![]()

Picture this: Your favorite stock has been falling for months. Everyone’s selling. Your investment group chat is filled with panic. News headlines scream doom. And then, a few months later, the same stock doubles. Sound familiar?

This is exactly what’s playing out with foreign institutional investors (FIIs) in India right now. And if history is any guide, we might be sitting at one of the most contrarian buying opportunities in years.

The Counter-Intuitive Truth About FII Flows

Here’s something most investors get wrong: FIIs don’t create trends—they chase them.

Think of FIIs like guests at a party. They arrive after the music starts and leave before it ends. They’re momentum players, not visionaries. A detailed study from 2007-2017 proved this: FIIs consistently bought Indian stocks when PE ratios were high (expensive) and sold when PE ratios were low (cheap).

So when you see massive FII selling, your first instinct says “danger.” But the data says “opportunity.”

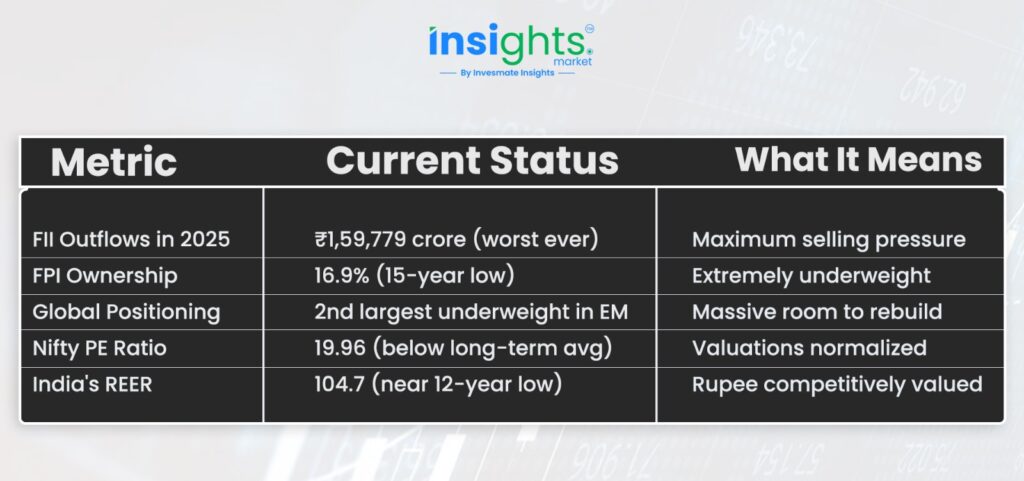

What's Actually Happening Right Now?

Let me break down the current situation in simple numbers:

Translation: Everyone who wanted to sell has already sold. Valuations are no longer expensive. The rupee is cheap on a real basis. This is the contrarian setup.

Why FIIs Have Been Selling So Much

Here’s the part most people are missing—and it’s critical to understand the current phase.

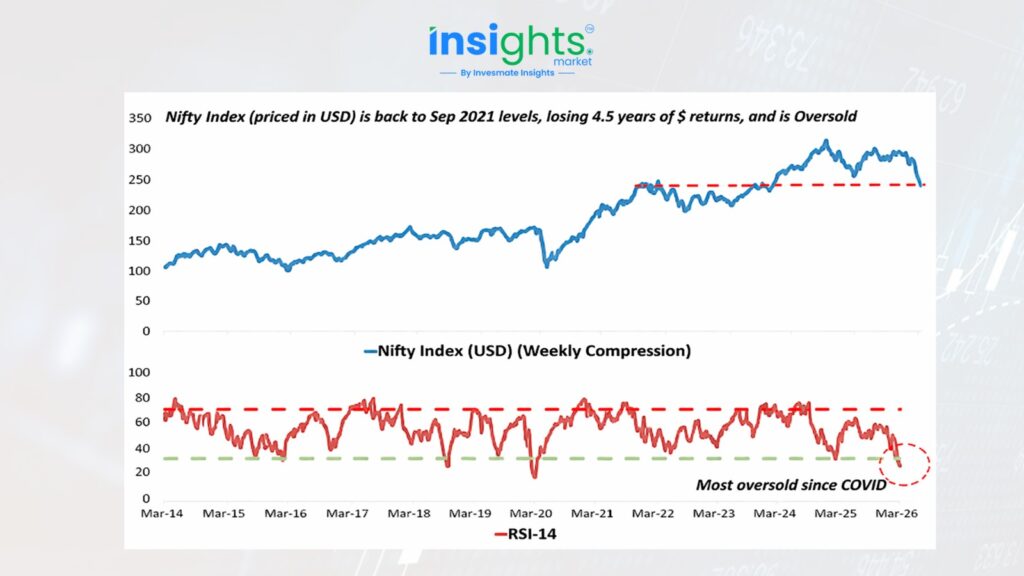

Technically, FIIs have made almost 0% returns from Indian markets over the last ~4.5 years (in dollar terms).

Even though Indian markets have delivered returns in rupee terms, foreign investors haven’t benefited the same way.

This is because rupee depreciation has offset the gains made in the market.

- Equity returns (INR): Positive

- Currency impact (INR → USD): Negative

- Net result for FIIs: Near-zero returns

In simple terms, FIIs invested, markets went up—but when converted back to dollars, those gains largely disappeared.

This creates a weak incentive to stay invested:

- Returns don’t justify risk

- Capital gets reallocated globally

- Selling pressure increases

So FIIs are not just reacting to valuations—they are reacting to actual realized returns in dollar terms.

