![]()

You’re scrolling on your phone when a notification appears: “Buy gold from ₹1!” It sounds amazing, right? But on November 8, 2025, SEBI issued a major advisory that has made many digital gold investors anxious.

Interestingly, this warning came at a time when gold prices reached an all-time high in 2025, rising 66% year-to-date and exceeding ₹1,20,000 per 10 grams.

What makes this warning even more important? In recent years, the digital gold market has grown rapidly, shifting from a niche offering to a mainstream investment category.

The Growth Story of Digital Gold

From just a few million investors and a handful of tonnes traded, digital gold has now become a household financial product in India. But what exactly about this explosive growth made SEBI raise its eyebrows?

Let’s break down what this SEBI warning means for your wallet.

What Exactly Is Digital Gold?

Over the past decade, India’s financial landscape has seen a wave of new ideas. One such idea is digital gold. It was promoted as an easy way to own gold in today’s digital world.

Why let your savings collect dust when you can convert ₹100 into 24-karat gold in seconds? With just a tap on an app, your gold is bought and stored safely in a vault under your name—no locker, no paperwork, just a digital certificate that proves your ownership.

Indians, who have always had a strong connection to gold, took to it eagerly. Based on transaction data, UPI transactions in digital gold rose from about ₹760 crore in January 2025 to nearly ₹1,180 crore by August. This increase shows how well the combination of tradition and technology appealed to investors.

Using platforms like Paytm, PhonePe, and Google Pay, people can buy or sell gold anytime, starting from as little as ₹1. But as this new shiny trend gained popularity, SEBI’s recent warning reminded us that not everything that glimmers on your screen is risk-free gold.

SEBI’s November 2025 Warning: The Core Issue

SEBI issued a caution notice stating one thing crystal clear: digital gold is completely outside their regulatory framework. This means digital gold isn’t regulated by SEBI like stocks or mutual funds. It’s also not classified as a commodity derivative like gold futures on MCX.

Translation? If something goes wrong, SEBI can’t help you. Your platform could shut down, the vault could have problems, or charges could mysteriously increase—and SEBI has zero authority to intervene.

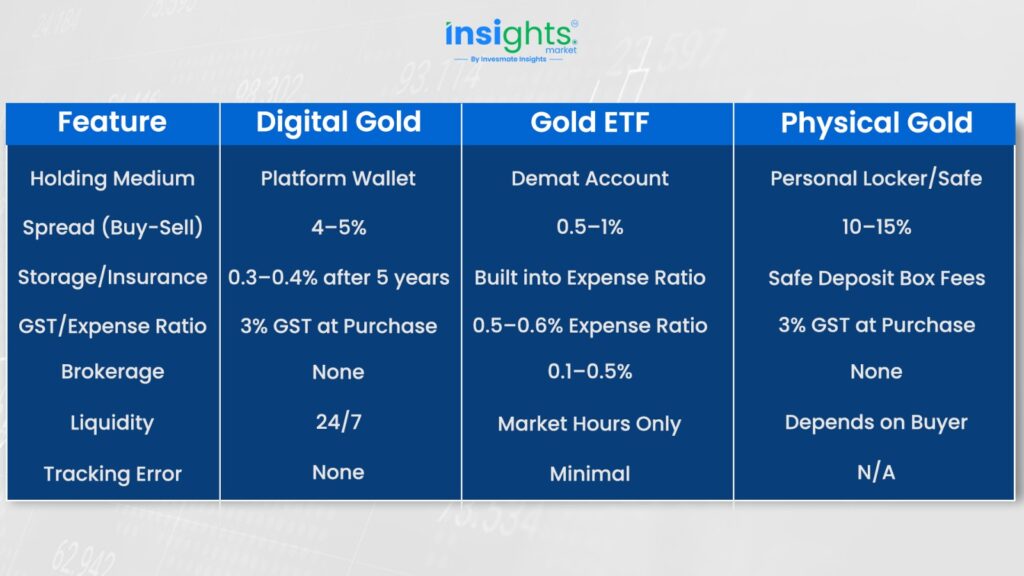

Digital Gold vs Gold ETF vs Physical Gold: The Real Comparison

Notice the spread difference? Digital gold at 4-5% versus Gold ETF at 0.5-1%. That’s the opacity cost.

The Pricing Problem: Opacity Over Transparency

Regulated markets require clarity—ETFs publish daily NAVs, provide buy-sell prices, and disclose expense ratios. You always know what you’re paying for.

Digital gold? None of this exists. There’s no common exchange or clear pricing.

Here’s what actually happens: when you press “buy,” you’re essentially purchasing physical gold stored by someone else on your behalf. This means a 3% GST kicks in immediately. On a ₹10,000 purchase, that means ₹300 is gone right away.

Then there’s the spread. Each platform sets its own buy-sell prices, typically 2–3% apart, to cover vaulting, insurance, and logistics. So, another ₹200–300 disappears due to price differences.

In total, your ₹10,000 investment quickly turns into just ₹9,400–₹9,500 worth of gold—a 5–6% loss before the price even changes.

The Regulatory Vacuum Problem

Here’s what keeps SEBI awake at night: digital gold operates in a gray zone. Regulated brokers can’t sell digital gold anymore (since October 2021), but unregulated fintech apps can.

This creates an asymmetric risk where you have no investor protection mechanisms, no dispute resolution from SEBI, and no compensation fund (unlike bank deposits covered by DICGC).

