![]()

The Real Story Behind Q4 FY26

Okay, real talk — most stocks “beat estimates” because the bar was set so low that literally anyone could’ve cleared it. Every quarter, there’s a chorus of “company X beat expectations!” And every quarter, if you look closely, the “expectations” were slashed just enough before results to make the numbers look good.

But Q4 FY26? This one actually had some genuine overachievers. Companies that grew fast not because their base was weak, but because their businesses genuinely got better. Solar parks are getting built. Banks are cleaning up bad loans. AI servers flying off the shelves. Credit ratings are picking up. A PSU bank is quietly stealing market share.

Five companies. Five completely different sectors. All of them had a legit story — backed by actual numbers.

DISCLAIMER

This is a research and educational blog. Not investment advice. Markets carry risk — you know the drill.

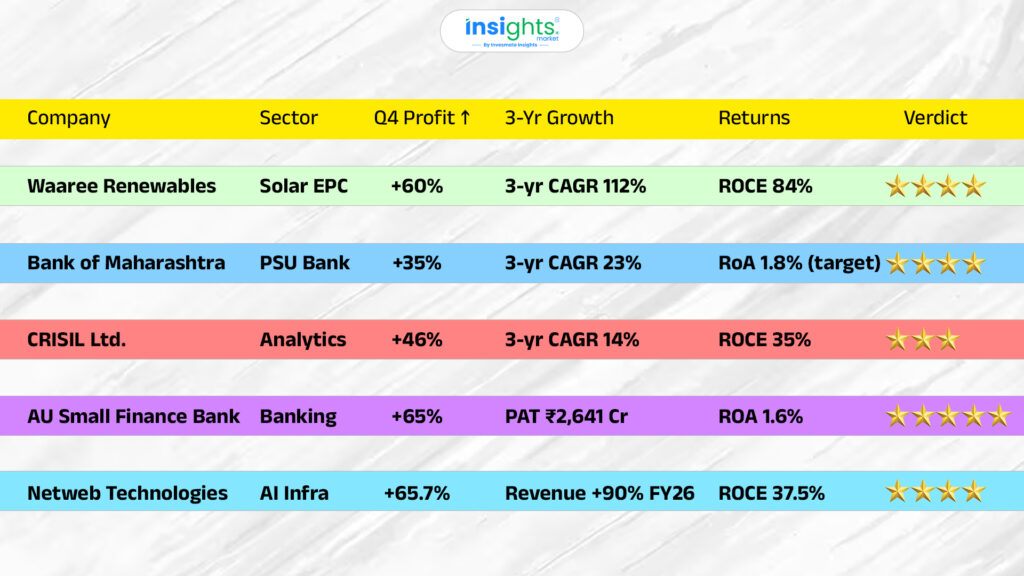

The Quick Scoreboard

Before we go deep on each one, here’s the bird’s eye view. Think of this as your cheat sheet.

Waaree Renewable Technologies

India’s solar builders — not panel makers, the people actually constructing the parks

What does this company actually do?

Imagine India wants to build a massive solar farm in Rajasthan. Someone has to actually design it, buy all the equipment, and build the damn thing. That’s Waaree Renewables. They’re called an EPC company — Engineering, Procurement & Construction. They don’t make the solar panels (their parent Waaree Energies does that). They just build the parks.

