![]()

Did you check your demat account this morning and see HUL’s share price looking weird? Don’t panic. Your money didn’t disappear. Something way cooler just happened instead.

Today, December 5, 2025, Hindustan Unilever (HUL) officially spun off its ₹1,800 crore ice cream business into a brand-new company called Kwality Wall’s (KWIL). And here’s the best part: If you owned HUL shares yesterday, you automatically got free KWIL shares. One share for every share you own. No catch. It’s real.

But here’s the part nobody talks about: The financials reveal why HUL HAD to do this.

The Numbers Tell a Story: Why HUL Split Ice Cream

Let’s look at the real issue hiding in HUL’s recent quarterly results.

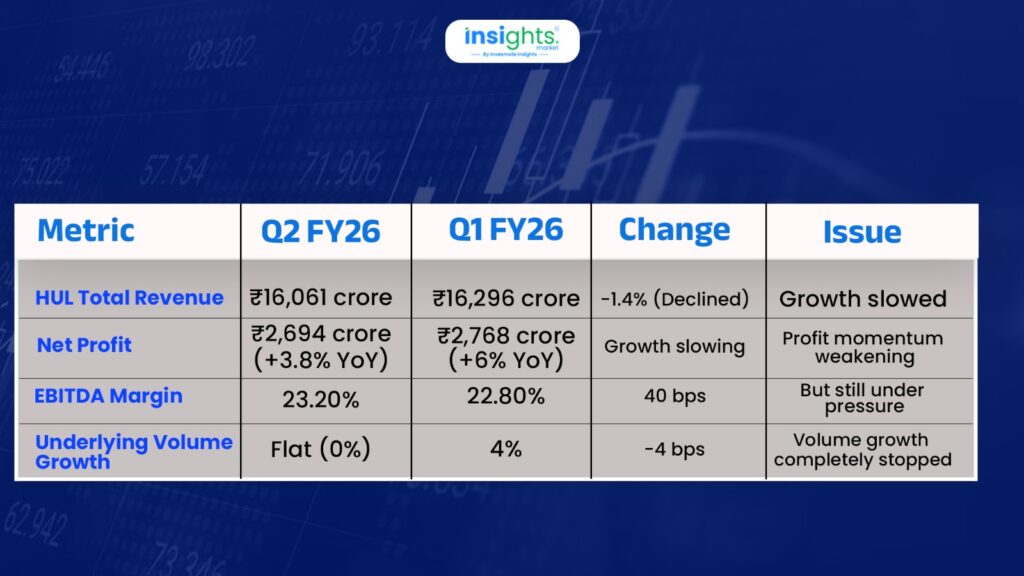

Q2 FY26 Financial Reality:

Here’s what really happened: In Q2 FY26, HUL’s underlying volume growth turned FLAT at 0% YoY—down sharply from Q1’s 4% growth. Revenues barely grew (+2.1%), and while profits grew (+3.8%), that included a one-off tax gain of ₹273 crore. Strip that out, and profit growth looks way more modest.

So why did management spin off ice cream if the overall business already has problems?

The Numbers Tell a Story: Why HUL Split Ice Cream

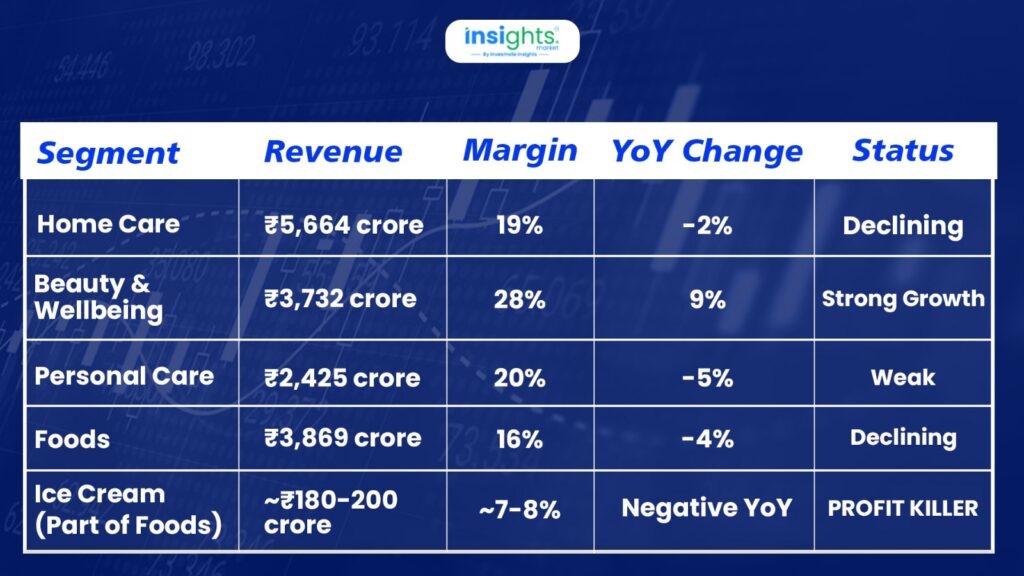

Here’s the brutal truth hiding in segment performance:

Q2 FY26 Segment-wise Performance:

See the problem? Ice cream operates at 7-8% EBITDA margins while HUL’s average is 22-23%. And in Q2, the ice cream segment actually contracted year-over-year due to the extended monsoon and GST reclassification. It’s dragging down the entire Foods segment, which reported -4% growth.

