![]()

When we talk about India’s growth — new highways, metro rail, factories, railways, ports — one thing quietly connects all of it.

Steel.

And steel cannot be made without coking coal.

This is where Bharat Coking Coal Limited (BCCL) comes into the picture.

BCCL is not a new company. It has been operating since 1972. But for the first time, it is opening a part of its ownership to the public through an IPO.

What Exactly Is the BCCL IPO?

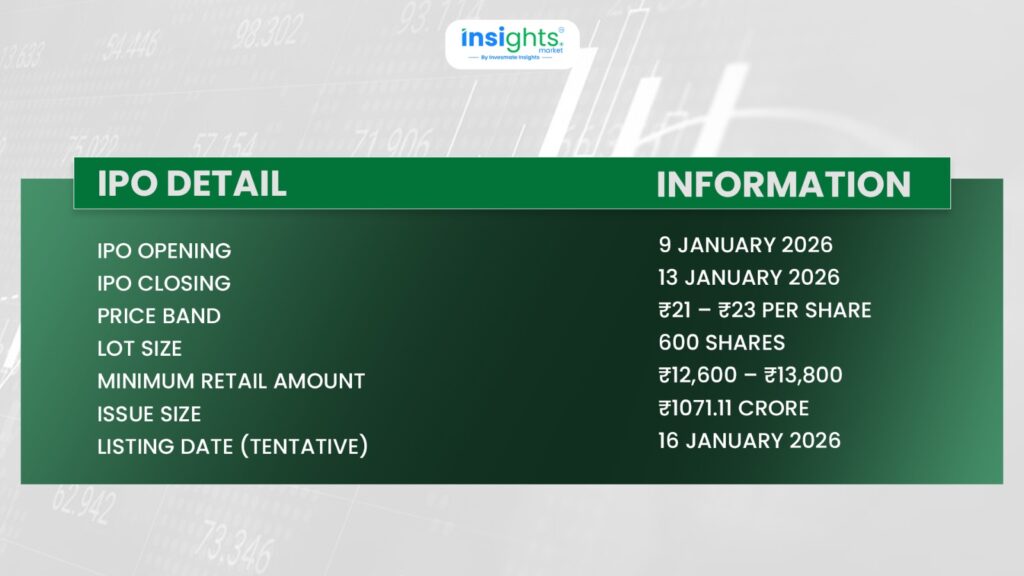

BCCL is coming out with a mainboard IPO in January 2026.

Here are the basic details:

Now comes an extremely important point.

This is a 100% Offer for Sale (OFS)

What does that mean?

- BCCL will not receive any money from this IPO

- The entire amount will go to the parent company, Coal India Limited

- Coal India is selling 10% of its stake in BCCL

So this IPO is not about funding new projects.

It is purely about changing shareholding.

What Does BCCL Do?

Coal is of many types, but for understanding BCCL, you only need to remember two:Thermal coal ,Coking coal.

How BCCL Makes Money

In FY25:

- BCCL alone produced 58.5% of India’s domestic coking coal

- Despite this, India still imports almost 90% of its coking coal needs

This makes BCCL strategically important, even if the coal sector itself faces long-term questions.

Why Is BCCL So Important?

India still imports almost 90% of its coking coal needs.

At the same time, steel demand continues to rise due to infrastructure and manufacturing growth.

BCCL matters because:

- It is the only company in India with prime coking coal reserves

- It holds 7.91 billion tonnes of coking coal resources

Its mines are located in Jharia (Jharkhand) and Raniganj (West Bengal) — regions known for high-quality coal.

