![]()

If you’ve been shopping online across India, chances are you’ve used Meesho without even realizing it. Meesho Limited, the much-anticipated e-commerce unicorn, is set to open its IPO doors on December 3-5, 2025. If you’re seeing this blog, you’re likely confused about whether to invest or stay away. That’s exactly what this guide is for.

Over the last three years, Meesho has built something remarkable: an e-commerce platform with 234 million annual users and 1.59 billion orders placed in a single year. But it has also accumulated massive losses. The company claims it’s the leader in its space, but the financial numbers raise serious questions.

This blog breaks down everything you need to know—the good, the bad, and the risky—so you can make an informed decision.

What Exactly is Meesho? The Company Behind Your Online Shopping

Meesho started in 2015 and has been operating for 10 years. But here’s what makes it special: it’s built for India’s small towns and Tier-2 and Tier-3 cities, where people don’t have fancy branded stores or quick delivery options.

Think of it this way:

- Amazon and Flipkart = Big brands, expensive, fast delivery (but not everywhere)

- Meesho = Affordable products, unbranded items, sellers from small cities, delivered through social media sharing

Meesho works like this: Small sellers (homemakers, students, entrepreneurs) can sell products through WhatsApp and Instagram without needing big warehouses or spending tons of money on marketing. Buyers get cheap products. Meesho makes money by running ads and offering services to these sellers—not by taking a commission like other platforms.

The scale is massive:

- 234 million annual users

- 575,000 active sellers

- 1.59 billion orders shipped in just one year

This makes Meesho the number one e-commerce platform in India by order volume.

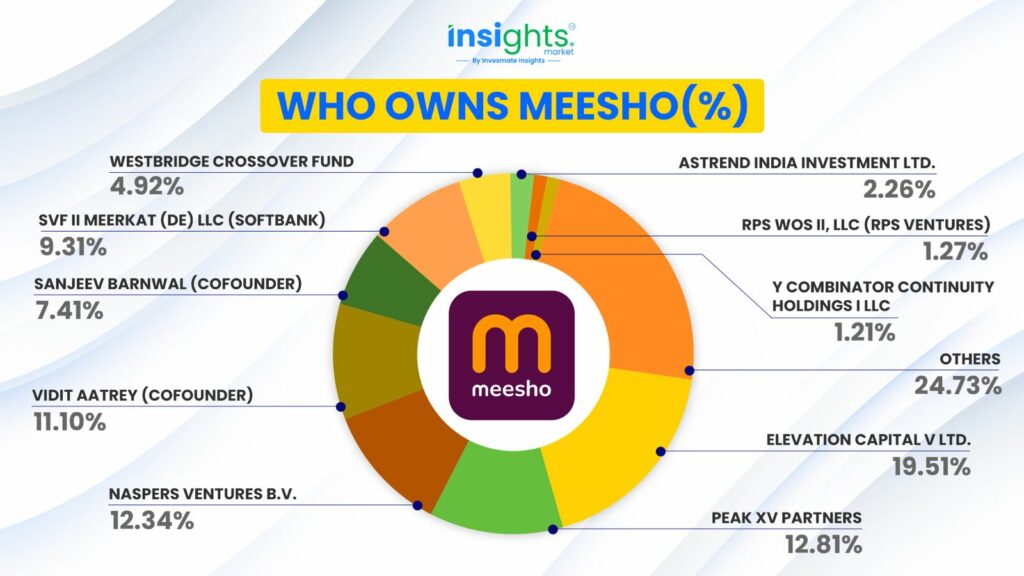

Who Owns Meesho? The Shareholders and Founders

Before investing, it’s important to know who owns this company and whether they’re committed to it.

Current Ownership Structure:

Vidit Aatrey holds 11.1% pre-IPO and is selling 11.7 million shares, while Sanjeev Barnwal holds 7.41% and is also selling around 11.7 million shares. Together, the founders hold 18.51% and will offload roughly 23.4 million shares. Among investors, Elevation Capital holds 19.51% and is the largest seller with 55.4 million shares, followed by Peak XV Partners (Sequoia) with a 12.81% stake, selling up to 30.5 million shares.

