![]()

Hey there, money-savvy friend! If you’ve been hearing about the RBI’s big bang announcements and wondering what it all means for your wallet, you’re in the right place. Let’s make sense of it together…

1. What Just Happened? The Big Story

Let’s take a quick look at repo rate trends…

Repo Rate Cut:

The RBI slashed its key interest rate,the repo rate by a whopping 50 basis points (0.5%) to 5.5%, the lowest in nearly three years.

Read Also: RBI’s Repo Rate Cut: A Game-Changer for Borrowers and Markets

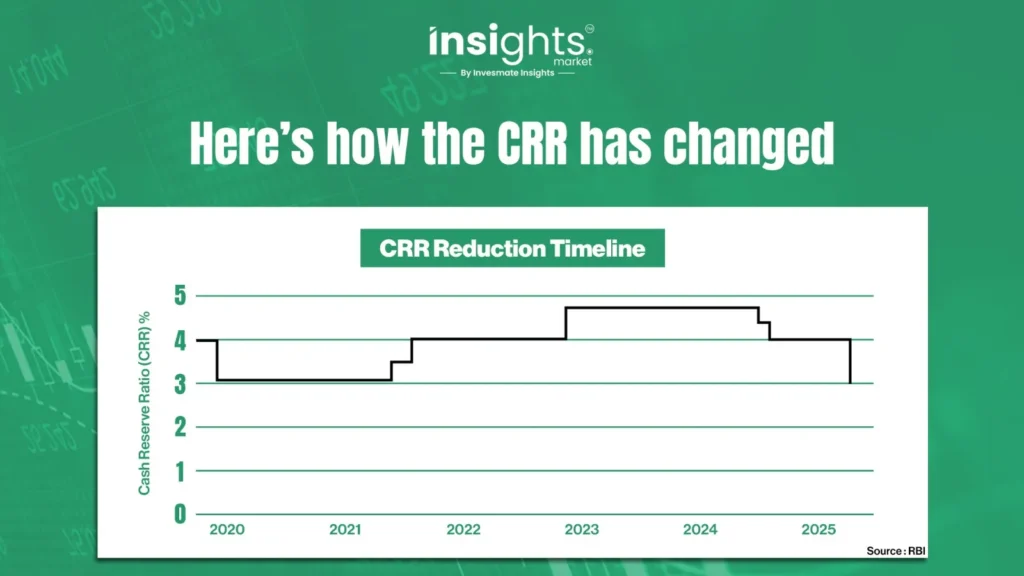

CRR Cut:

The Cash Reserve Ratio (CRR)—the slice of deposits banks must keep with the RBI—was cut by 100 basis points (1%) to 3%.

Here’s how the CRR has changed

But Why Now?

Inflation is under control, and the RBI wants to give the economy a boost.

Let’s get to know about it in detail below..

2. Why Did the RBI Do This? The Inside Scoop

The Analogy:

Think of the RBI as the “banker to the banks.” When it cuts the repo rate, it’s like giving banks a discount on the money they borrow. The CRR cut? That’s telling banks, “You don’t have to keep as much money in your piggy bank,go ahead and lend more!”

The Real Reasons

Alright, let’s get real: why did the RBI hit the brakes on interest rates and free up more cash for banks? It’s not just a random decision!

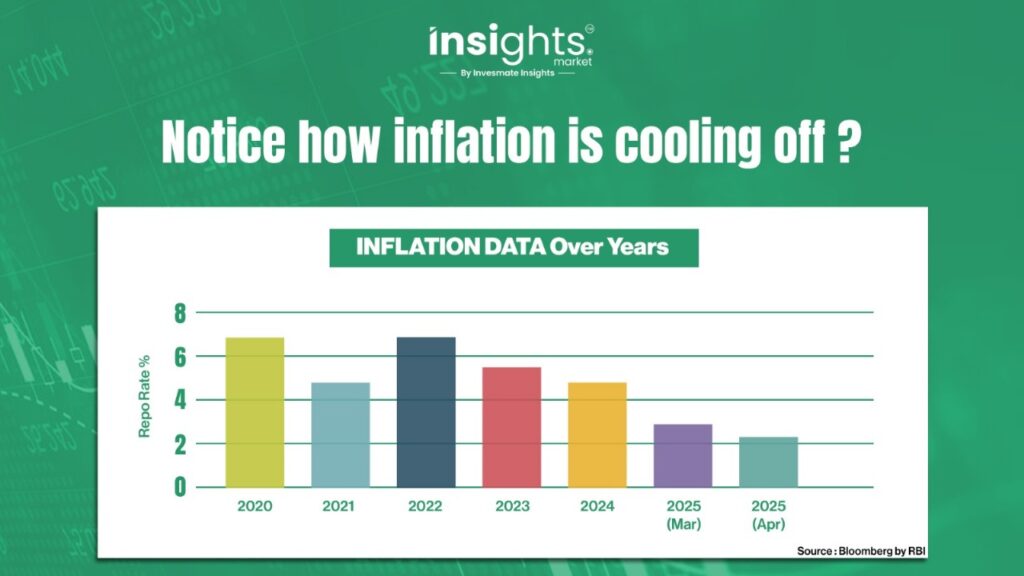

Notice how inflation is cooling off?

