![]()

Look, if you’ve been watching your portfolio lately and wondering why your Tata Consultancy Services or Infosys shares keep bleeding red, you’re not alone.

The IT sector has lost over ₹2 lakh crore in market value recently. The NIFTY IT is at multi-month lows. And yet — there hasn’t been a catastrophic earnings miss.

This isn’t a normal correction.

This is a structural reset.

The Fall That Won’t Stop

Here’s what makes this confusing:

- TCS is still profitable.

- Infosys is still winning large deals.

- HCLTech has raised guidance.

- Wipro hasn’t reported a disaster.

Yet stocks fall 2%, recover slightly, then fall again.

It feels like water slowly draining from a bathtub — steady and persistent.

So what’s really happening?

The Real Reason: Future Growth, Not Current Earnings

The market isn’t worried about what IT companies earn today.

It’s worried about what they’ll earn five years from now.

And that worry has a name: Artificial Intelligence.

But here’s something crucial most people are missing:

Indian IT management teams are not guiding for an “AI death spiral.”

They are broadly saying three things:

- Near-term growth is weak.

- AI is structurally disruptive.

- AI is a medium-term revenue and productivity opportunity — not an existential threat.

The recent fall is more about market psychology and business-model uncertainty than about what official guidance numbers are actually saying.

The Trigger: The $285 Billion “SaaSpocalypse”

On January 30, AI startup Anthropic released 11 open-source plugins for its enterprise AI assistant, Claude Cowork.

Within a single trading session, roughly $285 billion was wiped off global software stocks.

The media quickly called it a “SaaSpocalypse.”

What spooked investors wasn’t a breakthrough model.

It was workflow ownership.

What Exactly Did Anthropic Release?

Claude Cowork is an agentic AI assistant designed for non-technical professionals. It can:

- Read files

- Organize folders

- Draft documents

- Execute multi-step workflows

The new plugins allowed companies to customize Claude for specific job functions — sales, finance, marketing, data analysis, customer support, product management, and even biology research.

But the legal workflow plugin triggered panic.

It automated:

- Contract review

- NDA triage

- Compliance checks

- Legal brief drafting

No proprietary legal engine.

No special fine-tuned legal model.

Just structured prompts layered on top of Claude.

Yet markets reacted violently.

The Market Reaction Was Immediate

- Thomson Reuters fell over 15%.

- RELX (owner of LexisNexis) dropped 14%.

- LegalZoom plunged nearly 20%.

- A Goldman Sachs software basket saw its worst single-day fall since April.

The Nasdaq Composite declined 1.4%.

And the ripple hit India:

- Infosys ADRs slipped ~5.5%.

- Wipro fell nearly 5%.

This wasn’t about quarterly earnings.

It was about this shift:

AI is no longer just powering software companies.

AI might start replacing parts of them.

When Claude was just an API, companies could build on top of it.

When Anthropic began publishing ready-made vertical solutions, it moved up the value chain — from infrastructure provider to competitor.

That’s the real shock.

Why This Matters for Indian IT

Indian IT doesn’t sell legal software.

It sells workflows.

If AI can compress a 12-month project into 4 months, cut a 300-person team to 100, and automate multi-step processes, revenue growth becomes less linear.

That’s why the manpower model looks vulnerable.

Markets aren’t pricing collapse.

They’re pricing transition risk.

How Indian IT Companies Actually Make Money

For decades, Indian IT worked on a beautifully simple model:

A US bank needs to migrate their systems? Send 500 engineers. Work for 18 months. Bill by the hour. Everyone’s happy.

This “manpower model” built a ₹30 lakh crore industry. It gave millions of Indians jobs. It made investors wealthy.

What Actually Triggered This Sell-Off?

Several things hit together:

- Global tech correction led by weakness in US markets.

- Fear that “agentic AI” tools (like autonomous workflow AI systems) can replace multi-step legal, finance, and customer service work.

- Concerns that AI will:

- Reduce outsourcing demand

- Compress pricing

- Cap headcount-led growth

- Reduce outsourcing demand

Investors re-read management commentary through a far more bearish lens.

But here’s the important distinction:

Earnings guidance still implies low single-digit growth — not collapse.

What Management Is Actually Saying

Across Tata Consultancy Services, Infosys, HCLTech, and Wipro, commentary has been surprisingly consistent:

1. AI Is Already a Revenue Line Item

- TCS reports ~$1.8 billion annualised AI services revenue.

- HCLTech’s Advanced AI revenue is growing ~20% QoQ.

- Infosys says almost every large deal now has a GenAI component.

- Wipro calls GenAI central to nearly every opportunity.

This is not theoretical anymore.

2. Guidance Is Weak — But Not Collapsing

- Infosys guidance: ~3–3.5% CC revenue growth.

- HCLTech: ~4–4.5% CC growth.

- Margins remain broadly stable.

That’s cyclical weakness + transition.

Not implosion.

3. Clients Want ROI — Not Experiments

Clients now expect:

- 15–40% productivity gains

- Clear cost benefits

- Faster delivery cycles

They’re moving from AI pilots to scaled implementation — but they want proof.

That creates pricing pressure in the short term.

4. Massive Reskilling Is Underway

- TCS has trained 200,000+ employees in AI.

- Wipro has trained 87,000+ employees.

- HCLTech has trained over 127,000 employees.

- Infosys is pushing its “Topaz” AI platform aggressively.

Only ~2% of enterprises globally are fully AI-ready across data, governance, and talent.

That suggests a long runway for services.

So What’s The Real Fear?

It’s not demand vanishing.

It’s the business model changing.