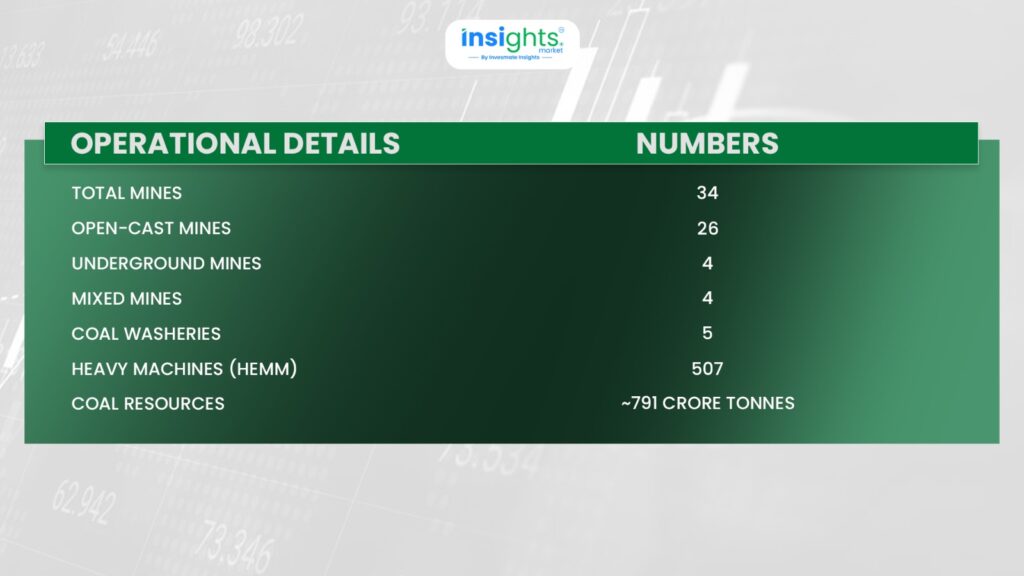

Scale of Operations: How Big Is BCCL?

As of September 2025:

BCCL also leads India in coal washing capacity at 13.65 million tonnes per year, which is essential because Indian coal has high ash content and must be cleaned before use.

Industry Background: Why Coking Coal Matters

India continues to invest heavily in infrastructure, manufacturing, and urban development. All of this keeps steel demand alive, and as long as steel demand exists, coking coal demand will also persist.

At the same time, renewable energy is expanding, and India has committed to achieving net-zero emissions by 2070. This creates a situation where coal remains important in the medium term, but faces uncertainty in the long term. BCCL operates right in the middle of this transition.

