![]()

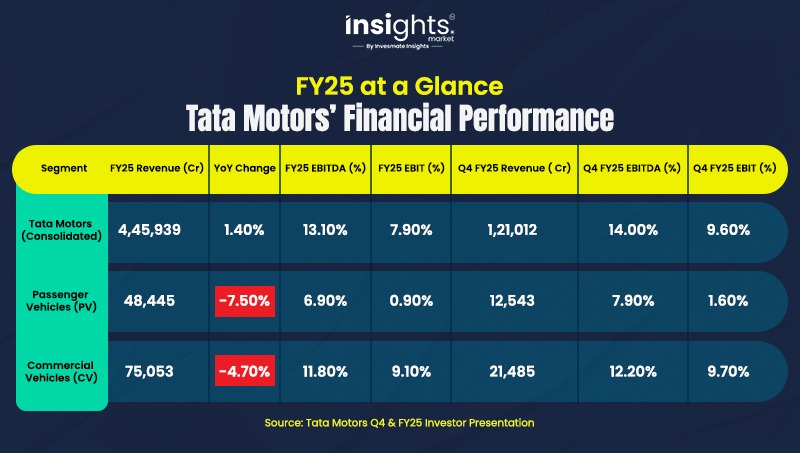

FY25 at a Glance: Tata Motors’ Financial Performance

The EV Business: Profitability Achieved Despite Volume and Market Share Decline

A Historic Turnaround

- EBITDA Positive for the First Time: Tata Passenger Electric Mobility (TPEM) reported a positive EBITDA margin of 6.5% in Q4 FY25, marking a significant turnaround from previous losses.

- Profit Before Tax (PBT): The EV arm posted a PBT of ₹100 crore in FY25, reversing a loss of ₹400 crore in FY24.

- Operational Efficiency: This profitability was driven by improved cost management, better supply chain efficiencies, and a focus on higher-margin EV models.

The Volume and Market Share Paradox

- Declining EV Sales: Despite the profitability, Tata’s EV volumes fell by approximately 10.7% YoY, with around 57,616 units sold in FY25 compared to 64,530 units in FY24.

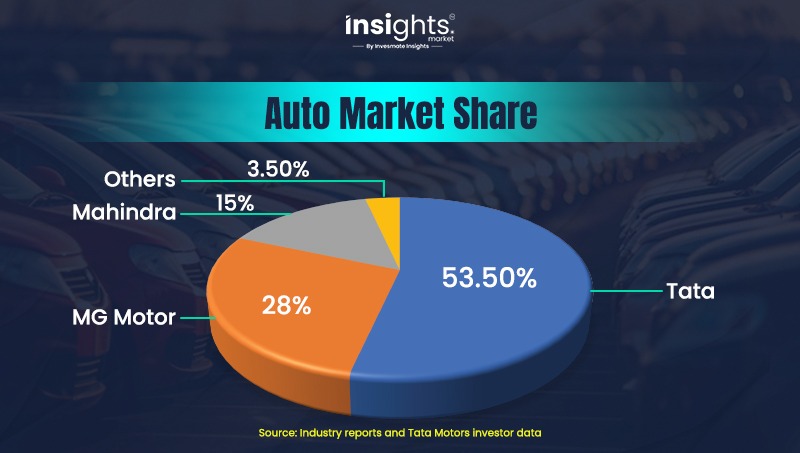

- Market Share Drop: Tata’s EV market share dropped sharply from 70.5% in FY24 to 53.5% in FY25, as competitors like MG Motor and Mahindra aggressively expanded their EV portfolios.

- April 2025 Snapshot: Tata sold 4,461 EVs in April 2025, a 14% YoY decline, while MG Motor and Mahindra posted triple-digit growth, pushing Tata’s market share down to 36% for the month.

Passenger Vehicle Segment: Revenue and Margin Pressures Persist

- Revenue Decline: The PV segment’s revenue dropped 7.5% YoY to ₹48,445 crore in FY25, with Q4 revenue down 13.1% YoY.