Kwality Wall’s was not “weakening” Hindustan Unilever’s (HUL) financials in an absolute sense, but its performance metrics were

below the average for HUL’s core operations, making it a drag on the overall margins and a distinct business that could operate more effectively independently.

The Margin Squeeze: Ice Cream Is the Culprit

Here’s the financial math that forced the demerger:

HUL’s EBITDA Margin Trend:

- Q1 FY26: 22.8% EBITDA margin

- Q2 FY26: 23.2% EBITDA margin

- Challenge: Margins contracted by 90 basis points YoY (from 24% in Q2 FY25)

Why? Because HUL had to cut prices on 40% of its product portfolio (soaps, shampoos, foods) from 18% GST to 5% GST. This price reduction hit margins hard. Add to that the ice cream segment’s low 7-8% margins, and you’ve got a profitability anchor.

The Math: You Get 1 Free Share for Every 1 You Own

This is dead simple:

That’s it. 1:1 ratio. No dilution. No complications.

TODAY’S 05 Dec’25 MARKET ACTION: HERE’S EXACTLY WHAT HAPPENED

You probably noticed HUL’s price looked different this morning compared to yesterday’s ₹2,464 close.

Here’s exactly what went down:

The Price Discovery Session: NSE and BSE ran a special one-hour auction at 9 AM. The market figured out: What’s HUL worth without ice cream? After the price discovery session, HUL opened at ₹2,424 (down 1.5%).

The Intraday Roller Coaster: Throughout the day, HUL saw heavy SELLING pressure, plunging as low as ₹2,289—a sharp 7% drop.

But then something interesting happened. Smart money started buying the dip. By afternoon, HUL recovered and closed at ₹2,338.60, ending down 3.44% (or 3.7% depending on final prints).

Here’s the actual math:

₹2,464 (yesterday’s close) minus ₹2,424 (today’s opening after price discovery) = approximately ₹40 per share

That ₹40 per share is your ice cream value now assigned to KWIL shares.

Think about it:

Time | Price | %Change | Sentiment | Why |

Opening (9:30 AM) | ₹2,424 | -1.5% | Cautious | Price discovery started |

Intraday Low (11:00 AM) | ₹2,289 | -7% | PANIC | Retail investors saw red, didn’t understand the demerger |

Midday (12:30 PM) | ₹2,345 | -3.2% | Stabilizing | Smart money realized it’s a value split, not a loss |

Close (3:30 PM) | ₹2,338 | -3.44% | Accepted | The market digested the demerger |

The market wasn’t saying “HUL is worth less.” It was saying “HUL’s composition changed, so fair value recalibrated.” By the close, that recalibration was accepted.

When Will You See These New Shares?

By December 29, 2025, KWIL shares will be credited to your demat account automatically (if your KYC is done, which it probably is). You’ll get an email notification.

January-February 2026: KWIL starts trading on NSE and BSE. That’s when you can actually sell if you want. Until then, the shares are frozen in your account.

Analyst estimates: When KWIL lists, it could open between ₹50-₹60 per share. But that’s just guessing. The market will decide the real price on Day 1.

Why Did HUL Split Its Ice Cream Business?

Ice cream and soaps are completely different businesses.

Ice cream:

- Seasonal (summers = boom, winters = dead)

- Needs expensive cold-chain infrastructure

- Runs on thin margins (7.1%)

Soaps:

- Stable year-round

- High margins (22-23%)

- Predictable

By splitting:

- KWIL moves fast like a startup, perfect for chasing summer demand

- HUL gets cleaner financials—instantly +50 basis points (0.5%) margin boost

- Investors get options—stable HUL or high-growth KWIL

- Global strategy—parent Unilever is doing this worldwide

What's Inside Kwality Wall's?

KWIL gets these iconic ice cream brands:

- Kwality Wall’s (the classic)

- Magnum (premium)

- Cornetto (the cone)

- Feast (value)

- Creamy Delight (budget)

The scale: ₹1,800 crore annual revenue. India’s #2 ice cream player. Over 2,00,000 cold cabinets have already been built across India.

Management's Growth Plan

HUL CEO Rohit Jawa called this a “high-growth business” that will “unlock fair value for shareholders.“

KWIL’s playbook:

- Expand cabinets from 2,00,000 to millions (there are 40-50 lakh retail points in India)

- Push premium brands (Magnum & Cornetto) from 12-15% of sales to 18-22% by 2031

- Dominate quick-commerce (Blinkit, Zepto, Instamart)—ice cream is impulse purchase gold

- Ride the GST wave—if ice cream GST cuts from 18% to 5%, the market explodes

For HUL post-demerger:

- Mid-single digit volume growth expected in H2 FY26

- EBITDA margins stay at 22-23% (including the +50bps boost)

- EPS growth ~8.3% annually through FY28

- Sharper focus on premium and wellness products

The Hidden Signal: ₹19 Interim Dividend Amid Demerger

Here’s something investors missed: Right before the demerger, HUL announced an interim dividend of ₹19 per share for FY26.

