![]()

THE STORY BEHIND YOUR LATE-NIGHT PIZZA & AMAZON BOX

You order pizza at 11 PM. It arrives by midnight. Your Amazon parcel shows up the next day. You return a shirt to Flipkart—picked up from your doorstep in hours. Behind all this magic isn’t some superhero. It’s Shadowfax—a 10-year-old logistics company that’s been quietly working in the background, moving millions of packages every single day across India.

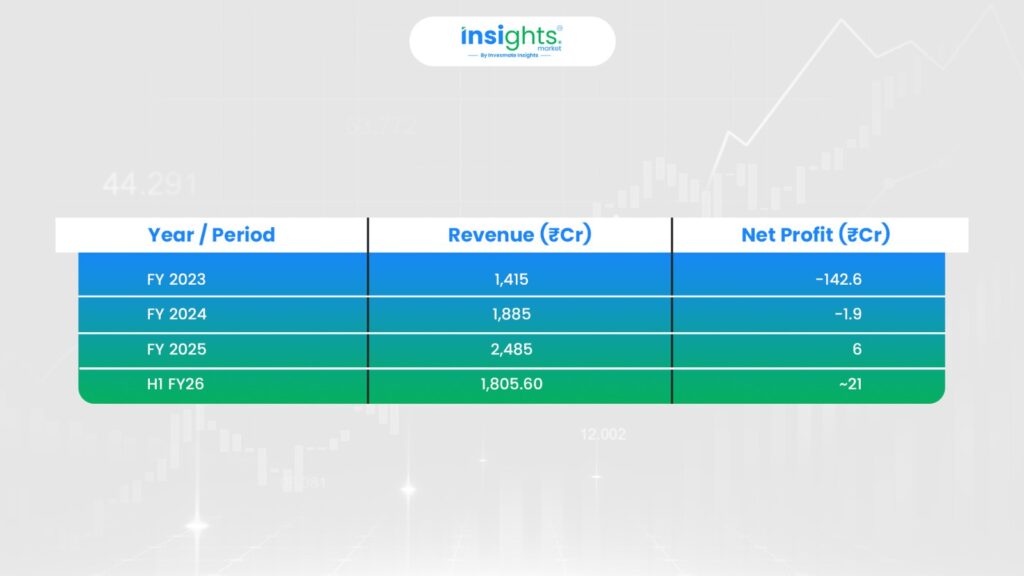

But here’s the thing: Shadowfax has been losing tons of money doing this. Imagine running a business that delivers packages faster than anyone else, but burning cash every single day. That’s exactly what happened in 2023—they lost ₹142 crore. But something changed. In 2025, they finally started making money. Not just a little. They’re now achieving profitability while delivering more packages than ever before.

And now, they’re coming to the stock market with a ₹1,970 crore IPO asking you and millions of other Indians to bet on their growth.

Should you invest? Let’s find out together.

IPO TIMELINE

WHO IS SHADOWFAX, REALLY?

Shadowfax isn’t just another delivery company. They’re the backbone of India’s online shopping experience. When Flipkart promises you delivery tomorrow, when BigBasket promises your groceries in 30 minutes, when Zomato promises your food in 20 minutes—Shadowfax is often the one making it happen behind the scenes.

Think of them as a Swiss Army knife for delivery. While others specialize in one thing, Shadowfax does it all:

- Express Services: Your Amazon parcel, Flipkart order, returns—all handled (~69% of revenue)

- Hyperlocal Services: That pizza, those groceries arriving in 30–60 minutes (~20% of revenue)

- Other Services: Dark stores, critical items, anything else you need moved fast

They work with Flipkart, Meesho, Swiggy, Zomato, Zepto, Nykaa—basically, if you’ve ordered something online and it arrived quickly, Shadowfax probably helped.