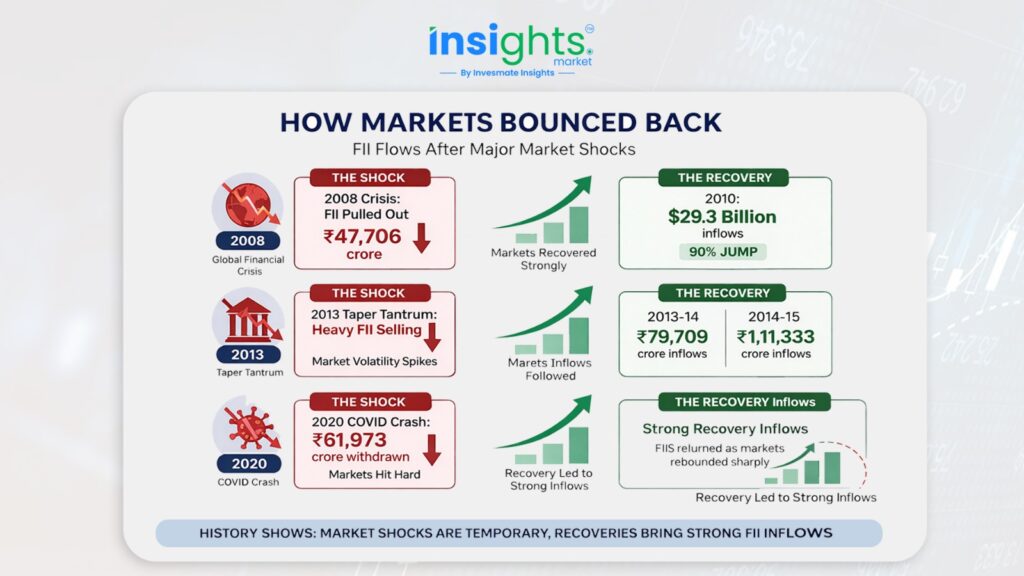

The Historical Pattern That Never Fails

Here’s where it gets interesting. Every major FII exodus in India’s history has been followed by massive inflows:

The Comeback Pattern:

Recovery Timeline: Typically 6-18 months from peak outflows to stabilization.

Why This Time Has Better Support

Here’s the game-changer: For the first time in history, domestic institutional investors (DIIs) now own more of the Indian markets (17.62%) than FIIs (17.22%).

Your neighborhood uncle investing via SIPs and domestic mutual funds has created a safety net that didn’t exist in 2008 or 2013. This means:

- Less volatility when FIIs sell

- Stronger floor under the market

- Better risk-reward for new positions

The Four Signals FIIs Watch

Three out of four boxes are already checked. That’s not a guarantee, but it’s a strong setup.

What Smart Money Is Saying

HSBC Mutual Fund’s recent outlook is telling: “We expect a return of FII investors into India in 2026, catalyzed by better earnings growth visibility in FY27 and potential US trade deal.”

They’re not saying “buy tomorrow.” They’re saying the probability of sustained foreign returns is improving from a low base.

The Capital Account Story (Why Economists Care)

Here’s the deeper angle: India’s capital account has slipped into deficit. Net FDI has fallen from $40 billion to nearly zero due to repatriation and IPO exits. This isn’t just about stock prices—it’s about balance of payments stability.

When FII/FDI flows improve, it helps:

- Stabilize the rupee

- Fund the current account deficit

- Reduce pressure on forex reserves

This makes it an economic story, not just a market-timing story.

The Investment Takeaway

This is NOT a timing call. FII flows can stay weak longer than valuations suggest, especially if the dollar strengthens or global risk appetite deteriorates.

But here’s the smart framing: “FIIs don’t buy India because it’s loved. They buy when India is less crowded, less expensive, and the rupee has absorbed the bad news.”

Right now, we’re at that point. India has gone from everyone’s favorite (overweight, expensive) to everyone’s problem child (underweight, fairly valued).

The contrarian question isn’t “Will FIIs come back?”—it’s “How much are you willing to allocate while others are still pessimistic?”

Bottom Line

Record FII outflows, 15-year low ownership, normalized valuations, and weak REER create the classic contrarian setup. History shows foreign flows return precisely when everyone thinks they won’t. The probability of a sustained comeback is improving—even if the timing remains uncertain.

Are you positioning for the turn, or waiting for everyone else to confirm it’s safe?

Key Metrics to Watch:

- Nifty PE ratio trend

- Monthly FII flow data (NSDL reports)

- REER movement

- Q4 FY26 earnings trajectory

FAQs

Foreign Institutional Investors (FIIs) are global investors who invest in Indian equities and debt markets. Their large capital flows influence liquidity, market sentiment, and short-term price movements, making them a key driver of stock market trends.

FIIs have been selling due to a combination of factors including lower dollar-adjusted returns, rupee depreciation, better opportunities in global markets, and portfolio rebalancing. Even when Indian markets rise in rupee terms, currency depreciation can reduce their actual returns in USD.

Not necessarily. Historically, large FII outflows have often occurred near market bottoms rather than tops. These phases can create contrarian buying opportunities as valuations become attractive and selling pressure gets exhausted.

FIIs invest in Indian markets in rupees but measure returns in dollars. If the rupee depreciates, it reduces or even wipes out equity gains when converted back to USD, leading to lower real returns and potential capital outflows.

FIIs usually return when key conditions improve—reasonable valuations, stable currency, strong earnings visibility, and macroeconomic stability. Historically, this turnaround happens 6–18 months after peak outflows.

It can be a favorable time from a contrarian perspective, as markets are often less crowded and valuations are more reasonable. However, investors should focus on fundamentals and avoid timing the market purely based on FII flows.

This article is for educational and informational purposes only. It is not investment advice or a stock recommendation. Investors should conduct their own research or consult a qualified financial advisor before making investment decisions.