite.

On costs — this time, in your favour:

The Total Expense Ratio (TER) structure has been revised with explicit limits on what AMCs can charge investors. Only a defined set of items — base expense ratio, permitted brokerage, transaction costs, statutory levies, and exit load — can sit inside TER. Everything else is out.

SEBI has also:

- Removed the earlier provision allowing an additional 5 bps where exit load was levied

- Cut TER ceilings for ETFs, Fund of Funds, and close-ended schemes

- Reduced brokerage caps that mutual funds can pay — both in cash markets and derivatives

The net effect: headline expense ratios should compress, especially for passive and thematic structures.

On governance — trustees now have real teeth:

Under the 2026 Regulations, trustees and independent directors must actively monitor investment management agreements, scheme-level remuneration, related-party contracts, and charges levied to investors — and formally flag and follow up on deficiencies.

This isn’t just a disclosure tweak. It shifts accountability upstream. AMCs will face harder questions from their own boards.

Who benefits: Direct plan investors, long-term SIP investors, ETF holders.

Who feels pressure: Distributors, AMCs running higher-cost active strategies.

3. Gold & Silver Funds: Your NAV Is Now Tied to Exchange Spot

Meanwhile, mutual fund investors in gold and silver are seeing a very different kind of shift — one about price integrity.

SEBI has mandated that from April 1, 2026, all mutual funds must value physical gold and silver using “polled spot prices” published by recognised stock exchanges — specifically, the same prices used to settle physically delivered bullion derivatives contracts.

Until now, funds had discretion in choosing third-party price providers, which meant two gold ETFs could — in theory — show slightly different NAVs for the same underlying metal.

That’s ending.

What changes for you:

- Gold ETF and gold FoF NAVs will be directly and consistently anchored to exchange spot polls.

- Tracking error relative to bullion prices should tighten.

- But intraday NAV sensitivity to exchange price swings may increase — if exchange gold prices move sharply in a session, fund NAVs will reflect that more immediately.

For most long-term gold investors, this is a clean, pro-transparency move. For traders trying to exploit NAV-price gaps in gold ETFs, the window narrows.

4. Leverage Is Getting Squeezed — Hard

At the same time, RBI is tightening the screws on how market participants can borrow against their portfolios and how brokers can fund client positions.

The new RBI directions on capital-market exposure and broker funding kick in from April 1, 2026. Here’s what’s being clamped:

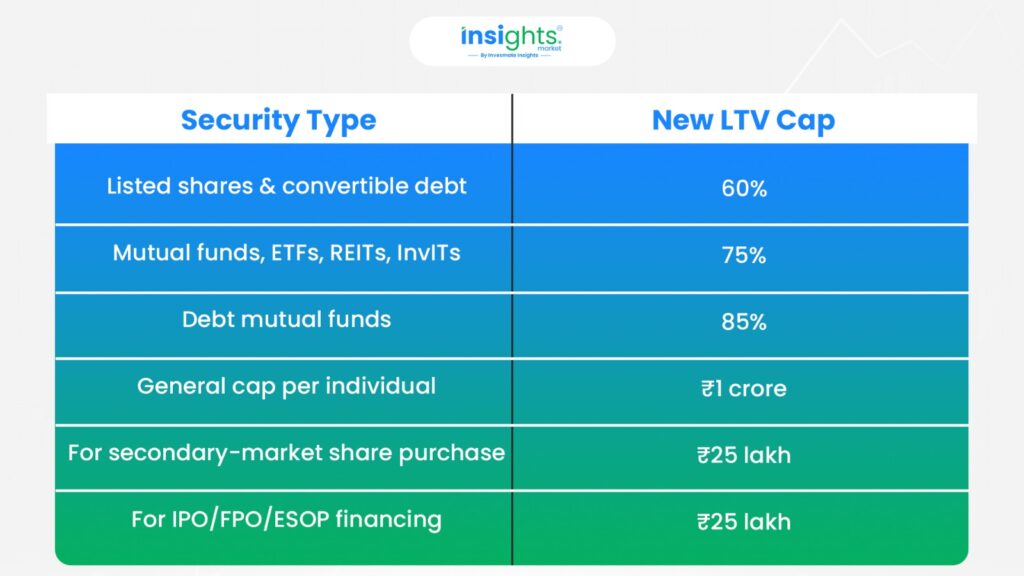

Loans against securities — new LTV caps:

Acquisition finance:

- Bank funding now capped at 75% of deal value — acquirers must bring at least 25% equity.

- Listed acquirers must show profit in each of the last three years; unlisted acquirers need at least a BBB- credit rating; minimum net worth requirement: ₹500 crore.

Broker funding:

- From April 1, only 100% secured funding will be permitted for brokers — unsecured promoter or corporate guarantees are out.