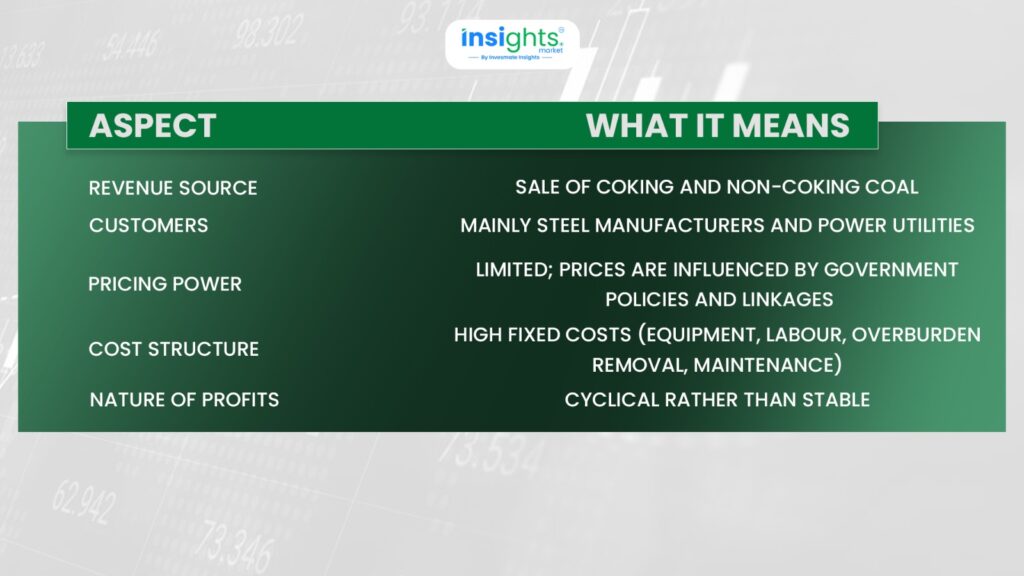

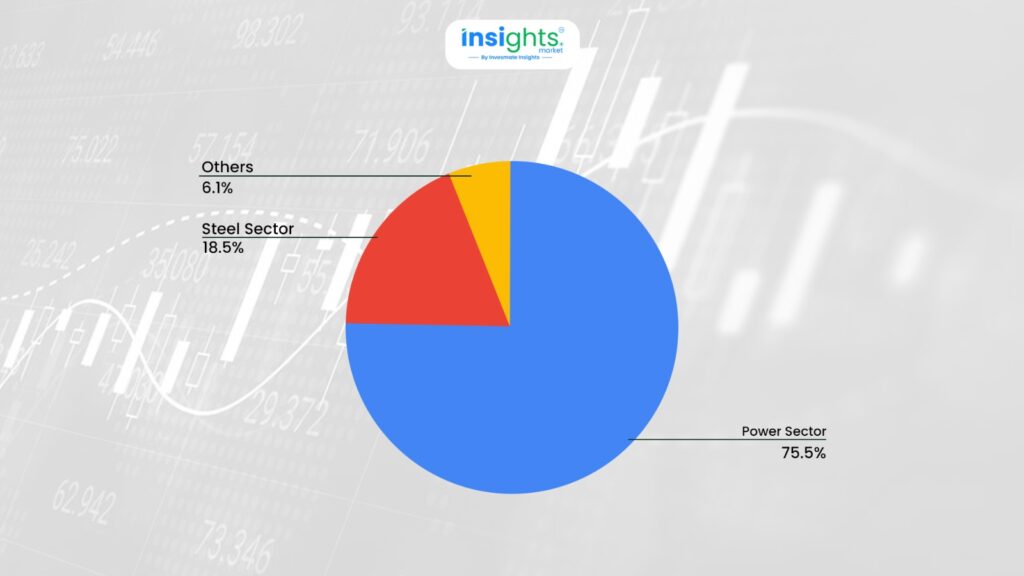

Who Buys Coal from BCCL?

BCCL’s customers are heavily concentrated.

Most of these customers are government-owned utilities and PSUs.

This concentration has an important implication. Government customers usually buy in large volumes, but payments are often delayed. This directly affects BCCL’s cash flow, which becomes very important when we look at the financials.

Financial Performance: What’s Happening Behind the Numbers?

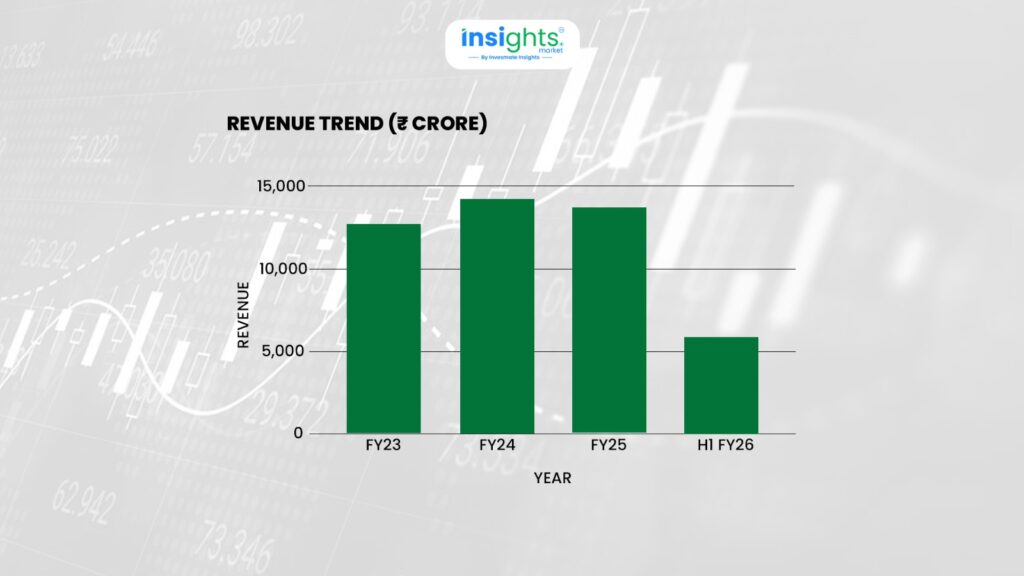

Why did revenue fall in FY25?