IPO Details at a Glance - What's Being Offered

Share Allocation Across Investor Types:

- QIBs (Large institutional investors): At least 75%

- Non-Institutional Investors (HNIs): Up to 10%

- Retail Investors: Up to 15%

Registrar: Kfin Technologies Private Limited

Where is Meesho Spending Your Money?

Meesho is investing heavily in technology infrastructure, not just burning money on discounts—a positive signal for long-term sustainability.

The Business Model Challenges - Understanding the Key Risks

The AWS Legal Dispute

Meesho is in a legal dispute with Amazon Web Services (AWS) over cloud services.

What happened: In 2022, Meesho signed a contract with AWS promising a minimum spend for discounted rates. Issues arose when Meesho claimed AWS services were unreliable, causing app disruptions. Meesho moved to another provider and refused full payment.

The numbers:

- AWS’s demand: ₹127.45 crore

- Meesho’s counter-claim: ₹86.5 crore

- Current status: Pending arbitration in New Delhi

Investor perspective: This is small (less than 3% of the IPO size) and disclosed transparently in official documents. However, it remains a contingent liability worth monitoring.

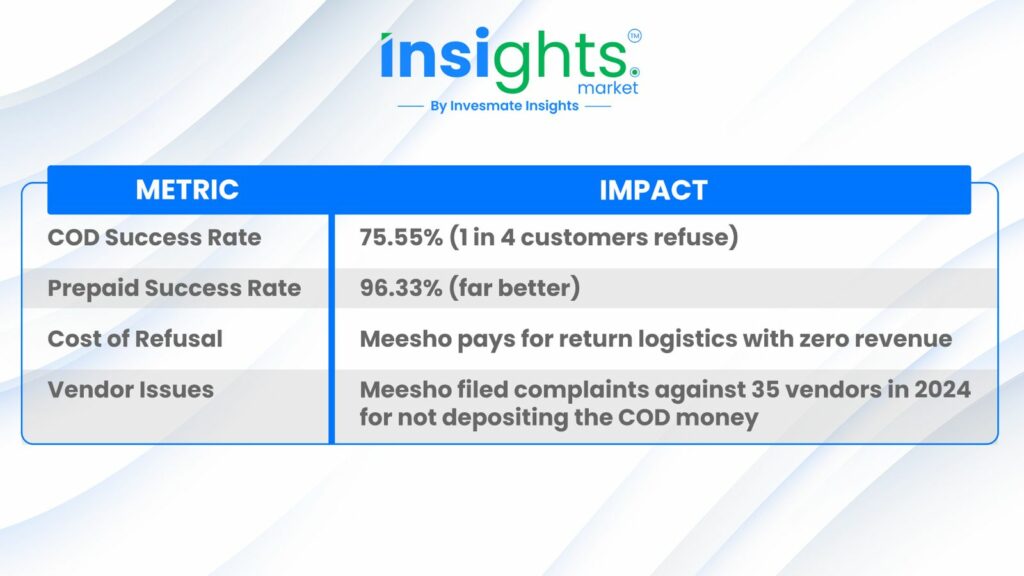

The Cash-on-Delivery Challenge

Here’s a problem that directly impacts profitability: 76.95% of orders are COD (cash-on-delivery).

Why is this risky?

When customers refuse COD orders, Meesho absorbs both forward and reverse delivery costs—essentially losing money on that transaction. This directly eats into margins.

The company is addressing this by offering incentives for digital payments, but COD dependency remains a significant operational challenge.

Why Meesho’s Zero-Fee Strategy Is a Red Flag for Investors

Another key concern is Meesho’s refusal to introduce even a nominal platform fee, despite its potential to improve profitability instantly. During the IPO process and in a recent interview, the management reiterated that Meesho will stick to a zero-commission, zero-platform-fee model.

Analysts point out that with an estimated 280 crore orders in FY26, a simple ₹1 platform fee could add around ₹280 crore to Meesho’s profit—without affecting customer behaviour. Yet the company chose not to adopt it, prioritising customer trust over monetisation.

This approach strengthens Meesho’s brand, but raises an important investor question: If the company avoids easy revenue levers, how quickly can fundamentals improve? Like early Apple under Steve Jobs, product focus alone may not translate into shareholder returns unless monetisation eventually scales.