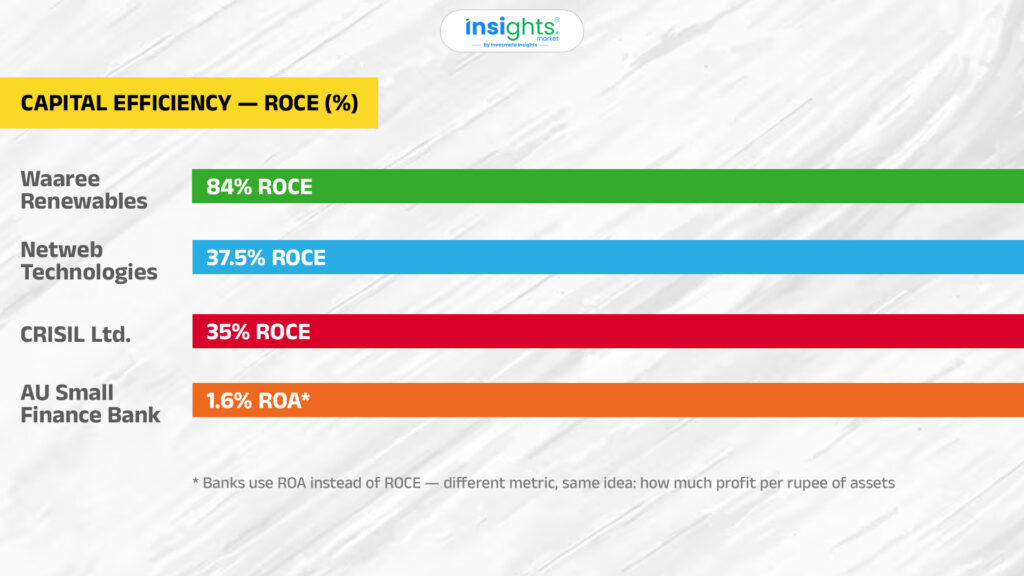

The clever bit? They don’t own any heavy machinery or factories. They design, coordinate, and manage. Very capital-light — which means high returns on whatever money they put in.

131% Sales Growth | 60%+ Profit Growth | 84% ROCE | 2.8 GW Order Book | 36 GW Bidding Pipeline |

The number that blew me away

Their pipeline of projects they’re currently bidding on is 36 GW. You know what they actually executed in all of FY26? About 2.8 GW. So they’re bidding for 13 times their current annual capacity. Even if they win 30% of that, they’re looking at years of work already lined up.

THINGS TO WATCH

When Waaree takes on big ‘turnkey’ contracts (where they handle everything end-to-end), their profit margins get squeezed because costs pile up. Their margin dipped to 18.8% — not terrible, but compressed. Also watch receivables — money their clients owe them is growing faster than sales, which means working capital could get tight.

VERDICT

India needs to build 350 GW more solar by 2030. Waaree is literally in the business of building it. Their order pipeline is enormous, they’re asset-light (smart model), and even at 28x P/E they’re cheaper than peers. The margin pressure is real but manageable. High conviction — if you’re patient.

Bank of Maharashtra

The PSU bank quietly outgrowing the entire industry — nobody’s talking about it

Why this one surprised everyone

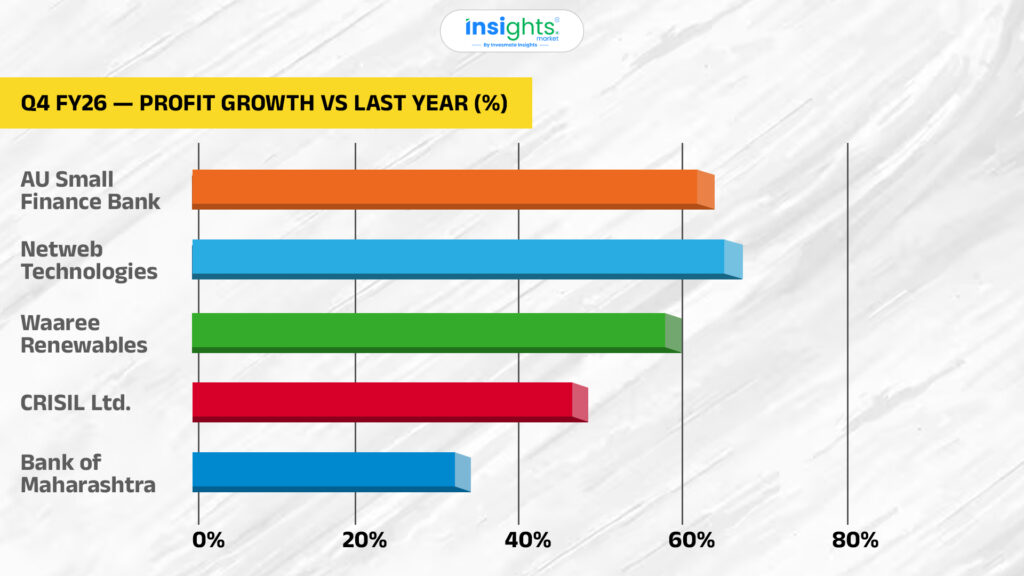

Public sector banks (PSU banks) have a reputation. Slow. Government-ish. Lots of bad loans. Not exactly exciting. So when the whole banking industry grew credit at 16% and Bank of Maharashtra grew at 22% — people sat up. That 6 percentage point gap matters a lot. It means BOM is taking customers and loan books away from competitors. Net profit jumped 35%.

22% Credit Growth(vs 16% industry) | 35% Net Profit Growth | 3.75% NIM Target FY27 | ₹2,000Cr Extra Income Est. FY27 |

What's their secret weapon?

CASA ratio — this is the share of deposits that are in Current Accounts and Savings Accounts. These are cheap deposits (you don’t earn much interest on a savings account, right?). So the more CASA a bank has, the cheaper its funding is, and the more it can make on lending. BOM has been improving this — and it structurally protects their profit margins going forward.