BCCL’s revenue grew from ₹12,624 crore in FY23 to ₹14,245 crore in FY24, reflecting strong production and dispatch. However, in FY25, revenue declined slightly to ₹13,802 crore.

This fall was not due to weak demand. FY25 witnessed excessive rainfall, which disrupted mining operations and reduced coal production and supply. When volumes fall, revenue naturally follows. In the first half of FY26, revenue stood at ₹5,659 crore, reflecting continued operational stress.

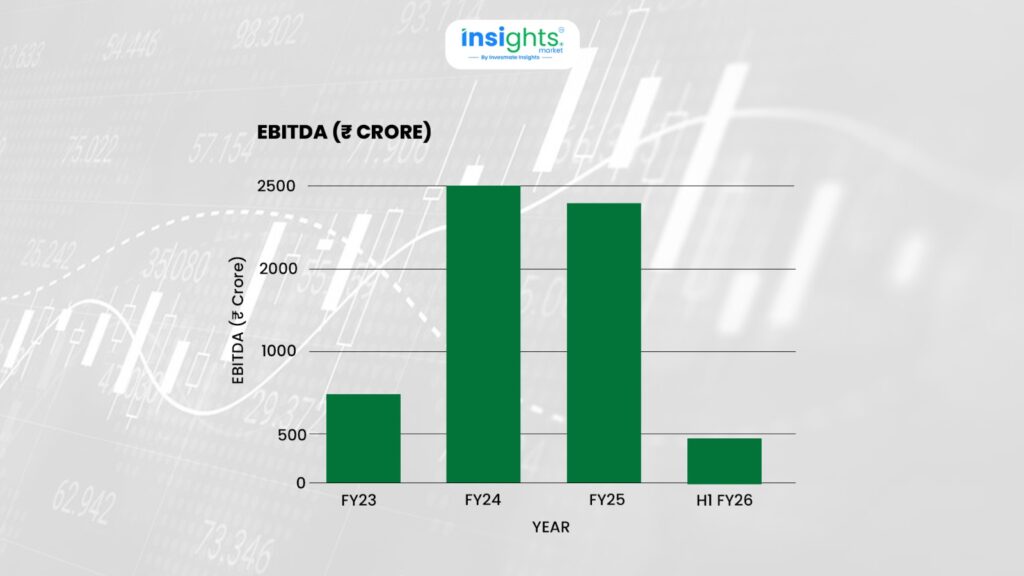

Operating Profit (EBITDA): Efficiency First, Disruption Later

Operating profit, or EBITDA, tells us how efficiently a company runs its core operations. BCCL’s EBITDA improved sharply from ₹891 crore in FY23 to ₹2,494 crore in FY24. This improvement came from better cost control, lower consumption of fuel and explosives, reduced employee costs due to declining headcount, and improved overburden removal efficiency.

In FY25, EBITDA remained relatively strong at ₹2,356 crore, despite lower production. However, the picture changed dramatically in the first half of FY26.