Meesho may build a strong ecosystem over time, but profitability could take longer—making this a crucial risk for IPO investors to consider.

Regulatory Crackdown: CCPA Imposes Record ₹210 Lakh Penalty on Meesho

Meesho was recently hit with a record ₹210 lakh CCPA penalty for allowing uncertified walkie-talkies on its platform—far higher than fines on peers. The order highlighted gaps in seller checks and delayed compliance. This adds a credible regulatory risk for investors to consider ahead of the IPO.

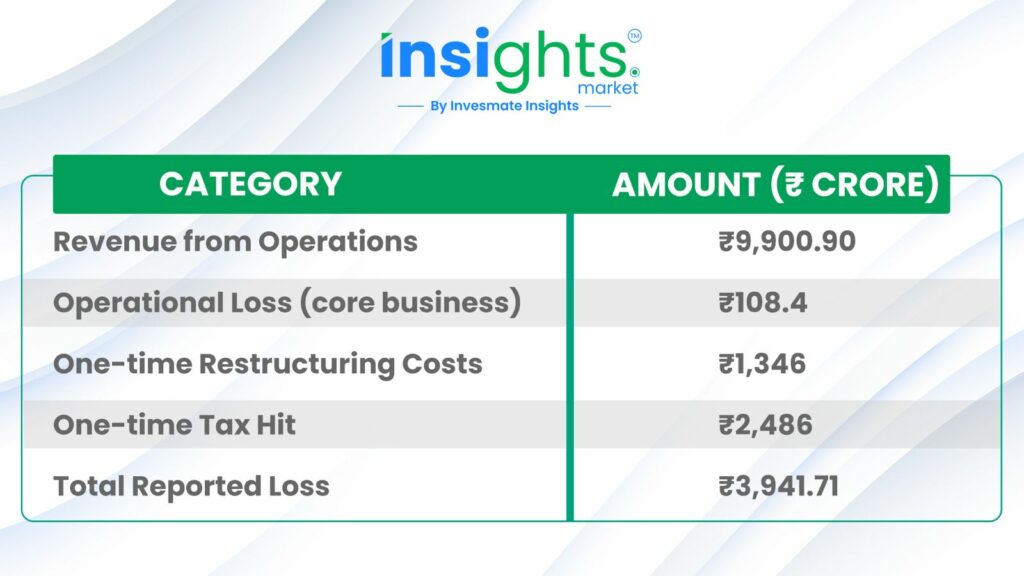

Understanding the Loss Situation

Meesho reported a loss of ₹3,941.71 crore in FY25, which sounds alarming. Here’s what actually happened:

Real translation: Of ₹3,941.71 crore in reported loss, ₹3,833 crore came from one-time costs (restructuring and tax adjustments related to moving headquarters from the US to India). These won’t repeat.

Meesho's Financial Performance Across Four Periods: Revenue Growing, Profitability Still Challenged

Meesho has shown sharp operational improvement from FY23 to FY25, with losses narrowing consistently as monetization strengthened and costs came under control. However, the early FY26 trend is concerning, with the annualized H1 operational loss rising again, indicating renewed pressure on margins. EBITDA mirrors this pattern—significant improvement through FY25 but still negative—showing that while efficiency has improved, the business has not yet reached sustainable profitability.

Complete Financial Picture - What The Numbers Really Say

Meesho’s revenue trajectory shows strong, consistent growth, with a ~28% CAGR over the last three years. FY26 is already trending ahead, indicating sustained momentum and continued scalability of the business model. The steady rise reinforces that Meesho is effectively expanding its platform while maintaining healthy top-line acceleration.

Balance Sheet Metrics:

- Cash in hand: ₹147 crore (low)

- Total debt: ₹0 (zero!)