THINGS TO WATCH

Their interest margin (NIM) slipped a bit — from 3.9% to a guided 3.75%. Also, about 41% of their loans are linked to the RBI repo rate, which means when RBI cuts rates (which it’s been doing), loan yields fall faster than deposit costs. That’s a short-term headwind on margins.

VERDICT

Strong execution, improving loan quality, and genuinely outgrowing the competition. The main thing to track in FY27 is whether provisions (money set aside for bad loans) stay low — because that’s what’s been powering the profit jump. If that holds, this story continues.

CRISIL Ltd.

The credit rating gatekeeper. 51% market share. Best quarter in 3 years.

So what does CRISIL actually do?

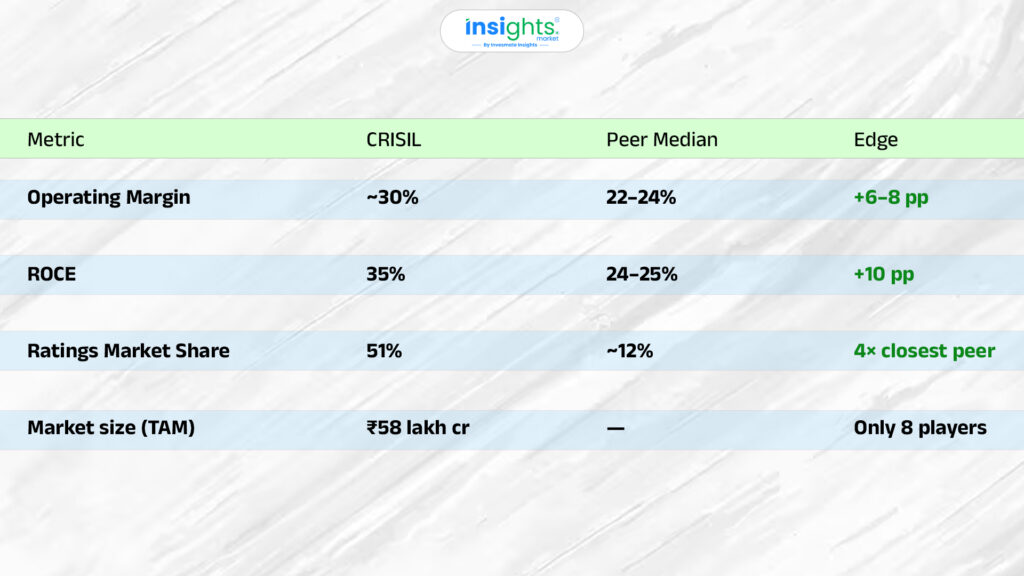

When a company wants to borrow money by issuing bonds or commercial paper, they need someone to tell investors: how risky is this? That someone is CRISIL. They’re like the report card writer for corporate India’s debt. 51% market share in credit ratings — with only 8 players in the whole market. They’re the dominant force.

But here’s the interesting part — ratings is only one piece. Their bigger revenue driver is their Global Analytical Centre (GAC), which does research and analytics work for S&P Global (their parent company). S&P delegates analytical work to CRISIL’s India team, and CRISIL charges for it. Cost-efficient for S&P, revenue for CRISIL. Win-win.

30% Sales Growth YoY | 46% Profit Growth | ~30% Operating Margin | 51% Ratings Market Share |

CRISIL vs Peers — Why the moat is real

THINGS TO WATCH

The stock’s PEG ratio is around 39x — meaning most of the good news is already baked in. Also, new bond issuances in the corporate debt market are slowing a bit — and that directly hurts CRISIL’s ratings revenue since they only earn when companies issue new debt.

VERDICT

This is a classic quality compounder — great business, dominant position, consistent execution. The only catch is valuation. Don’t chase it after a 46% profit quarter. Wait for a dip, then act. This is a buy-on-weakness story, not a buy-on-momentum one.

AU Small Finance Bank

9 years old. Highest profit quarter ever. And they just applied for a full bank licence.

Wait — what's a Small Finance Bank?

A Small Finance Bank (SFB) is like a “restricted” bank. They got a licence from the RBI but with certain limits — they can only lend to small borrowers, can’t do everything a full bank does, and have tighter product restrictions. Think of it like a learner’s licence for banking.

AU got their SFB licence in 2017. Nine years later, they’ve grown into a ₹1.4 lakh crore deposit bank. And now? They’ve applied for a full universal bank licence. If RBI approves it, AU moves from learner’s licence to full driving licence. That’s a massive deal.