- Profitability Squeeze: EBIT margin shrank to a mere 0.9% in FY25, down 110 basis points from the previous year, reflecting the impact of intense competition and operational inefficiencies.

- Volume Challenges: PV sales volumes fell 5.5% YoY in Q4, with hatchbacks and sedans particularly impacted.

- Operational Issues: Tata Motors acknowledged product and service quality challenges across its PV portfolio and committed to corrective actions including network expansion, enhanced customer service, and product refreshes.

Profitability Up, Volumes and Market Share Down

This paradox – profitability rising even as volumes and market share decline – can be explained by several factors:

- Cost Discipline and Operational Efficiency: Tata’s EV business optimized production costs and improved supply chain management, helping margins even as unit sales fell.

- Product Mix Shift: Focus on higher-margin EV models and premium variants boosted profitability despite fewer units sold.

- Competitive Intensity: Rivals like MG Motor and Mahindra aggressively captured market share through new launches, competitive pricing, and expanding dealer networks, pressuring Tata’s volumes.

- Industry Dynamics: The Indian EV market grew approximately 11% in FY25, but Tata’s share shrank, highlighting the rapidly evolving competitive landscape.

Competitive Landscape: Tata’s Rivals Gain Ground

- MG Motor: Leveraged aggressive pricing and fleet partnerships to grow its EV sales exponentially.

- Mahindra: Benefited from the strong brand pull in SUVs and launched new EV models, drawing urban and semi-urban buyers.

- New Entrants: BYD, Hyundai, and even Maruti Suzuki are preparing to launch multiple EVs, promising even more competition in FY26.

Also Read: Tesla vs. Tata & Mahindra: Will the EV Giant Disrupt India’s Auto Market?

Tata’s Strategic Response: What’s Next?

1. Product Pipeline

- Upcoming Launches: Tata plans to launch the Curvv EV, Harrier EV, and Sierra EV in FY26, aiming to reclaim lost ground in both premium and mass-market segments.

- Affordable EVs: Tata is working on a new, more affordable EV platform to compete with MG’s Comet and upcoming Maruti Suzuki EVs.

2. Customer Experience

- Service Overhaul: Tata is investing in after-sales service, digital platforms, and customer engagement to address past reliability and service complaints.

- Charging Infrastructure: Through Tata Power, the company is expanding public and home charging solutions to make EV ownership easier.

3. Operational Efficiency

- Localization: Tata is increasing local sourcing of key EV components, especially batteries and power electronics, to reduce costs and improve supply chain resilience.

- Sustainability: The company is pushing for greener manufacturing, aiming to make its EV business not just profitable but also environmentally responsible.

4. Operational Challenges and Improvement Initiatives

Tata Motors has openly acknowledged operational and quality issues across both its EV and ICE passenger vehicle lines. In FY2025, the company prioritized fixing gaps in after-sales service, product quality, and software integration, especially in urban markets. Tata expanded service capacity, added new outlets, and overhauled its product validation and software testing to rebuild customer trust and ensure a robust ownership experience.

What This Means for Tata Motors and the Indian EV Market

Tata Motors’ EV Business Is Maturing

Market Share Loss Signals Need for Innovation

Passenger Vehicle Segment Remains a Challenge

Conclusion

Tata Motors’ FY25 results highlight a paradox: despite a sharp revenue drop in passenger vehicles due to falling EV volumes, its EV arm turned EBITDA-profitable for the first time. This shift marks Tata’s evolution from a volume leader to a profitable EV player, with future leadership hinging on sustaining profits and regaining market share.

On Range Rover pricing, Tata noted that any impact from the UK-India free trade agreement will depend on the final terms, reflecting a balanced approach to global opportunities and domestic strategy.

FAQs

Yes, Tata’s EV arm turned EBITDA-positive for the first time in FY25, posting a ₹100 crore profit before tax.