- Net Worth: ₹1,561.88 crore (declining)

- Assets: ₹7,226.09 crore (FY25)

Key Observations:

- Zero debt is positive (no creditor pressure)

- Low cash reserve explains why the IPO is needed now

- Declining net worth is concerning

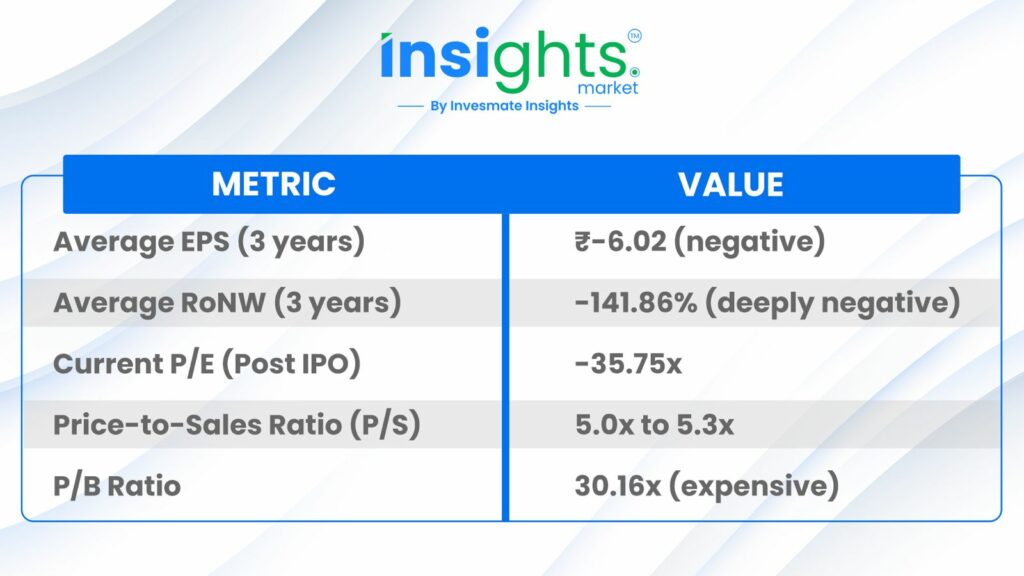

Profitability Metrics:

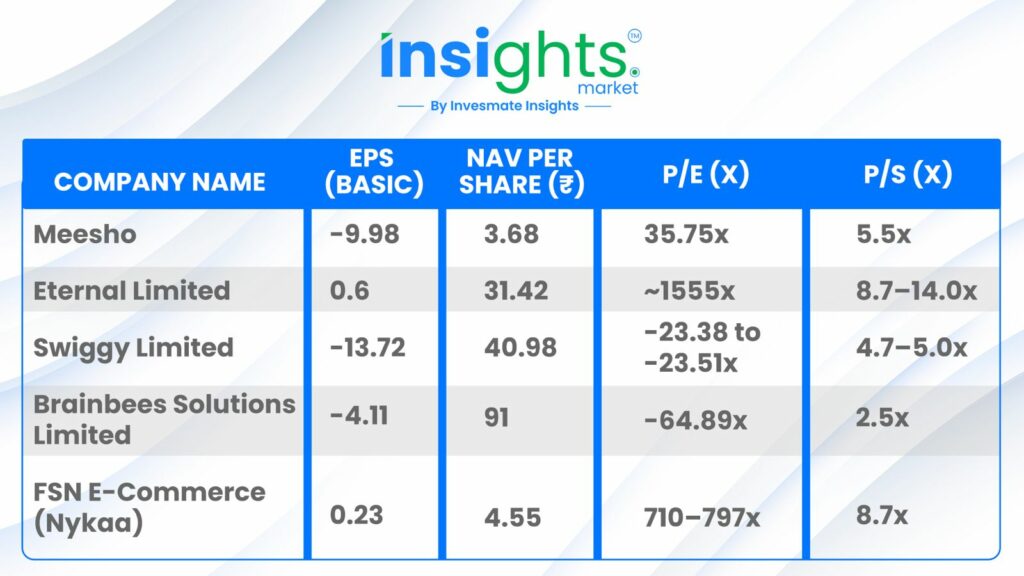

How Does Meesho Compare to Listed Peers?

Among its peers, Meesho trades at a comparatively lower P/S multiple of 5.0x–5.3x, versus Zomato at 9.3x and Nykaa at 8.6x, making it cheaper on a sales-multiple basis. However, its negative EPS and deeply negative RoNW show that profitability is still a challenge, especially compared to profitable peers like Eternal or high-growth leaders like Nykaa. Overall, the valuation discount suggests the market is pricing in Meesho’s losses—but whether it becomes an attractive value ultimately depends on confidence in Meesho’s path to sustainable profitability.