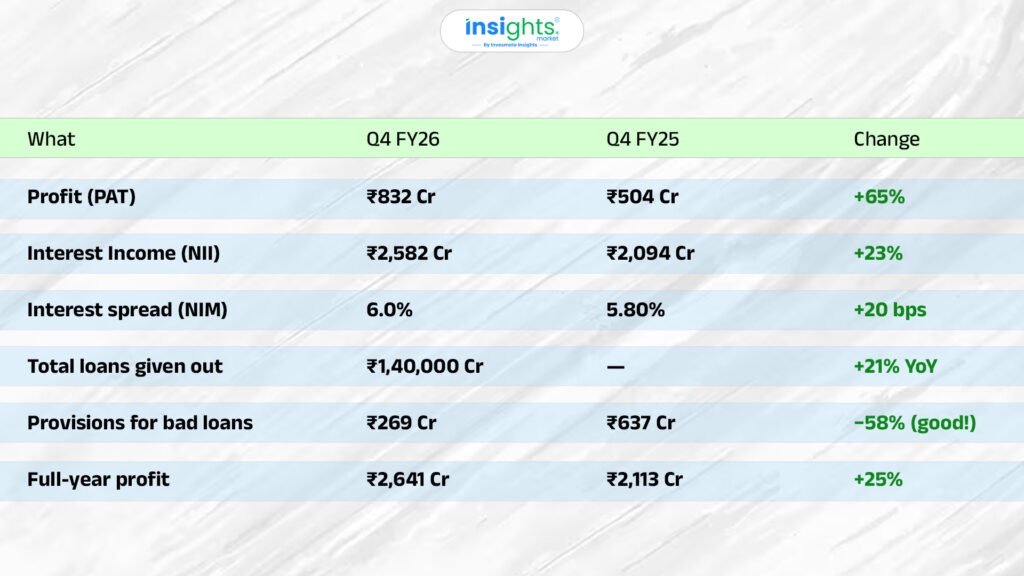

In Q4 FY26, their profit came in at ₹832 crore — up 65% from last year. And their NIM (the spread between what they earn on loans vs what they pay on deposits) hit 6% — a record high.

₹832Cr Q4 Profit (+65%) | 6.0% NIM (Record High) | +21% Loan Book Growth | −58% Provisions (fell sharply) |

The numbers, plain and simple

Why the universal bank licence is a big deal

Right now, AU can’t offer current accounts to corporates, can’t do merchant banking, and faces various product restrictions. Once they get a universal bank licence, all of that opens up. More products → more revenue streams → better margins → re-rating of the stock. It’s a genuine inflection point — if it comes through.

Timeline? Probably 18–24 months. And there’s no guarantee RBI approves it. But the application is filed, and management has cleared the procedural hurdles.

THINGS TO WATCH

Universal bank licence is still pending — no certainty on timing or outcome. GNPA (bad loans) at 2.03% is improving but still higher than top private bank peers. Their credit-deposit ratio at ~90% is elevated — meaning they’re lending out almost everything they receive as deposits, which leaves less buffer.

VERDICT

Growing loans 21%, margins at 6%, bad loans falling, AND a potential universal bank upgrade on the horizon? This is a rare combination. Analyst targets are in the ₹600–720 range. The universal bank licence — if approved — is a stock re-rating event. Patient money could do very well here.

Netweb Technologies

India’s only company building full AI supercomputing systems domestically. That moat is real.

Okay, what do they actually build?

You’ve heard of Nvidia making AI chips. You’ve heard of Dell or HP making servers. But who builds the complete AI computing system — the full stack — in India, for India? That’s Netweb. They design and manufacture high-performance computing (HPC) systems and AI servers domestically.

Here’s why this matters: every government in the world is now trying to build “sovereign AI” — AI that runs on servers in your own country. India’s government has earmarked ₹10,000+ crore for this under the IndiaAI Mission. And Netweb is the only listed Indian company that can supply these systems. That’s not a competitive advantage. That’s a structural moat.