The Uncomfortable Math

Old Model:

300 engineers × 12 months × $100/hour

= $28.8 million revenue

AI Model:

100 engineers × 4 months × $100/hour

= $9.6 million revenue

Same client outcome.

Much lower billing.

If productivity rises 30%, clients will want part of that gain.

This is called revenue deflation risk.

Less a Collapse, More a Transition

Industry analysts describe this phase as structural transition.

Indian IT may not build foundational AI models.

But it is positioned as:

- AI integrator

- Workflow optimizer

- Enterprise transformation partner

That’s a different growth model:

- Higher revenue per employee

- More outcome-based pricing

- Less linear hiring

The market is unsure how to value that yet.

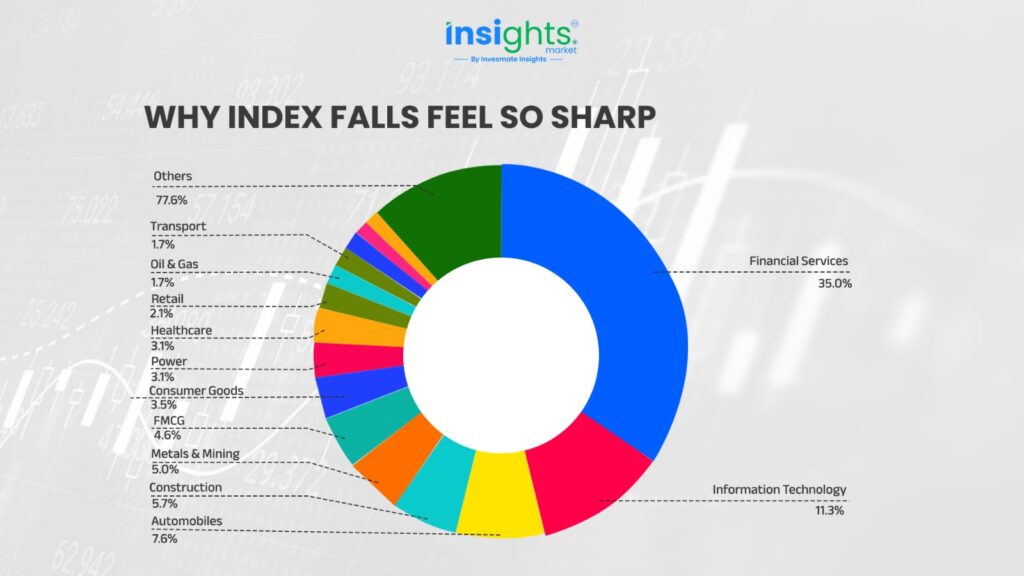

Why Index Falls Feel So Sharp

The NIFTY 50 is concentrated.

- IT weight ~10–11%

- Infosys ~5%

- TCS ~3%

When these two fall 5–6%, they drag the entire index.

Add weakness in financials, and you get 1% Nifty drops quickly.

When growth expectations fall, stock valuations fall. It’s that simple.

What To Track Going Forward

Instead of panicking, track these metrics:

- AI revenue growth disclosure

- Share of outcome-based contracts

- Revenue per employee trends

- Hiring vs. automation trends

- Medium-term growth guidance post-FY26

If companies maintain 4–5% growth and stable margins while AI revenue rises — the worst fears may not materialize.

The Bottom Line

Indian IT stocks are not falling because management has guided collapse.

They are falling because the market is repricing uncertainty.

The old belief was:

“You’ll grow 12% forever.”

The new assumption is:

“Maybe it’s 3–5% for a few years.”

That difference changes valuations dramatically.

This isn’t panic.

It’s adjustment .

AI is disrupting the manpower model.

Management teams say they’ll adapt.

Investors aren’t fully convinced yet.

That tension — between guidance and fear — is what’s driving this sell-off.

The old growth story is fading.

The new AI-led one is still forming.

And markets hate uncertainty more than they hate bad news.

FAQs

The fall isn’t about current earnings—it’s about future growth expectations. Markets price stocks based on 5–10 year projections, and AI is making investors doubt whether double-digit growth can continue. Even if Q3 results look fine, concerns about revenue deflation starting in FY27 are causing valuations to compress now.

No, but it will transform it. AI won’t eliminate tech spending—it’ll change where that spending goes. Companies that successfully transition from manpower-based services to AI-enabled platforms and consulting can thrive. Think of it as evolution, not extinction—but not all companies will adapt successfully.

That depends on your time horizon and risk appetite. Some quality stocks may be attractively priced if you believe in their ability to adapt to AI. However, the volatility may continue until there’s clarity on deal flow and AI’s actual impact on revenues. Consider rupee-cost averaging instead of lump-sum investment, and focus on companies demonstrating clear AI transformation strategies.

Companies investing heavily in AI reskilling (like TCS with 200,000+ trained employees), developing proprietary AI platforms, and winning AI-specific contracts are better positioned. Watch for firms moving toward outcome-based pricing and platform businesses rather than traditional staffing models. Quarterly deal flow announcements will be crucial indicators.

Honestly, no one knows—but analysts suggest volatility will continue until two things happen:

- US markets stabilize and tech spending visibility improves

- Indian IT companies provide clearer guidance on how AI impacts their deal pipelines and revenue models

This could take several quarters. The correction is fundamentally about repricing long-term growth, not a temporary panic.

Panic selling is rarely wise. If you’re a long-term investor, consider whether the companies you hold are adapting to AI. If you’re near retirement or need liquidity soon, speak with a financial advisor. Remember: the sector isn’t dying—it’s transforming. But the transformation period will be bumpy, and not all companies will emerge as winners.

This analysis is for informational purposes only and does not constitute investment advice. Readers should conduct their own due diligence or consult financial advisors before making investment decisions.