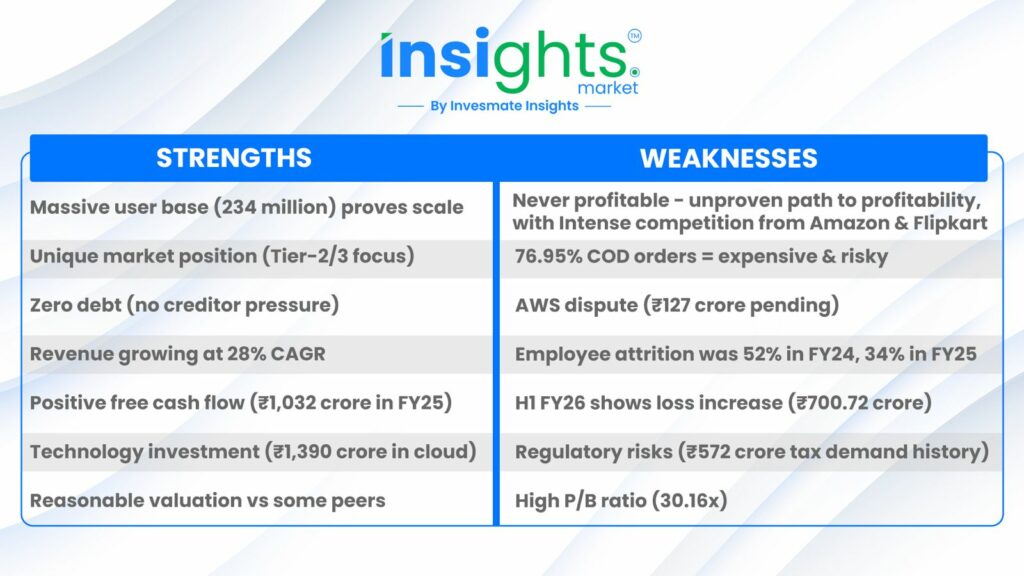

Strengths and Weaknesses - A Balanced Comparison

Grey Market Premium (GMP) - What Investors Are Expecting

Date | IPO Price Band | Grey Market Premium | Estimated Listing Price |

10/12/2025 (Listing) | ₹111 | ₹42.05 | ₹153 (37.84%) |

09/12/2025 | ₹111 | ₹36.00 | ₹147 (32.43%) |

08/12/2025 (Allotment) | ₹111 | ₹39.00 | ₹147 (32.43%) |

Verification Checklist - Before You Apply

Before bidding, verify:

✓ You have a demat account active and ready

✓ You have sufficient funds in your account

✓ You understand the risks outlined in this blog

✓ You can afford to lose this investment

✓ You’ve read the official prospectus (available on BSE/NSE websites)

✓ You have realistic expectations (GMP is zero, no guaranteed listing gains)

✓ You’re comfortable with a 2-3 year holding period minimum

✓ You’ve consulted with a financial advisor if needed

How to Apply for Meesho IPO

Open a demat account with any broker

→ Add at least ₹14,985 to your trading account (more if applying for multiple lots)

→ Go to the IPO section in your broker’s app or website

→ Select the Meesho IPO and place your bid at ₹105–₹111 per share

→ Approve the bank mandate to block funds

→ Wait for allotment results on December 8, 2025 (check via PAN or broker app)

→ If allotted, shares will list and start trading on BSE & NSE on December 10, 2025

Bottom Line

Meesho’s IPO offers high growth potential but comes with equally high execution risk. It’s a bet on a fast-scaling business with strong revenue momentum and cash generation, but that still lacks proven profitability. Only investors with a long-term horizon and the ability to absorb volatility should consider participating; conservative investors may be better off staying cautious.

Disclaimer

This blog is for educational and informational purposes only. It is NOT investment advice. Before investing in any IPO, please consult a SEBI-registered financial advisor and conduct your own due diligence. Read the DRHP carefully and understand all risk factors.