The sharp fall in H1 FY26 happened because:

- Production dropped

- Fixed costs remained

- Infrastructure disruptions affected operations

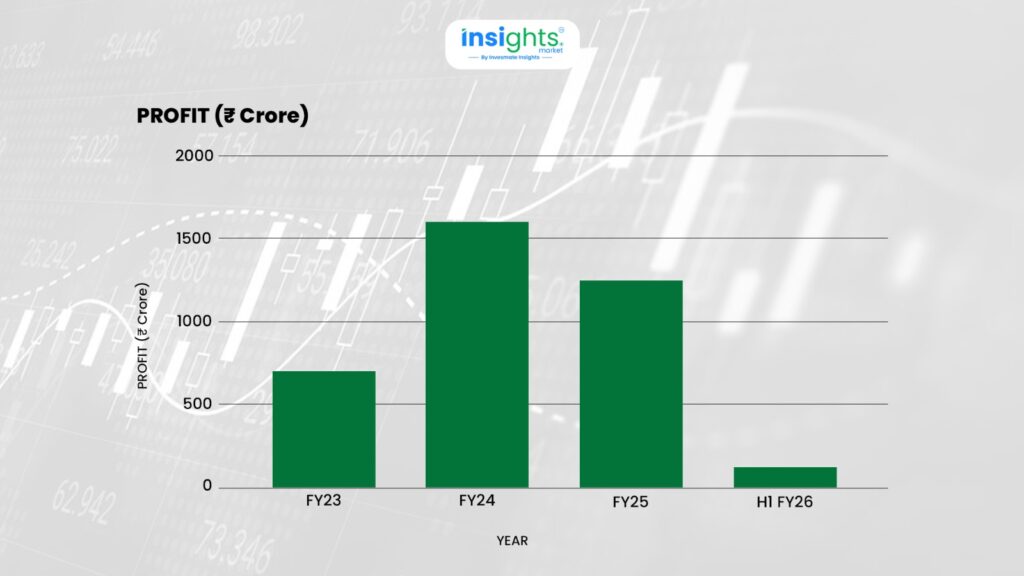

Profit After Tax: The Rise and the Sudden Fall

Profit after tax followed a similar trend. BCCL earned ₹664 crore in FY23, which jumped to a record ₹1,565 crore in FY24. FY25 saw a decline to ₹1,240 crore, largely due to weather-related issues.

In H1 FY26, profit dropped sharply to just ₹124 crore. This was not due to one single factor, but a combination of operational disruption, lower volumes, and rising financial stress.

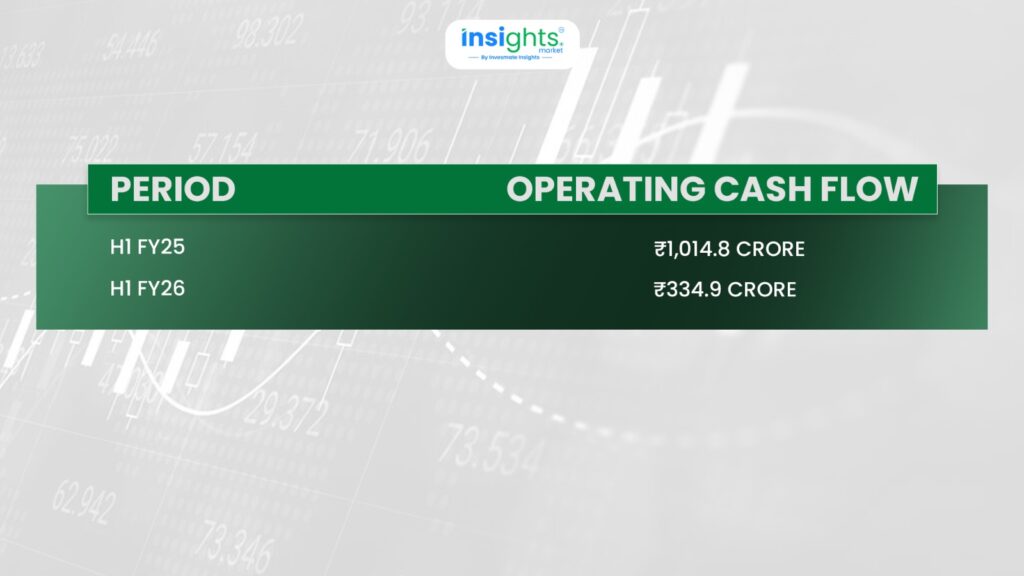

Cash Flow: Where the Real Stress Appears

Cash flow tells us whether profits are actually turning into money.