Why This Matters:

An interim dividend is management saying, “We’re confident enough in cash flows to pay you early.” This wasn’t forced. This was confidence.

Translation of the Signal:

- Management believes post-demerger HUL will generate even MORE cash

- They’re comfortable returning ₹19 per share while investing in growth initiatives

- The dividend + free KWIL shares = total shareholder value unlock

For You as Investor:

If you held HUL on Nov 7 (dividend record date), you got ₹19 dividend PLUS you’re getting free KWIL shares. Double win.

Real Talk: What Could Go Wrong?

KWIL isn’t guaranteed to moon:

Seasonality bites hard: Summer boom, winter crash. Expect volatile quarterly results.

Margins are weak right now: H1 FY26 margins hit near-zero due to cocoa inflation and GST reclassification. Competitors like Vadilal and Havmor run at 17-18% margins. KWIL has to catch up.

Capex is hungry: Expanding cabinets requires serious cash for manufacturing and distribution.

Watch quarterly results carefully. That’s where you’ll see if management can actually fix margins.

The Real Opportunity

KWIL starts with challenges (thin margins, seasonality, capital needs). But it has massive advantages that most startups don’t:

- Iconic brands with 70+ years of heritage

- 2,00,000 cold cabinets already built

- Unilever’s global R&D backing

- 2nd market position in India’s ice cream market

- High-growth category (ice cream growing faster than the overall FMCG)

If KWIL executes on premiumization, cabinet expansion, and GST benefits, it could see massive re-rating once margins normalize.

For HUL? The +50bps margin boost plus a focused strategy on core FMCG could drive solid EPS growth.

Timeline for Investors: What to Watch

The Bottom Line

Today marks a historic split in India’s FMCG. One company became two. The financials show why HUL HAD to do this:

- Ice cream is dragging the margin profile down

- Capital-heavy, low-return category

- Seasonal volatility hiding in consolidated numbers

- Diverting capital from higher-margin opportunities (Beauty & Wellbeing at 28% margins)

By December 29, you’ll have shares in both: leaner, more profitable HUL + growth-focused KWIL.

Stay invested. Monitor quarterly margins. Stay cool. 🍦

FAQs

HUL split its ₹1,800 crore ice cream business into Kwality Wall’s (KWIL) on December 5, 2025. Ice cream ran at 7-8% EBITDA margins vs HUL core at 22-23%, and in Q2 FY26, the segment declined YoY, dragging overall profitability. Separation gives HUL an immediate +50-60 bps margin boost while KWIL can pursue growth independently. It’s a win-win: HUL becomes leaner and more profitable; KWIL becomes a focused high-growth play.

No. The 7% intraday drop was panic selling. Yesterday’s ₹2,464 included both soaps and ice cream. Today, HUL (soaps only) closed at ₹2,338 (-3.44%); the ice cream value (~₹40-55/share estimate) moved to free KWIL shares (allotted later). You didn’t lose value — it was reorganised into two buckets. Smart money realised this and bought the dip, recovering the stock from its -7% low.

By December 29, 2025: KWIL shares credited to demat accounts if KYC is compliant (1 KWIL per 1 HUL held on Dec 4). Jan–Feb 2026: KWIL lists on NSE/BSE and trading begins. Analyst estimates: Nuvama expects a ₹50-60 listing range (5x EV/Sales), but the actual price depends on market demand.

Kwality Wall’s portfolio includes Kwality Wall’s, Magnum, Cornetto, Feast, and Creamy Delight, generating ~₹1,800–2,000 crore annually. KWIL has over 2,00,000 cold cabinets across India — strong brands and massive distribution, but a business model that needs different capital and strategy than soaps.

No dilution. For every 1 HUL share you own you get 1 free KWIL share. Example: 50 HUL → 50 HUL (now ~₹2,338) + 50 KWIL (~₹50-60 est.). Total value is reorganised; slight differences reflect market recalibration (KWIL trading at a lower multiple).

Profitability: HUL gets ~+50–60 bps EBITDA margin improvement (from ~23.2% to ~23.7–23.8%) as ice cream leaves. Management guidance: ~8.3% EPS CAGR FY26–28. Capital can be redeployed into higher-margin categories (Beauty & Wellbeing). Dividends: HUL announced an interim ₹19/share (record date Nov 7, paid Nov 20), signalling confidence in cash flows; post-demerger dividends should be structurally stronger.

The information provided in this reference is for educational purposes only and should not be considered investment advice or a recommendation. As an SEBI-registered organization, our objective is to provide general knowledge and understanding of investment concepts.

It is recommended that you conduct your own research and analysis before making any investment decisions. We believe that investment decisions should be based on personal conviction and not borrowed from external sources. Therefore, we do not assume any liability or responsibility for investment decisions made based on the information provided in this reference.