![]()

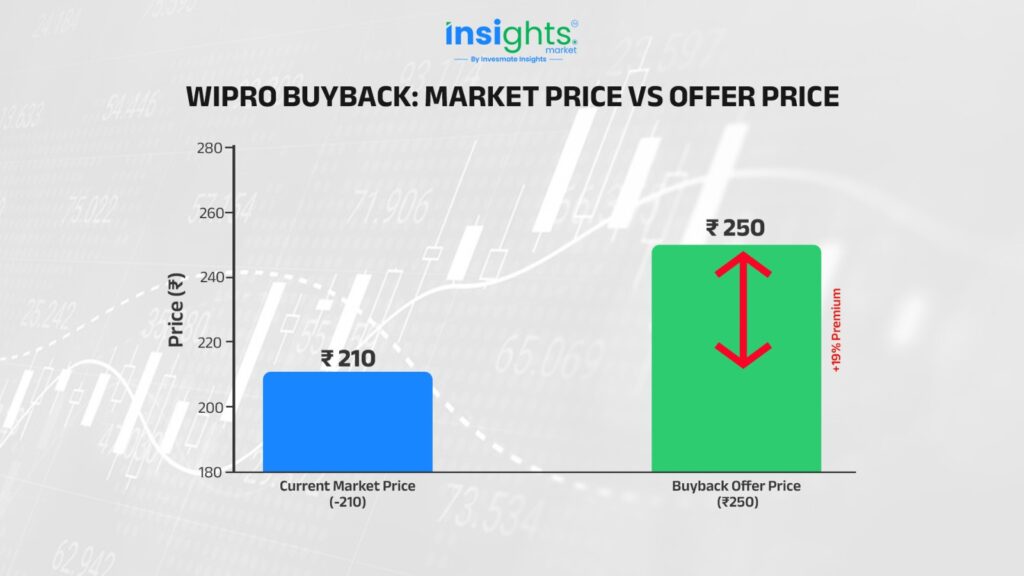

Picture this. You’re checking your portfolio on a Thursday evening after market hours, and suddenly a notification pops up. Wipro — one of India’s biggest IT giants — just announced it will buy back your shares at Rs 250 each. The market closed at Rs 210. That’s a 19% premium — handed to you on a silver platter. Sounds like free money, right?

Well, not quite. Before you rush to tender your shares, let’s pull back the curtain on exactly what Wipro is doing, why they’re doing it, and how much you’ll actually pocket after taxes, acceptance ratios, and market dynamics. Because the real number is very different from the headline.

At a Glance: Key Numbers

The Premium Visualised

Why Is Wipro Doing This? (The Honest Answer)

Let’s cut through the corporate speak. A buyback sounds like a company celebrating great times ahead — but Wipro’s case is more nuanced, and actually more interesting because of it.

Rs | Wipro is sitting on Rs 41,510 crore in cash as of December 2025 — the highest cash pile among all major Indian IT companies. When a company can’t find high-return opportunities to deploy that cash, returning it to shareholders is simply smart financial management. |

The 4 Real Reasons Behind This Buyback

- Idle cash problem: Rs 41,510 crore in cash earns far less sitting in the bank than it creates as shareholder value when returned via buyback.

- Weak near-term outlook: Q1 FY27 revenue guidance is -2% to 0% sequential growth in constant currency — that is flat to declining. Not the profile of a company deploying cash aggressively into growth.

- Soft demand environment: Core IT demand remains muted, and growth has been largely inorganic. The business isn’t booming.

- EPS accretion: Buying back ~5.7% of equity shrinks the share count, mechanically boosting earnings per share by mid-single digits. Motilal Oswal estimates 1-2% EPS upgrade from this move.

! | Morgan Stanley, which carries an ‘Underweight’ rating on Wipro, noted that near-term sentiment may get a bump from the buyback — but attention will quickly refocus on the muted FY27 revenue growth outlook. |

The bottom line: This is not a growth signal. It is capital discipline. Wipro is saying: ‘We don’t see enough high-return internal opportunities for this cash, so we’re giving it back.’ That’s actually responsible corporate governance — but don’t mistake it for a business upcycle.