- At least half the collateral must be in cash; shares used as collateral face higher haircuts.

Who this hits:

- HNIs and promoters running leveraged share-backed borrowing strategies face tighter headroom.

- Brokers who have been offering aggressive margin funding to clients will need to recalibrate.

- Highly leveraged acquisition structures become harder to finance through banking channels.

For risk-controlled, fully-funded investors, this is largely irrelevant. For leveraged market participants, it’s a material constraint.

5. Tax Reset: New Act, New SGB Rules, Same STT Hike

Finally, there’s the taxation layer — and it touches almost everyone.

The New Income Tax Act 2025:

India’s direct tax law is being comprehensively rewritten. The new Income Tax Act 2025 comes into force from April 1, 2026 (FY 2026–27). This isn’t just a rate change — the statute itself is being recast.

Capital-market investors should revisit their tax planning not just for what rates apply, but because the sections, definitions and computation mechanics may have changed. If your CA or financial advisor hasn’t already flagged this, it’s worth asking them to run through what’s different for your specific situation.

Sovereign Gold Bonds (SGBs) — an important narrowing:

This one catches many investors off guard.

Until now, SGB redemptions at maturity were tax-exempt for everyone — including investors who bought SGBs on the stock exchange at a discount to face value, and held until RBI’s scheduled redemption.

From April 1, 2026, this exemption is restricted to original subscribers only.

If you buy SGBs on the secondary market after this date and hold to redemption, the gains will be taxable under the new law — not exempt. The strategy of buying discounted SGBs and collecting tax-free maturity proceeds is gone.

For existing secondary-market SGB holders approaching maturity, the effective date and their purchase date both matter for how redemption proceeds will be treated. Worth checking your specific tranches.

The Bigger Picture

April 1, 2026 isn’t just a policy shift — it’s a signal.

Indian markets are moving away from easy leverage, high-churn trading, and opaque fee structures… toward transparency, discipline, and long-term investing.

Whether you’re a trader, a SIP investor, or someone managing a portfolio, this is a good time to review your strategy, recalculate your costs, and make sure your tax planning is updated for the new year.

The rulebook just changed. Make sure you’ve read it.

FAQs

From April 1, 2026, several key changes take effect simultaneously — STT on equity futures rises by 150%, SEBI’s new Mutual Fund Regulations 2026 replace the 30-year-old framework, RBI introduces stricter LTV caps on loans against securities, gold and silver fund NAVs must now track exchange spot prices, and the new Income Tax Act 2025 comes into force. Together, these changes affect traders, mutual fund investors, borrowers, and taxpayers.

STT on equity futures has increased from 0.02% to 0.05% of transaction value — a 150% hike. For options, the STT on premium rises from 0.10% to 0.15%, and on exercised options from 0.125% to 0.15%. These changes are effective for all trades on or after April 1, 2026, under Clause 143 of Finance Bill 2026. STT on equity delivery trades remains unchanged.

Not for everyone. From April 1, 2026, the tax exemption on SGB maturity redemptions is restricted to original subscribers only. If you purchased SGBs on the secondary market, gains at maturity will now be taxable under the new Income Tax Act 2025 — the earlier blanket exemption no longer applies. Investors holding secondary-market SGBs approaching maturity should review their specific tranche purchase dates carefully.

RBI’s new directions cap Loan-to-Value (LTV) ratios as follows — listed shares and convertible debt at 60%, mutual funds, ETFs, REITs, and InvITs at 75%, and debt mutual funds at 85%. There is also an overall cap of ₹1 crore per individual, with sub-limits of ₹25 lakh for secondary market share purchases and ₹25 lakh for IPO/FPO/ESOP financing. These limits are effective from April 1, 2026.

SEBI’s new Mutual Fund Regulations 2026 tighten what AMCs can include in Total Expense Ratio (TER). Only defined items — base expense ratio, permitted brokerage, transaction costs, statutory levies, and exit load — are allowed inside TER. The earlier provision permitting an extra 5 bps where exit load was levied has been removed. TER ceilings for ETFs, Fund of Funds, and close-ended schemes have also been cut — meaning most investors, especially direct plan and SIP investors, should see lower costs over time.

SEBI’s new Mutual Fund Regulations 2026 tighten what AMCs can include in Total Expense Ratio (TER). Only defined items — base expense ratio, permitted brokerage, transaction costs, statutory levies, and exit load — are allowed inside TER. The earlier provision permitting an extra 5 bps where exit load was levied has been removed. TER ceilings for ETFs, Fund of Funds, and close-ended schemes have also been cut — meaning most investors, especially direct plan and SIP investors, should see lower costs over time.

This article is for educational and informational purposes only. It is not investment advice or a stock recommendation. Investors should conduct their own research or consult a qualified financial advisor before making investment decisions.