![]()

The rupee just crossed ₹96 per dollar and the doomsday forecasts are back. Before you hit sell, here’s what the actual data says about your portfolio.

1. Rupee Fear Is Back

Every few years, a new wave of panic announces that the rupee is in freefall and Indian equities are about to crumble. In May 2026, INR crossed ₹96 per dollar — and the forecasts of ₹100–₹150 are back in prime-time debates. The question every investor is quietly asking: Should I reduce my equity exposure before it gets worse?

Before you do anything, look at what actually happened — every single time this fear came around.

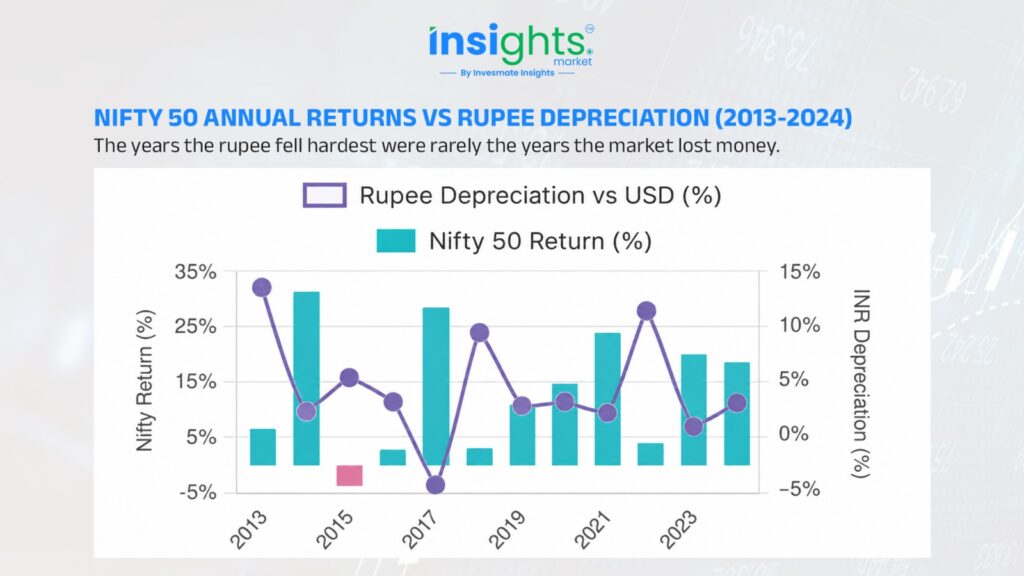

2. Has a Weak Rupee Hurt Indian Investors Historically?

The rupee has depreciated by more than 100% over two decades. And yet, over that same period, Indian equities delivered substantial wealth creation. Because corporate earnings grew faster than the currency weakened.

Notice the pattern: 2013 was a rupee crisis year — the taper tantrum sent INR tumbling — yet Nifty returned +6.8%. In 2022, the rupee fell over 11% against the dollar (the steepest single-year decline in a decade), yet Nifty still delivered +4.3%. The market’s direction was driven by earnings and sentiment, not the exchange rate alone.

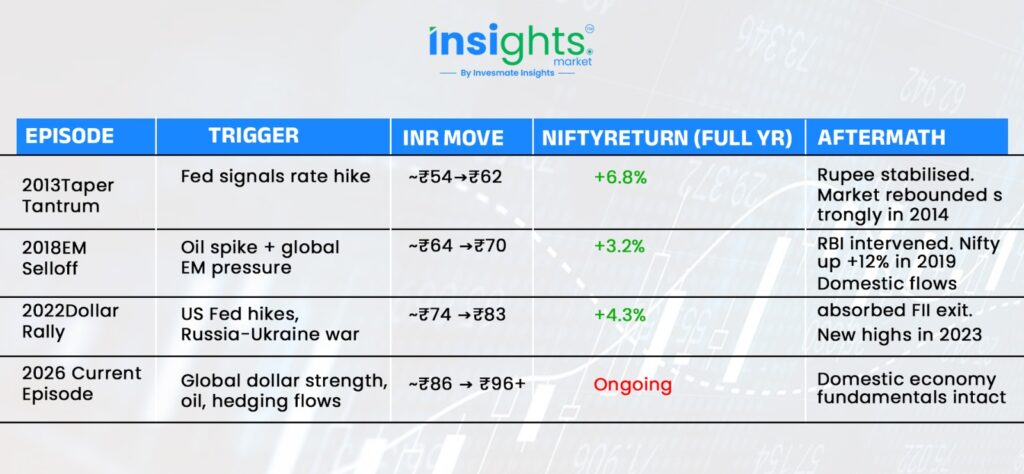

3. What Happens During Rupee Crises?

Look at every major rupee episode in recent memory. The pattern is remarkably consistent: sharp depreciation, peak fear, FII selling — and then stabilisation. Meanwhile, the domestic economy keeps growing underneath.

The current pressure is driven by global dollar strength, oil prices, and hedging behaviour — not by any collapse in domestic demand or corporate fundamentals. That distinction matters enormously for your portfolio.