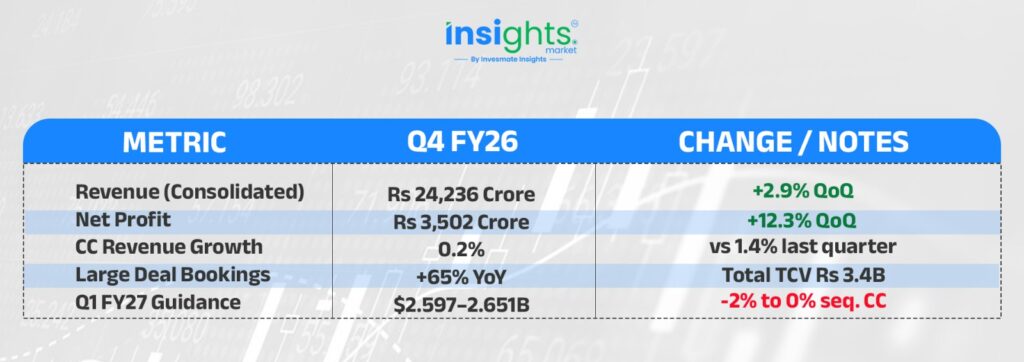

Wipro's Q4 FY26 Results: The Numbers That Matter

Numbers were largely in line with analyst estimates — no major shocks. However, the BFSI (Banking, Financial Services & Insurance) segment showed weakness, down ~1.3% due to specific client issues.

What Does This Mean For You as a Retail Investor?

Here is where things get really interesting — and a bit tricky.

Step 1: The Headline Math (Too Good to Be True?)

In a perfect world where 100% of your shares are accepted:

Step 2: The Acceptance Rate Reality Check

Here is the hard truth: you won’t get 100% of your shares accepted. In Wipro’s 2023 buyback, the retail entitlement ratio was 23.4%. Analysts expect this time to be in a similar range — roughly 15-25%.

And this time, promoters (who hold a massive 73% stake) have already signaled participation. That means more shares competing for the same pool, which typically lowers the retail acceptance ratio.

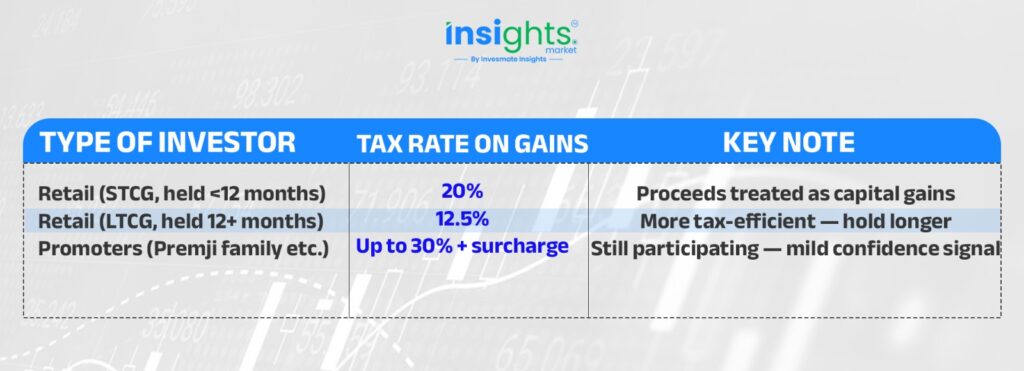

The New Tax Rules (April 2026 — This Changes Everything)

TAX | Important: India’s Finance Act 2026 changed how buyback proceeds are taxed — starting April 1, 2026. This is the first buyback under the new rules, so many investors are unaware of the implications. |

Previously, buybacks were taxed at a flat company-level DDT of 23.3%. Now the tax burden shifts entirely to the investor. If you’ve held Wipro for over a year, you’re in better shape with 12.5% LTCG. Short-term holders will pay 20%.