Cash flow shows whether profits are actually turning into cash. In H1 FY25, BCCL generated operating cash flow of ₹1,014.8 crore. In H1 FY26, this dropped sharply to ₹334.9 crore.

The main reason was delayed payments from customers. Coal was sold, but cash did not come in on time. As a result, BCCL had to rely more on short-term borrowings to fund day-to-day operations.

Working Capital and Receivables: A Key Concern

Receivable days increased from:

- 25 days (FY24)

- To 60 days (Sep 2025)

This shows rising dependence on borrowed money for daily operations.

Infrastructure Shock: Washery Collapse

In September 2025, BCCL faced a major setback when a silo at the Madhuband NLW washery collapsed. This reduced washing capacity by nearly 50%. Since washed coal fetches better realization and is critical for steel customers, this incident directly affects revenue and margins. Reconstruction is expected to take around two years, making this a medium-term operational challenge.

Key Pros & Cons of the BCCL IPO

Shareholder Quota: Special Point

If you held Coal India shares in your demat account until 1 January 2026, you are eligible for a 10% shareholder quota, allowing a separate application (within limits)

Valuation Snapshot

IPO Current GMP Snapshot

Stock / IPO | Grey Market Premium (GMP) | IPO Price | Indicative Listing Gain* |

Bharat Coking Coal (BCCL) | ₹11 | ₹23 | ~47.8% |

* Grey Market Premium (GMP) is an unofficial indicator based on informal market activity.

Bottom Line

The BCCL IPO offers investors a chance to understand and participate in a company that sits at the heart of India’s steel and infrastructure ecosystem. It represents a business with a dominant position in domestic coking coal, large and strategically located reserves, and a long operational history under the Coal India umbrella. At the same time, it reflects the realities of operating in a complex mining environment — including operational disruptions, cash flow sensitivity, customer concentration, and long-term industry transition risks.

In essence, this IPO presents a clear picture of a strategically important but operationally intensive business. Understanding both sides — its scale and its challenges — is key to understanding what the BCCL IPO truly brings to the table.

FAQs

BCCL is a coal mining company primarily engaged in the production of coking coal and non-coking coal. Coking coal is mainly used by steel manufacturers, while non-coking coal is supplied to power and other industrial users. The company operates multiple mines across Jharkhand and West Bengal.

The BCCL IPO is a 100% Offer for Sale (OFS). This means no new shares are issued and the company does not receive any fresh capital from the IPO. The selling shareholder is Coal India Limited.

The IPO includes a shareholder reservation of around 10% for eligible Coal India Limited shareholders. Investors who held Coal India shares on or before the specified cut-off date can apply under this quota, in addition to a regular application, subject to category limits.

BCCL operates in a capital-intensive and cyclical business. Profits depend on factors such as steel demand, coal quality, washery output, mining conditions, and government pricing policies. Because of this, earnings can fluctuate significantly from year to year rather than grow smoothly.

GMP reflects short-term market sentiment and demand for an IPO in the unofficial grey market. It is influenced by speculation and liquidity and does not reflect the company’s fundamentals, financial strength, or long-term performance potential.

Some of the key risks include earnings volatility, operational disruptions, high working capital dependence, contingent liabilities related to litigation, customer concentration in power and steel sectors, and long-term regulatory and environmental risks associated with coal mining.

The information provided in this reference is for educational purposes only and should not be considered investment advice or a recommendation. As an SEBI-registered organization, our objective is to provide general knowledge and understanding of investment concepts.

It is recommended that you conduct your own research and analysis before making any investment decisions. We believe that investment decisions should be based on personal conviction and not borrowed from external sources. Therefore, we do not assume any liability or responsibility for investment decisions made based on the information provided in this reference.