Happy Investing!

FAQs

Meesho targets affordable, unbranded products in Tier-2/3 cities, while Amazon and Flipkart focus on branded convenience for metro users. They operate in different segments and can coexist.

It’s uncertain, but the trend is improving. If losses keep narrowing at the current pace, profitability may emerge by FY26 or FY27—though there is no guarantee.

It’s a risk to watch, but not a deal-breaker. The ₹127 crore claim is small relative to the IPO size, and similar disputes are common. The issue is fully disclosed in regulatory filings.

₹14,985 for one lot (135 shares) at the upper price band of ₹111 per share.

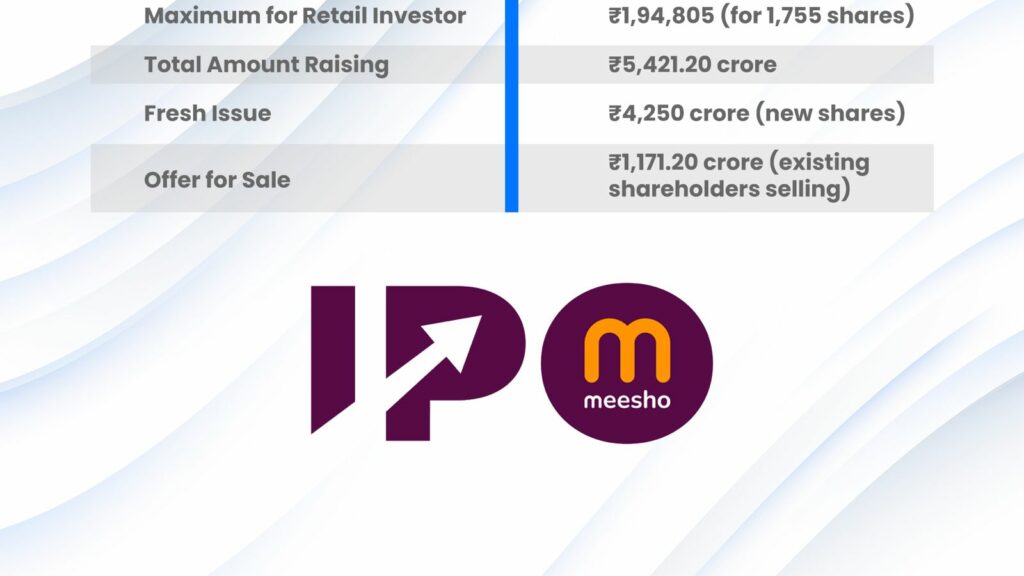

Meesho is raising a total of ₹5,421.20 crore through its IPO. This includes a fresh issue of ₹4,250 crore, where new shares are being created, and an offer for sale (OFS) of ₹1,171.20 crore, where existing shareholders are selling their shares. In total, the IPO consists of around 38.29 crore fresh issue shares and 10.55 crore OFS shares.

Meesho plans to utilize the ₹4,250 crore fresh issue proceeds mainly to strengthen its technology and growth initiatives. About ₹1,390 crore will go toward cloud infrastructure, ₹480 crore for expanding its AI and machine learning talent, and ₹1,020 crore for marketing and brand-building efforts. The remaining funds will be used for inorganic growth opportunities and general corporate purposes. This allocation shows a focus on long-term sustainability and technology-driven expansion.

Meesho operates a zero-commission marketplace that connects sellers, buyers, logistics partners, and content creators. Instead of charging commissions like other e-commerce platforms, Meesho earns revenue through advertising, seller services such as fulfillment and analytics, and logistics services through its Valmo subsidiary. Its model is especially suited for affordable, unbranded products catering to Tier-2 and Tier-3 cities, which differentiates it from platforms like Amazon and Flipkart.

The information provided in this reference is for educational purposes only and should not be considered investment advice or a recommendation. As an SEBI-registered organization, our objective is to provide general knowledge and understanding of investment concepts.

It is recommended that you conduct your own research and analysis before making any investment decisions. We believe that investment decisions should be based on personal conviction and not borrowed from external sources. Therefore, we do not assume any liability or responsibility for investment decisions made based on the information provided in this reference.