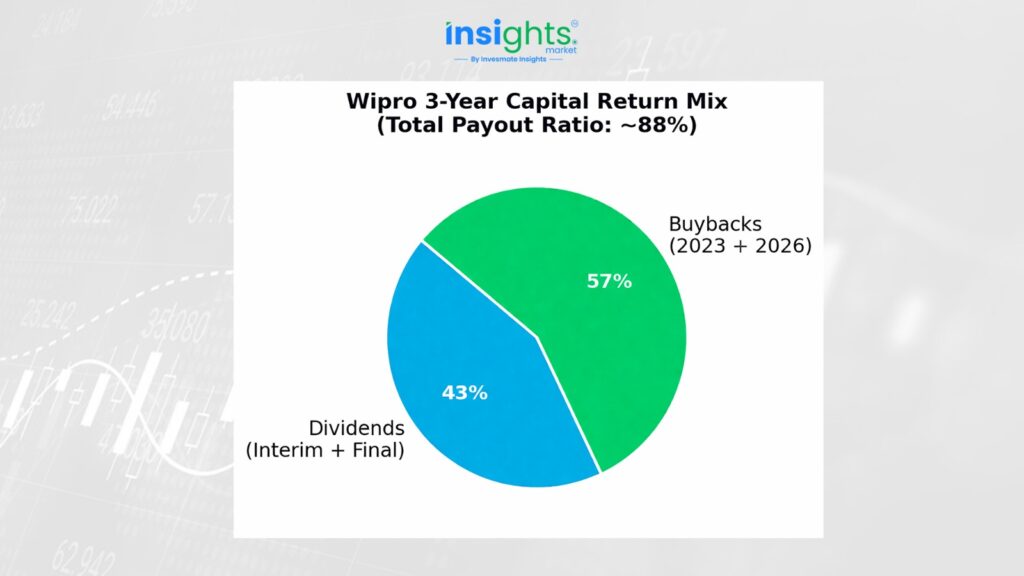

Wipro's 3-Year Capital Return Story: 88% Payout Ratio

Including the Rs 11/share interim dividend already paid, Wipro’s total shareholder returns over the last 3 years stand at ~88% — putting it on par with larger peers like TCS and Infosys. Nomura raised EPS estimates by 1-2% following the buyback announcement.

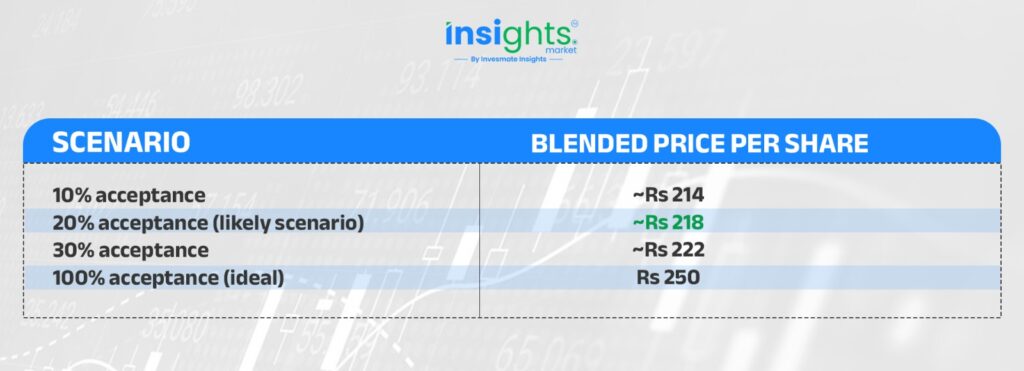

The Blended Price Effect: Your Real Exit Price

Here is a subtle but important calculation most investors miss. Since only ~20% of your shares get accepted at Rs 250, and the rest stay in your demat account at ~Rs 210, your effective average selling price is not Rs 250.

Effectively, at 20% acceptance, your blended exit is Rs 215-220 per share — a modest ~3-5% improvement over the market price, not 19%.

Should You Participate? A Framework

Key Dates to Watch

- Board approval: April 16, 2026 (Done)

- Shareholder approval: Required (timeline to be announced)

- Record date: Not yet declared — watch for public announcement and letter of offer

- Expected completion: Q1 FY27 (by June 2026)

CAL | Mark your calendar: The record date determines who is eligible to participate. You must hold Wipro shares before the record date to tender them in the buyback. |

The Verdict: Free Money? Not Quite — But Still Worth Noting

Wipro’s Rs 15,000 crore buyback is India’s largest IT buyback ever, and the first under the new April 2026 tax framework. It’s a well-structured shareholder return move — but let’s be clear about what it is and isn’t:

- It IS a smart capital return by a cash-rich company with limited near-term growth visibility.