If fraud happens, you’re pursuing a court case—expensive, lengthy, uncertain.

What Should Investors Actually Do?

If you have around ₹5-10k in digital gold, you’re probably fine holding it for now. The panic-selling loss might hurt more than staying put. But stop adding money to it.

If you have ₹50k-1L+, seriously consider shifting gradually to Gold ETFs. Don’t dump everything at once (that creates losses), but systematically move 25-50% over the next few months.

Before deciding, ask your platform:

- Is the gold stored with an independent, audited custodian?

- Can you physically redeem it on fair terms?

- What’s the platform’s financial stability?

The Better Alternatives SEBI Actually Recommends

Gold ETFs: Start with ₹500, buy anytime, trade on exchanges, full SEBI protection. Zero GST and zero making charges. Record inflows, with ₹83.6 billion added in September 2025. Requires a demat account but offers high liquidity and low expense ratios of 0.5-0.6%.

Gold Mutual Funds (Fund of Funds): No demat needed—ideal for beginners. These mutual fund schemes invest in gold ETFs on your behalf. Start with SIPs from ₹500. Expense ratios range from 0.10% to 1.2%. Top funds like SBI Gold Fund, HDFC Gold ETF FoF, and Axis Gold Fund delivered 32% returns over three years. No entry/exit loads and fully SEBI-regulated.

Electronic Gold Receipts (EGRs): New instruments backed 1:1 by physical gold, traded on exchanges, regularly inspected by depositories.

Sovereign Gold Bonds (SGBs): The government has discontinued issuing new Sovereign Gold Bonds. The last tranche was issued in February 2024, and no new issues are planned for 2025. However, if you already hold SGBs, you can still redeem them on scheduled dates or trade them on stock exchanges. For those seeking the tax benefits SGBs offered, Gold ETFs are now your better option.

All these alternatives offer actual regulatory oversight and peace of mind.

Bottom Line: Knowledge Is Your Real Investment

Digital gold isn’t illegal, it’s just unregulated. SEBI didn’t ban it; they just warned you that you’re on your own. Think of it like buying from a vendor without a shop license. It might work, but if something breaks, the government won’t fix it.

Your best move? Understand what you own, know the costs, and make an informed choice. If you’re just starting with gold, skip digital gold entirely and go straight to Gold ETFs—especially when gold is at historic highs and investor confidence is strong. If you already have digital gold among 50+ million users, don’t panic—just have a plan to gradually transition to regulated products.

Remember, Gold is forever, but unregulated platforms? They might not be.

The choice is yours. But now you know exactly what you’re choosing.

FAQs

Yes, digital gold is legal but completely unregulated. Platforms operate under general business laws, not under SEBI or RBI supervision. SEBI’s November 2025 warning didn’t ban it—it simply clarified that these products fall outside regulatory protection. So while buying digital gold is legal, investors have no safety net if something goes wrong.

Yes, but it’s costly. Platforms charge 5–10% making charges and additional delivery fees, depending on weight and location. There’s also a minimum redemption limit (often 1 gram). So, if you redeem ₹10,000 of digital gold, you could lose ₹750–₹1,500 in costs before receiving your gold.

Digital gold is stored in a platform wallet with zero SEBI oversight, while Gold ETF units sit in your demat account with full SEBI protection. Gold Mutual Funds (specifically Fund of Funds schemes) are also fully SEBI-regulated and don’t require a demat account—they’re ideal for beginners. On costs, digital gold charges 4-5% spread, while Gold ETF spreads are only 0.5-1%, and Gold Mutual Funds have expense ratios of 0.10-1.2%. Digital gold attracts 3% GST at purchase, while both Gold ETFs and Gold Mutual Funds have no GST. Gold ETF expense ratios are 0.5-0.6% annually, and Gold Mutual Funds range from 0.10-1.2%. Digital gold offers 24/7 trading, while Gold ETFs and Gold Mutual Funds trade/process during business hours. The biggest advantage of Gold Mutual Funds? You can start with SIPs as low as ₹500 and don’t need a demat account, making them perfect for beginners. Top funds like SBI Gold Fund have given 32% returns in the past three years.

If a digital gold platform collapses, you’re unprotected. SEBI can’t intervene, and there’s no investor compensation fund. Recovery would require a long, costly court case to prove your gold exists in their vaults. This counterparty risk is exactly what SEBI warned about.

No. For small amounts (₹5k–₹10k), hold but stop investing more. For larger sums (₹50k+), exit gradually—move 25–50% to Gold ETFs over time. Avoid losses from sudden sales. Before deciding, check if your platform uses audited custodians and allows fair redemption.

SEBI suggests regulated options:

- Gold ETFs – start with ₹1,000, SEBI-regulated, no GST, transparent pricing.

- Electronic Gold Receipts (EGRs) – 1:1 backed by physical gold, traded on exchanges.

- Gold Futures on MCX – regulated commodity contracts.

(SGBs ended in 2024 but remain tradable.)

For most investors, Gold ETFs are the safest, cheapest, and most transparent choice.

The information provided in this reference is for educational purposes only and should not be considered investment advice or a recommendation. As an SEBI-registered organization, our objective is to provide general knowledge and understanding of investment concepts.

It is recommended that you conduct your own research and analysis before making any investment decisions. We believe that investment decisions should be based on personal conviction and not borrowed from external sources. Therefore, we do not assume any liability or responsibility for investment decisions made based on the information provided in this reference.