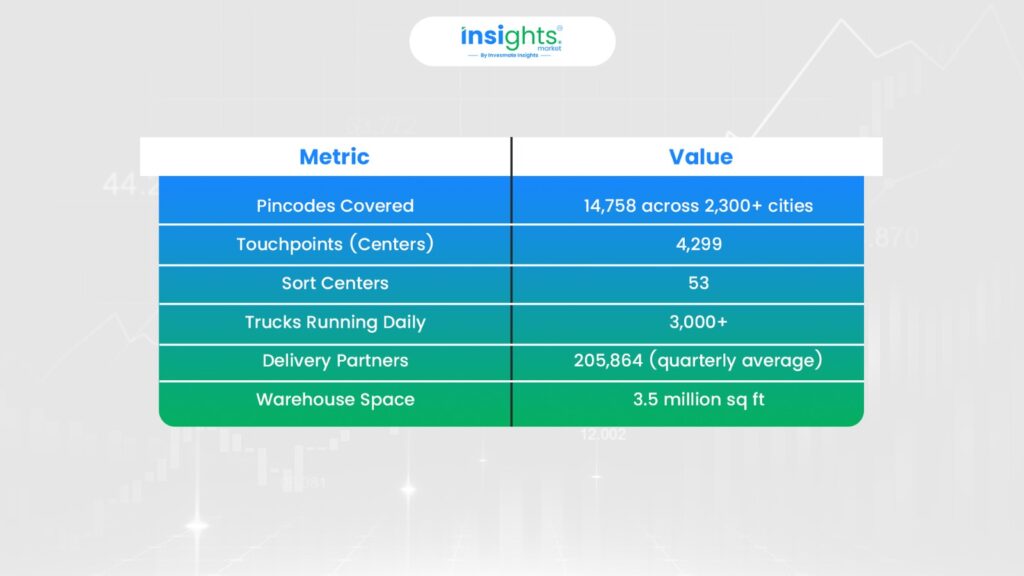

SERVICE NETWORK & SCALE: BY THE NUMBERS

Key Achievement: Shadowfax is India’s #1 3PL player for reverse shipments (returns) and same-day deliveries by order volume—the hardest services to execute and the ones that support better margins.

Capital Efficiency: Shadowfax has the highest capital turnover ratio (3.96x) among listed Indian peers in FY25. This means they generate ₹3.96 in revenue for every ₹1 invested in assets—a leaner setup with less capex dependency.

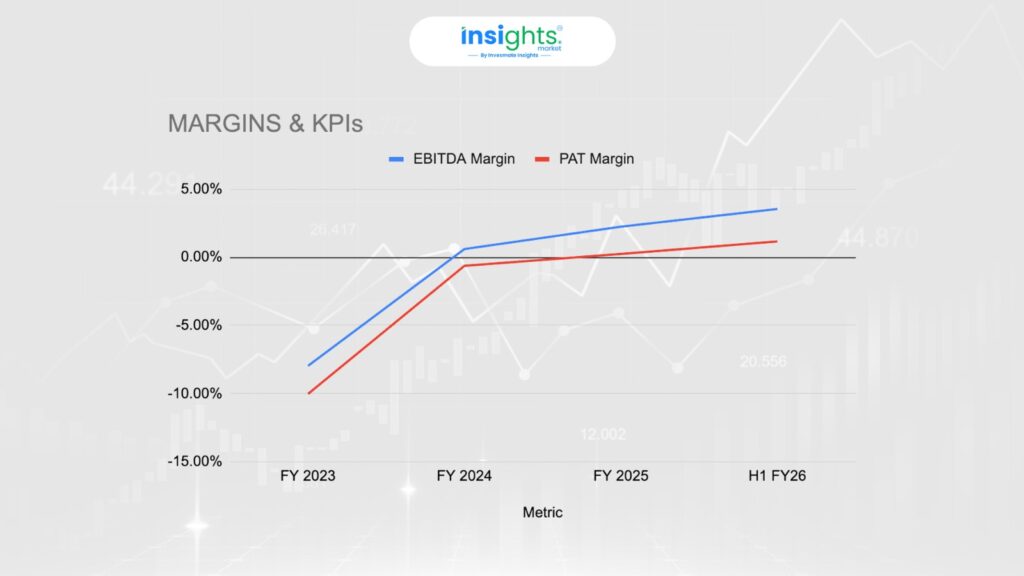

THE FINANCIAL TURNAROUND: HOW MARGINS TELL THE REAL STORY

This is where execution quality matters most.

Margins

Revenue & Profit

Growth is Real: H1 FY26 revenue of ₹1,805.6 crore is up 68% YoY from ₹1,072 crore in H1 FY25.

Critical Insight: In a business with thin margins (1–2%), even small operational failures cascade into profit problems. A 1–2% improvement in cost efficiency changes everything. But so does a 1–2% pricing pressure or cost spike.

THE HIDDEN RISK: LOST & DAMAGED SHIPMENTS

This is the detail many miss. In H1 FY26, Shadowfax reported lost shipment costs of ₹148.2 crore. That’s massive.

Why it matters: When you’re moving millions of packages daily and your profit margin is only 1–2%, operational errors directly destroy profitability.

What This Signals: As volumes explode (68% growth), small error rates become big rupee numbers. One misrouted package seems minor. 100,000 misrouted packages = ₹10+ crore loss.

WHY ARE THEY RAISING ₹1,000 CRORE IN FRESH FUNDS?