Imagine this:

You’re the boss of all banks—like the head coach of a cricket team. You see your star players (banks) are a bit nervous because inflation is low (meaning prices aren’t rising too fast), and the economy needs a little push to keep scoring runs (growing!).

So, what do you do? You give them a pep talk and a secret weapon: cheaper money (the repo rate cut) and permission to play with more of their cash (the CRR cut). That’s exactly what the RBI did!

Here’s the play-by-play:

- Inflation is Under Control: Prices are rising at a gentle pace—just 3.16% in April, way below the RBI’s 4% target. That’s like a bowler hitting the right line and length, keeping things steady.

- Economy Needs a Boost: The world economy is a bit shaky, and India’s growth needs to stay strong. The RBI wants to make sure we keep hitting those sixes—more spending, more investment, more jobs!

- Policy Stance: The RBI has moved from “let’s keep cutting rates” (accommodative) to “let’s wait and watch” (neutral). Think of it as taking a strategic timeout to see how the match is going.

3. How Does This Affect You? Let’s Talk Money!

Now, let’s get to the important part—how does all this RBI action actually touch your life? Whether you’re a borrower, a saver, or an investor, here’s the scoop:

If You’re a Borrower (or Dreaming of a Loan)

- Cheaper Loans: Home, car, and personal loans just got a whole lot more affordable! If your loan is linked to the repo rate, your EMI could drop by a nice chunk. Imagine paying a little less every month, that’s extra cash for your next adventure!

- Business Boost: If you’re running a business or planning to start one, banks now have more money to lend at lower rates. That means easier access to credit for your dreams and ideas.

If You’re a Saver (or Love Your Fixed Deposits)

- Lower Interest on Deposits: Fixed deposits and savings accounts might not give you as much interest as before. It’s like your favorite ice cream shop reducing the number of scoops and time to look for new treats!

- Time to Invest? With lower returns on savings, maybe it’s a good time to explore other options like mutual funds or stocks. Think of it as trying a new flavor—you might just love it!

Read Also: Understanding Value Investing: A Simple Guide For Beginners

5. What’s Next? The Crystal Ball (With a Pinch of Fun!)

Alright, let’s peek into the future—what can you expect after this RBI fireworks show? Grab your popcorn, because the next few months are going to be interesting!

CRR Cut Rollout: The Grand Plan

Think of the CRR cut as a surprise gift that’s being unwrapped in four parts. Starting September 6 and ending November 29, 2025, banks will get a fresh injection of ₹2.5 lakh crore. That’s like getting a box of chocolates, but instead of eating them all at once, you get a piece every few weeks!

Will Loans Get Cheaper Faster?

The RBI expects banks to pass on the rate cuts to short-term loans pretty quickly—like a relay race where the baton (cheaper money) gets handed over fast. But for home loans and other big-ticket items, it might take a bit longer. Don’t worry, though the benefits will reach you, just with a little lag, like your favorite TV show’s next episode.

Pause Ahead? The RBI’s Next Move

Most economists think the RBI is done with big rate cuts for now. Unless something wild happens, like a global shock or a sudden spike in inflation the RBI is likely to keep rates steady for the rest of the year. Think of it as the RBI taking a breather after a marathon, waiting to see how the race unfolds.

Now What About the Economy?

The RBI’s latest moves cutting the repo rate and CRR are like giving the Indian economy a much-needed energy drink. With inflation under control and growth momentum on track, these policy changes are set to make loans cheaper, boost business activity, and put more money in the hands of both consumers and entrepreneurs. Sure, savers might see lower returns on deposits, but the bigger picture is a more vibrant, opportunity-filled economy.

As always, the RBI is keeping a close eye on global risks and stands ready to act if needed. For now, whether you’re planning a big purchase, thinking about investing, or just watching the markets, these changes could open up new doors.

Don’t forget to tell us, What do you think about the RBI’s move?

Are you excited about cheaper loans, or worried about lower returns on your savings?

Drop a comment below—we’d love to hear your thoughts!

FAQs

Yes, if your loan is linked to the repo rate, your EMI will drop as banks pass on the rate cut.

Banks usually lower EMIs for repo-linked loans almost immediately, but full changes may take a few weeks to show up.

Lock in higher FD rates now if you can, as banks may cut rates further. Or, consider debt mutual funds for better returns.