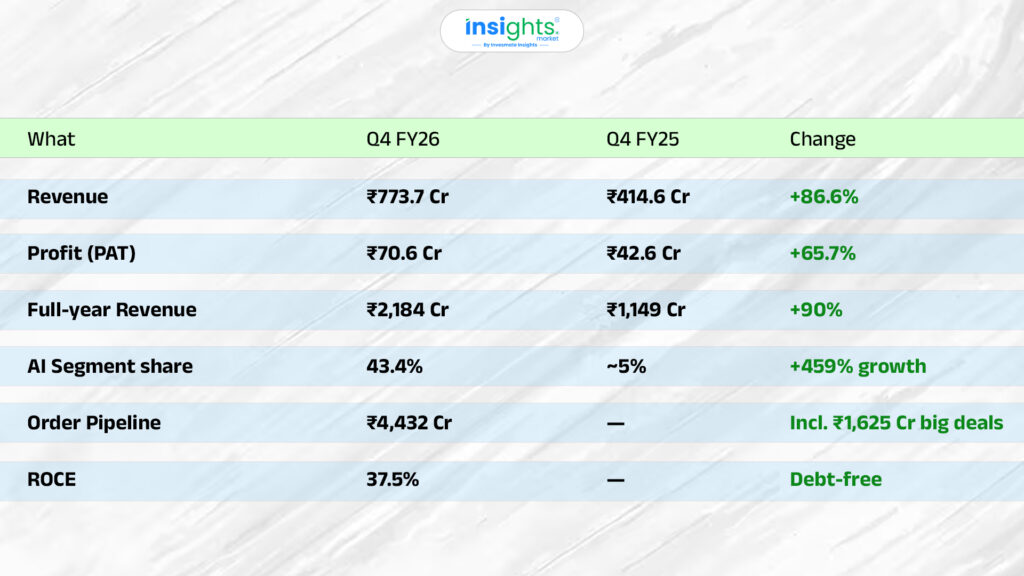

+87% Q4 Revenue Growth | +66% Q4 Profit Growth | 459% AI Segment Growth FY26 | Zero Debt (Debt-Free!) |

The numbers at a glance

Revenue mix shift — AI is eating the business (in a good way)

In FY25, AI was roughly 5% of revenue — a rounding error. By FY26, AI grew 459% and now represents 43% of total revenue. That’s a business transformation in 12 months. Full-year revenue nearly doubled — from ₹1,149 Cr to ₹2,184 Cr.

THINGS TO WATCH

Margins dipped a bit (to 12.5%) because large government orders tend to have lower margins — the government negotiates hard. Also, this is a small-cap stock with lower liquidity, so big institutional money can’t easily enter or exit. And their large deals tend to be concentrated with a few clients — concentration risk is real.

VERDICT

India’s AI infrastructure buildout is just getting started. Netweb is the only domestic company with the capability to supply it. Debt-free, 37.5% ROCE, and AI going from 5% to 43% of revenue in 12 months? That’s a business transformation. Analyst targets: ₹2,550–2,600. Accumulate — but size your position carefully given the small-cap risk.

Q4 FY26 wasn't just noise — it was a signal.

Solar infrastructure getting built. A PSU bank quietly grabbing market share. India’s most dominant ratings company firing on all cylinders. A small finance bank evolving into something bigger. And India’s AI compute story finally having a stock to represent it.

Whether you track all five or just deep-dive one — the key is to read the annual reports, watch the Q1 FY27 commentary, and always size your position to your conviction, not your FOMO.

Research smart. Invest with conviction.

FAQs

While many companies met lowered expectations, standout performers with genuine fundamental growth in Q4 FY26 included Waaree Renewables (Solar EPC), Bank of Maharashtra (PSU Bank), CRISIL Ltd. (Analytics & Ratings), AU Small Finance Bank, and Netweb Technologies (AI Infrastructure).

Netweb Technologies is currently the only listed Indian company that designs and manufactures full-stack artificial intelligence (AI) supercomputing systems and servers domestically. Their AI segment has seen massive growth, driven by India’s push for “sovereign AI” infrastructure.

A solar panel manufacturer produces the physical panels, while a Solar EPC (Engineering, Procurement, and Construction) company, like Waaree Renewables, is responsible for designing, managing, and building the actual solar parks. EPCs are typically asset-light businesses, which can lead to higher Capital Efficiency (ROCE).

When a Small Finance Bank (SFB) like AU Small Finance Bank upgrades to a universal bank license, the RBI removes previous product restrictions. This allows the bank to offer current accounts to large corporations, engage in merchant banking, and diversify its revenue streams, which often leads to a positive re-rating of the stock.

Bank of Maharashtra is outpacing industry credit growth by aggressively improving its CASA (Current Account Savings Account) ratio. A high CASA ratio provides the bank with access to cheaper deposits, which structurally protects its profit margins and allows it to offer more competitive lending rates to capture market share.

While companies with high Return on Capital Employed (ROCE) and strong market monopolies (like CRISIL) are excellent compounders, their valuations are often high following strong earnings reports. For quality stocks with high PEG ratios, investors often look to accumulate on market dips rather than chasing momentum immediately after an earnings beat.

This article is for educational and informational purposes only. It is not investment advice or a stock recommendation. Investors should conduct their own research or consult a qualified financial advisor before making investment decisions.