Use of funds:

- Capex (₹423 crore): Buy trucks, install sorting machines, upgrade technology

- Lease Payments (₹139 crore): Rent new delivery centers in new cities

- Marketing (₹89 crore): Build brand awareness

- Strategic Buys (Remaining): Acquire smaller logistics companies

Translation: They’ve proven they can make money. Now they want to expand network capacity, lease new centers, and boost delivery partner supply before competition catches up.

Note: ₹907.27 crore OFS is early investors (Flipkart, Fidelity, Qualcomm, IFC, Nokia) exiting—they’re taking profits, not funding growth.

CRITICAL BUSINESS MIX: EXPRESS PARCEL DOMINATES, QUICK COMMERCE GROWING

Revenue Breakdown (FY25):

- Express forward parcel deliveries: ₹1,716 crore (69%)

- Hyperlocal (quick commerce, food): ₹513 crore (20%)

- Other logistics: ₹256 crore (11%)

Why This Matters: Express deliveries are stable, but quick commerce demands are relentless. 30-minute deliveries require more touchpoints, more delivery partners, and higher operational complexity. Growth comes with execution risk.

THE COMPETITION & VALUATION: HOW DO THEY COMPARE?

What This Means: Shadowfax sits between peers. Valuation is reasonable for a company just achieving profitability with 68% revenue growth.

KEY STRENGTHS: WHY SOME PEOPLE ARE EXCITED

- Only Player Doing Everything: Express + hyperlocal + food. Competitors specialize; Shadowfax owns all three.

- Capital Efficient: 3.96x capital turnover = can grow without massive capex every cycle.

- India’s Biggest in Returns & Same-Day: Hardest services to execute = stickier clients, better margins potential.

- Giant Gig Fleet: 205,864 delivery partners = instant scale-up/down without employment commitments.

- Perfect Market Timing: E-commerce boom + quick commerce explosion

KEY RISKS: WHAT COULD GO WRONG

- Razor-Thin Margins (1–2%): One mistake = profits vanish. No cushion for error.

- Flipkart Dependency: One client = 48.91% of revenue. Contract change = revenue collapse.

- Leased Facilities Risk: Facilities are leased, not owned. Renewal problems or cost hikes can disrupt operations. Shifting a hub or last-mile center impacts delivery speed and customer satisfaction.

- Delivery Partner Churn: 205,864 gig workers can leave if pay drops or competitors offer better incentives. Peak season shortages = cost pressure.

- Lost Shipment Risk: ₹148.2 crore in H1 FY26 is already high. As volumes scale, error rates multiply into bigger losses.

WHO THIS IPO MAY SUIT — AND WHO IT MAY NOT

This IPO may suit investors who believe in the long-term growth of India’s e-commerce and quick-commerce ecosystem, understand the realities of low-margin infrastructure businesses, and can commit capital for 3–5 years.

It may not suit investors seeking quick listing gains, stable dividend income, or businesses with wide and predictable margins.

GMP Trend

Date | IPO Price (₹) | GMP (₹) | Estimated Listing Price (₹) | Expected Listing Gain |

18 Jan 2026 | 124 | 10 | 134 | ~8.1% |

17 Jan 2026 | 124 | 9 | 133 | ~7.3% |

16 Jan 2026 | 124 | 15 | 139 | ~12.1% |

Bottom line

Shadowfax is a legitimate, scaled logistics platform that has crossed the critical profitability threshold. Its nationwide network, strong client base, and improving margins make it a serious contender in India’s logistics infrastructure story.

At the same time, the business remains fragile. Thin margins, high client concentration, shipment-loss costs, and dependence on a gig workforce mean execution must remain near-flawless.

This IPO is not about excitement or quick money. It is a measured bet on execution and scale. Investors should approach it with realistic expectations, patience, and a clear understanding of the risks involved.

FAQs

₹14,160 (120 shares @ ₹118, lower price band).

Fresh issue (₹1,000 crore) strengthens Shadowfax’s balance sheet. OFS (₹907 crore) just reshuffles ownership. For you as a buyer, both are new shares you can purchase.

They have the highest capital turnover ratio (3.96x) among listed peers—meaning they generate more revenue per rupee of assets invested.

Flipkart (₹4,000 crore), Fidelity (₹1,970 crore), Qualcomm, IFC, Nokia. Strong VC backing validates the business.

For a company handling millions of daily deliveries, it’s a concern. Signals execution challenges as volumes scale.

Minimum 3–5 years. Margin expansion takes time in logistics.

The information provided in this reference is for educational purposes only and should not be considered investment advice or a recommendation. As an SEBI-registered organization, our objective is to provide general knowledge and understanding of investment concepts.

It is recommended that you conduct your own research and analysis before making any investment decisions. We believe that investment decisions should be based on personal conviction and not borrowed from external sources. Therefore, we do not assume any liability or responsibility for investment decisions made based on the information provided in this reference.