- It IS NOT a signal that Wipro’s business is about to accelerate.

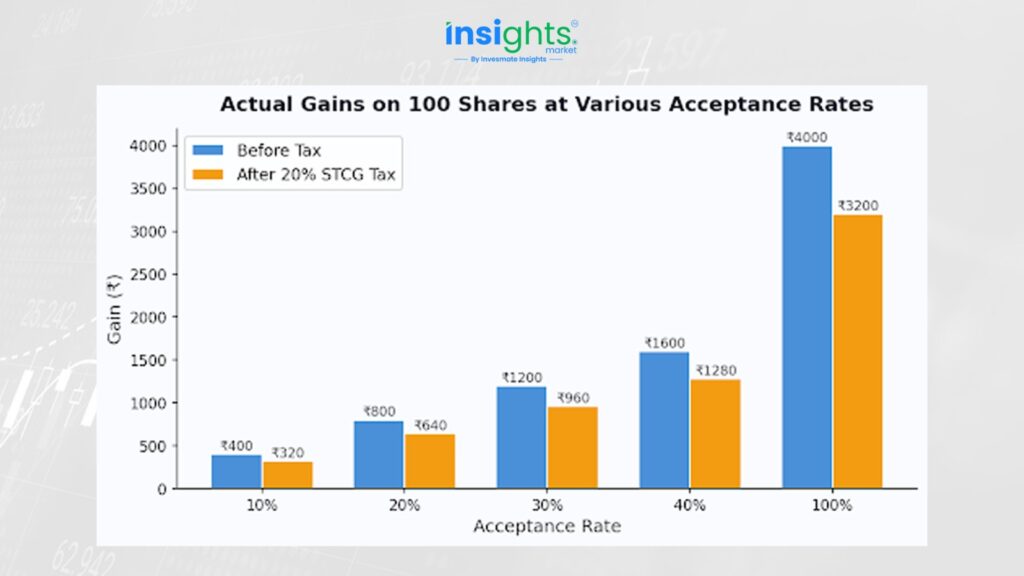

- Your real after-tax gain at a 20% acceptance rate on 100 shares is roughly Rs 640 — not Rs 4,000.

- The 3-year payout ratio of 88% shows Wipro is committed to shareholder returns, on par with peers.

If you hold Wipro and want a partial clean exit at a premium, the buyback offers a disciplined, low-risk opportunity. But if you’re betting on a business revival, the Q1 FY27 guidance of -2% to 0% growth tells a sobering story. Trade with eyes wide open.

FAQs

Wipro has announced a buyback at Rs 250 per share, which is about a 19% premium over the current market price of around Rs 210. However, this full premium applies only if 100% of your shares are accepted, which is unlikely in reality.

The expected acceptance ratio is around 15% to 25%, based on historical trends like Wipro’s 2023 buyback (23.4%). Promoter participation this time may further reduce the effective acceptance for retail investors.

At a 20% acceptance rate, a retail investor holding 100 shares may earn about Rs 800 before tax and roughly Rs 640 after 20% STCG tax. So, the real gain is much lower than the headline Rs 4,000.

Under the new tax rules effective April 2026, buyback gains are taxed in the hands of investors. Short-term capital gains (holding <12 months) are taxed at 20%, while long-term capital gains (holding >12 months) are taxed at 12.5%.

Since only a portion of your shares (e.g., ~20%) gets accepted at Rs 250 and the rest remain at market price (~Rs 210), your effective selling price becomes a blended average of around Rs 215–220, not Rs 250.

You may consider participating if you want partial liquidity or a short-term premium exit. However, long-term investors bullish on IT sector recovery may prefer to hold, especially given Wipro’s muted near-term growth guidance.

This article is for educational and informational purposes only. It is not investment advice or a stock recommendation. Investors should conduct their own research or consult a qualified financial advisor before making investment decisions.