“A falling rupee does not automatically destroy shareholder wealth. The bigger determinant has always been earnings growth, pricing power, and business quality.“

4. Why Corporate Profits Keep Growing

Here’s the mechanism most investors miss. When input costs rise due to a weak rupee, strong businesses don’t absorb the pain — they pass it on. And crucially, when input costs later normalise, prices rarely fall back completely. This “margin ratchet” is why India Inc’s profit-to-GDP ratio has climbed to a

15-year high of ~4.8% in FY24, even after years of currency weakness. By FY25, estimates put it closer to 6.9%. Corporate profits grew nearly 3× faster than GDP between FY20–25.

Private consumption’s share of GDP has simultaneously risen to a twodecade high of ~61%. Indian consumers keep spending despite higher prices — because incomes are rising too.

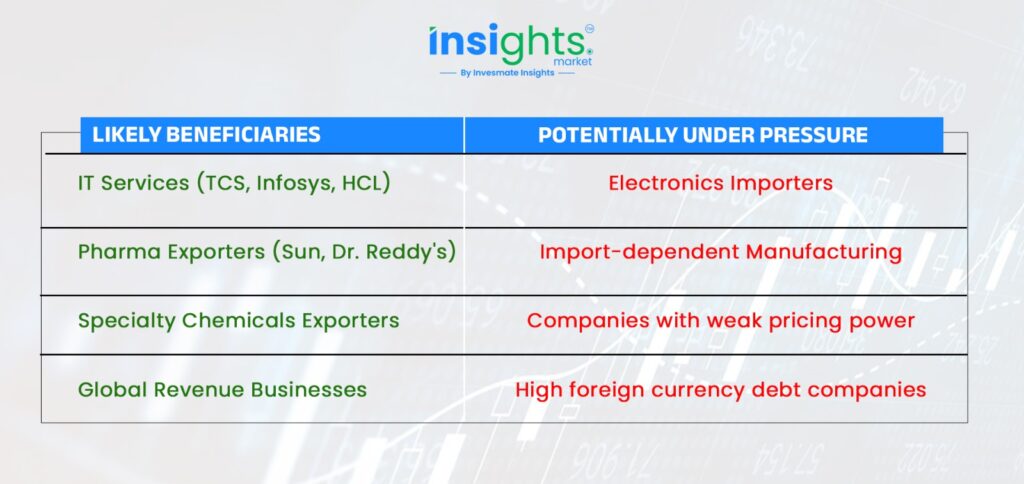

5. The Sectors That Benefit and Su!er

Rupee weakness doesn’t hit every stock equally. It redistributes profit pools. A 5–10% depreciation can lift operating margins for net exporters by 1.5–3 percentage points — while compressing margins for import-heavy companies that can’t pass on costs.

The direction of your portfolio matters more than the direction of the currency.

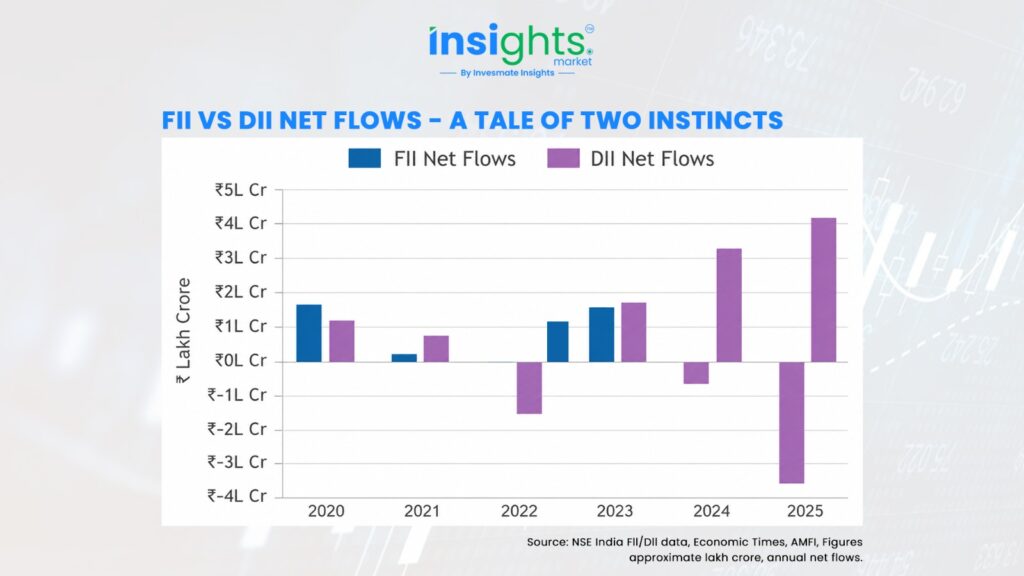

6. Why DIIs Often Buy When FIIs Sell

Between October 2021 and April 2022, FIIs sold roughly ₹1.6 lakh crore of

Indian equities — the largest selling streak since 2008. Yet Nifty was only 3– 4% below all-time highs, because domestic institutions kept buying. Equity mutual funds recorded 13 consecutive months of net inflows through the entire FII exodus.

FIIs need “perfect macro.” They exit when things look messy. DIIs — and SIPdriven retail flows — buy the same businesses at better prices. That is where long-term alpha gets created.

