![]()

In a market where investors are constantly hunting for undervalued opportunities, the price-to-earnings (P/E) ratio remains one of the most widely used tools for identifying potential value buys. When high-quality companies trade below their long-term average P/E ratios, it often sparks interest. However, it’s essential to separate genuine value opportunities from possible value traps—stocks that look cheap but suffer from structural issues or weak future prospects.

Two prominent Indian companies—Maruti Suzuki and Cipla—are currently trading below their 10-year median P/E ratios. Both have strong fundamentals, but their recent growth trajectories have softened. Are these signs of temporary headwinds, or is the market rightly skeptical? Let’s take a closer look.

Read Also: Indian Stock Market Reaction To Wars; Conflicts, And Terror Attacks: A Look Since 1990

Maruti Suzuki: Leadership with Execution Risks

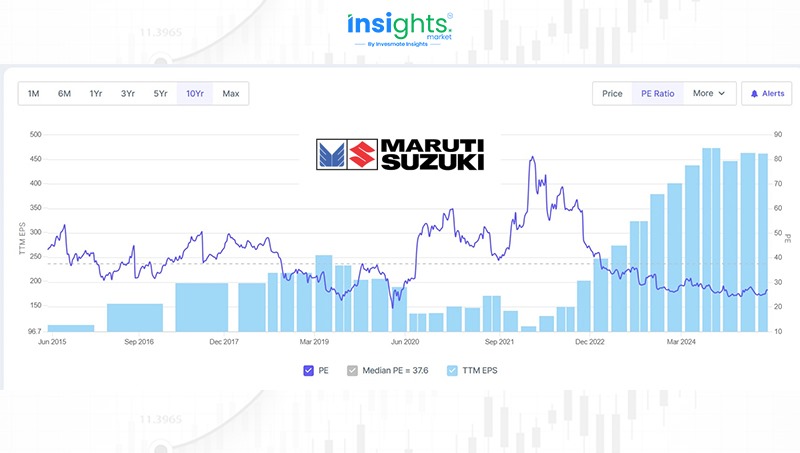

P/E Snapshot:

- Current P/E: 26.6x

- 10-Year Median P/E: 37.6x

Maruti Suzuki is undeniably a titan in the Indian auto sector, commanding around 42% of the passenger vehicle market and leading both mini and compact car segments. The company reported a strong FY24, with its highest-ever annual sales volume of 1.79 million units. Key drivers included a robust SUV lineup, which saw a 119% year-over-year jump in sales, and solid export momentum that saw a 10% rise in outbound shipments. Maruti Suzuki’s SUV segment gained strong traction in FY25, accounting for 36% of its domestic passenger vehicle sales.

Financial Performance:

Export Outlook:

Exports rose to 332,585 units in FY25, reflecting a 17.5% increase from the previous year. Looking ahead, exports are expected to grow by 20% year-on-year in FY26. The company’s global footprint now extends to nearly 100 countries, with key export destinations including Chile, Mexico, Saudi Arabia, South Africa.

The Key Risks:

- Domestic demand is tapering due to macroeconomic challenges.

- Market competition in the SUV and EV segments is intensifying.

- Execution on EV strategy and international expansion must deliver.

Bottom Line:

Maruti Suzuki Share Price

Cipla: A Pharma Powerhouse with Global Reach

P/E Snapshot:

- Current P/E: 25x

- 10-Year Median P/E: 31x

Cipla has long held a strong presence in India’s pharmaceutical landscape and is expanding globally, particularly in the U.S. and Africa. With a diversified product portfolio and exposure to high-margin chronic therapies, Cipla enjoys a solid revenue mix. The company’s FY24 performance was supported by strong U.S. sales, including key generic launches like Revlimid and Albuterol.

Financial Performance:

R&D Outlook:

The Key Risks:

- Slower domestic and international growth in recent quarters.

- Regulatory uncertainties in key markets like the U.S.

- Execution risk in launching complex and specialty products.

Bottom Line:

Cipla’s fundamentals remain intact, and margin expansion shows resilience. The company’s innovation and U.S. strategy could drive the next phase of growth. If execution stays strong, the current valuation may indeed be a discount.

Cipla Share Price

Final Thoughts: Value Buys or Value Traps?

Both Maruti and Cipla present intriguing cases for value-focused investors. They are fundamentally solid, boast market leadership, and operate in sectors with long-term tailwinds. However, both are facing moderate growth in the near term, which has likely contributed to their current P/E discounts.

The key determinant moving forward will be execution—whether Maruti can navigate the EV transition and sustain exports, and whether Cipla can capitalize on its U.S. pipeline and specialty focus. If they succeed, the current valuations could offer attractive entry points. If not, the market’s caution might prove justified.

Investor takeaway: Watch upcoming product launches, margin trends, and management commentary closely. These will reveal whether the stocks are mispriced opportunities—or stocks priced just right.