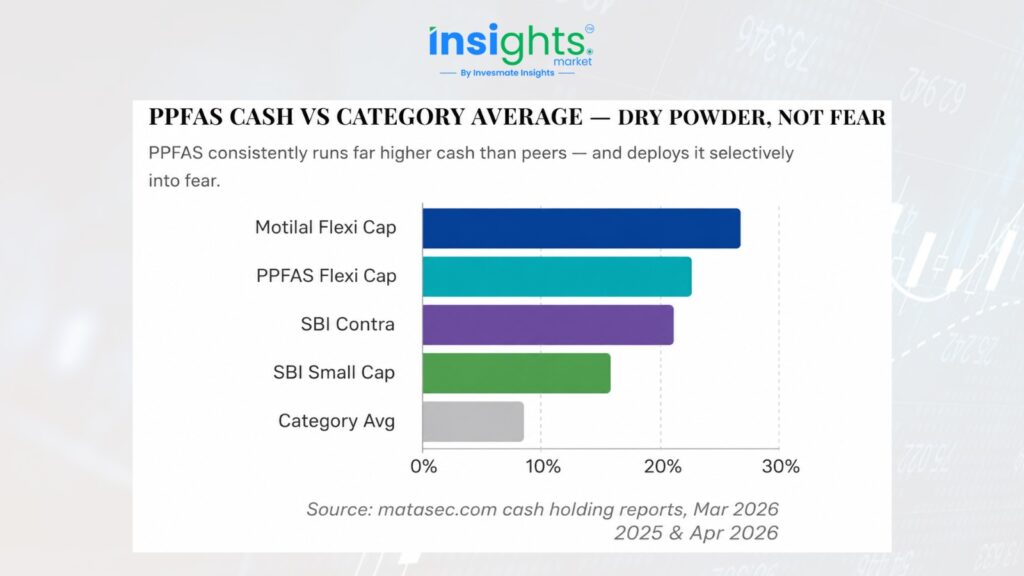

7. Parag Parikh Flexi Cap: The Smart Money Isn't Running

One of India’s most respected value investors isn’t exiting. PPFAS

Flexi Cap, with over ₹ 1.4 lakh crore AUM and a decade-plus track record of ~mid-teens annual returns, is doing something instructive right now.

8. How Investors Should Position Their Portfolio

The answer to a weak rupee isn’t to exit India. It’s to own the right India. The real protection against rupee weakness isn’t currency hedging or moving to gold — it’s owning businesses that can pass costs to consumers and retain those price hikes even when input costs ease. Think Asian Paints, Titan, HUL, Nestlé India.

PREFER TO

- Export-oriented businesses

- Global revenue companies

- Strong consumer brands

- Businesses with pricing power

- Low import dependence

BE CAUTIOUS OF

- High import dependency

- Thin or weak margins

- Heavy foreign currency debt

- Commodity price-takers

- No brand or pricing moat

Final Takeaway

Every major rupee scare in the last 20 years looked catastrophic in the moment — and manageable in hindsight. The investors who panicked and exited missed the recoveries. The ones who stayed, or accumulated selectively, captured the returns.

The rupee going from ₹39 to ₹90 didn’t break Indian equities. If it goes to ₹100 or beyond, the businesses with real earnings power, loyal customers, and pricing moats will still be standing — and probably more profitable in rupee terms than before.

Don’t fight the rupee. Own the businesses that don’t need to.

FAQs

No. Historical data shows that while a weaker rupee can create short-term volatility, it has not always led to long-term declines in Indian equities. Over the years, the rupee has depreciated significantly against the US dollar, yet Indian companies have continued to grow earnings and create shareholder wealth. The impact depends more on corporate profitability and economic growth than on the exchange rate alone.

Export-oriented sectors such as Information Technology (IT), pharmaceuticals, and certain manufacturing businesses often benefit from a weaker rupee because their overseas revenues translate into more rupees. Companies with global revenue streams and low import dependence may see improved profitability during periods of currency weakness.

Import-dependent sectors such as electronics, oil and gas marketing, chemicals, and certain manufacturing industries may face higher input costs when the rupee weakens. If these companies cannot pass on the increased costs to customers, their profit margins may come under pressure.

Not necessarily. History suggests that currency depreciation alone has not been a reliable reason to exit Indian equities. Investors should focus on business fundamentals, earnings growth, competitive advantages, and valuation rather than making investment decisions solely based on exchange-rate movements.

FIIs are influenced by global factors such as US interest rates, dollar strength, geopolitical risks, and capital flows. A weaker rupee can reduce their returns when converted back into dollars, prompting some investors to withdraw funds. However, domestic institutional investors (DIIs) often step in and provide support to the market during such periods.

Investors can focus on businesses with strong pricing power, export exposure, low import dependence, healthy balance sheets, and sustainable competitive advantages. Diversification across sectors and maintaining a long-term investment approach can also help navigate periods of currency volatility.

This article is for educational and informational purposes only. It is not investment advice or a stock recommendation. Investors should conduct their own research or consult a qualified financial advisor before making investment decisions.